en.Wedoany.com Reported - In the week ending June 5, 2026, Chinese steel prices declined, with the market showing seasonal slowdown characteristics. On the raw materials side, iron ore prices fell, domestic coke prices rose week-on-week, while billet prices remained stable.

Despite a significant drop in steel mill inventories, steel prices still moved lower. Data from the China Iron and Steel Association (CISA) showed that in late May (May 21-31), total steel inventories at key CISA mills stood at approximately 15.83 million tonnes, down 15.7% from 18.77 million tonnes in mid-May. However, on a month-on-month basis, this inventory level increased by 2.6% from 15.43 million tonnes in late April. Year-on-year, it rose by 3.5% from 15.3 million tonnes in late May 2025.

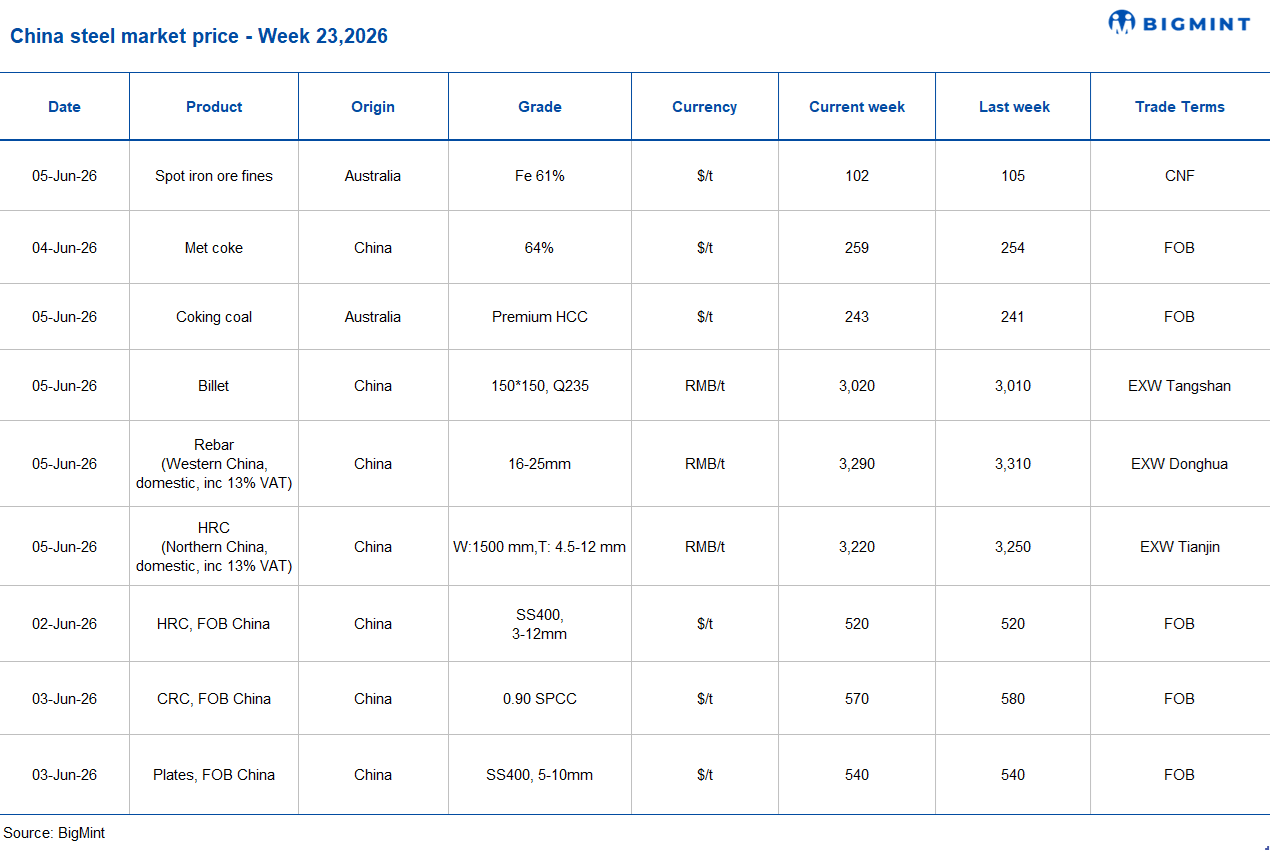

Domestic hot-rolled coil (HRC) prices fell by 30 yuan/tonne (about $4/tonne) week-on-week, dropping to around 3,220 yuan/tonne ($476/tonne) on June 5, compared to 3,250 yuan/tonne ($480/tonne) the previous week. The Shanghai Futures Exchange HRC futures contract (October 2026 delivery) edged down 19 yuan/tonne ($3/tonne) week-on-week, from 3,378 yuan/tonne ($499/tonne) a week earlier to 3,397 yuan/tonne ($502/tonne). China's HRC export offers were around $520/tonne FOB Rizhao, flat week-on-week. The domestic HRC market faced pressure this week, with weak seasonal demand continuing to drag down procurement and transaction volumes. However, firm production costs and stable export orders provided support, limiting price fluctuations.

As of June 5, Chinese rebar prices fell by 20 yuan/tonne ($3/tonne) week-on-week to 3,290 yuan/tonne ($486/tonne), compared to 3,310 yuan/tonne ($489/tonne) the previous week. The Shanghai Futures Exchange rebar futures contract (October 2026 delivery) edged down 13 yuan/tonne ($2/tonne) week-on-week, from 3,173 yuan/tonne ($469/tonne) a week earlier to 3,160 yuan/tonne ($467/tonne). Delayed and weak payments for construction projects continued to constrain procurement activities, leading to sluggish demand.

Shagang Steel kept its long steel product prices unchanged for early June. Among them, rebar (16-25mm) was priced at 3,400 yuan/tonne ($503/tonne), wire rod (8-10mm) at 3,530 yuan/tonne ($523/tonne), and wire rod (6-10mm) at 3,440 yuan/tonne ($509/tonne).

Raw material prices showed divergent trends. The benchmark iron ore fines (62% Fe) price fell by $3/dry metric tonne week-on-week to $102/dry metric tonne CFR China on June 5. Market sentiment was weak, with high coke prices squeezing steel mill margins and limiting raw material procurement, while increased miner shipments and inventory liquidation further pressured prices. Additionally, weakening expectations for steel demand during the construction off-season and concerns over increased iron ore supply from Guinea's Simandou project also drove prices lower. The spot premium for 65% Fe pellets was $19.45/tonne CFR China (June 3), up $1.6/tonne week-on-week. The spot lump ore premium fell by $0.006/dmtu week-on-week to $0.1765/dmtu (June 5).

China's coking coal and coke markets remained firm, supported by strict mine safety inspections, slow supply recovery, and strong downstream demand. The fifth round of coke price hikes (50-55 yuan/tonne, approximately $7-8/tonne) has been fully implemented, with low inventories and rising pig iron production continuing to support the market. Market participants anticipate a sixth round of coke price increases, maintaining a bullish sentiment. Meanwhile, as of June 5, Australian premium hard coking coal (PHCC) prices rose by $2/tonne week-on-week to $243/tonne FOB. Reflecting international market trends, BigMint's PHCC index edged up $1/tonne to $269/tonne CNF Paradip, India.

Chinese billet prices were largely stable, at 3,020 yuan/tonne ($448/tonne) on June 5, compared to 3,010 yuan/tonne ($444/tonne) on May 29. Prices rose to 3,030 yuan/tonne ($448/tonne) early in the week, supported by coke price increases, firm iron ore values, and supply concerns following stricter safety inspections, but gains were subsequently capped by weak seasonal demand, rising inventories, and sluggish trading activity. Chinese billet export offers rose to $474/tonne FOB, supported by stronger raw material costs and expectations of price hikes from major mills, but weak overseas demand limited export activity.

Looking ahead to the coming days, China's domestic steel market is expected to maintain range-bound fluctuations. Seasonal demand weakness may continue to weigh on prices, while changes in steel production and inventory levels will be closely monitored. Cost support and supply adjustments may help limit any significant downside.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com