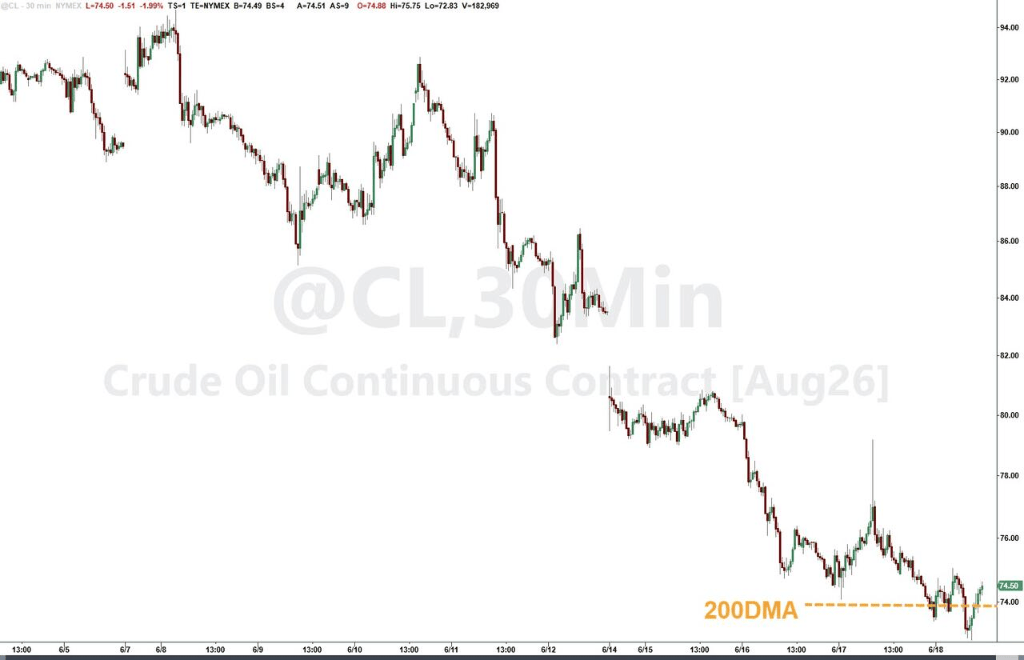

en.Wedoany.com Reported - After the U.S.-Iran interim peace agreement took effect, the Strait of Hormuz resumed navigation, with multiple supertankers crossing the strait. The return of crude oil supply expectations pushed energy prices downward. U.S. Vice President Vance announced at a White House press conference that the 60-day negotiation window stipulated in the memorandum of understanding signed by U.S. President Trump and Iranian President Pezeshkian has officially begun. The Trump administration declared that the U.S. military has lifted all maritime blockades against Iran. Within hours of the agreement's signing, three Saudi-flagged supertankers passed through the Strait of Hormuz. Trump posted on Truth Social that oil is flowing, Iran can never have nuclear weapons, and the stock market is roaring. U.S. Vice President Vance downplayed concerns that Iran might impose transit fees. WTI crude oil futures settled at $76.60 per barrel, hitting lows seen before the Iran war, recording the largest single-week drop in nearly two months this week.

Ian Lyngen of BMO Capital Markets stated that improved prospects for oil supply in the Persian Gulf supported stock prices, while lower energy costs eased forward inflation expectations and led to a meaningful decline in long-end U.S. Treasury yields. Fawad Razaqzada of Forex.com believes that if energy costs continue to feed into inflation data, inflation should gradually moderate in the coming months, potentially allowing the Federal Reserve to maintain its current policy stance without implementing a new round of tightening.

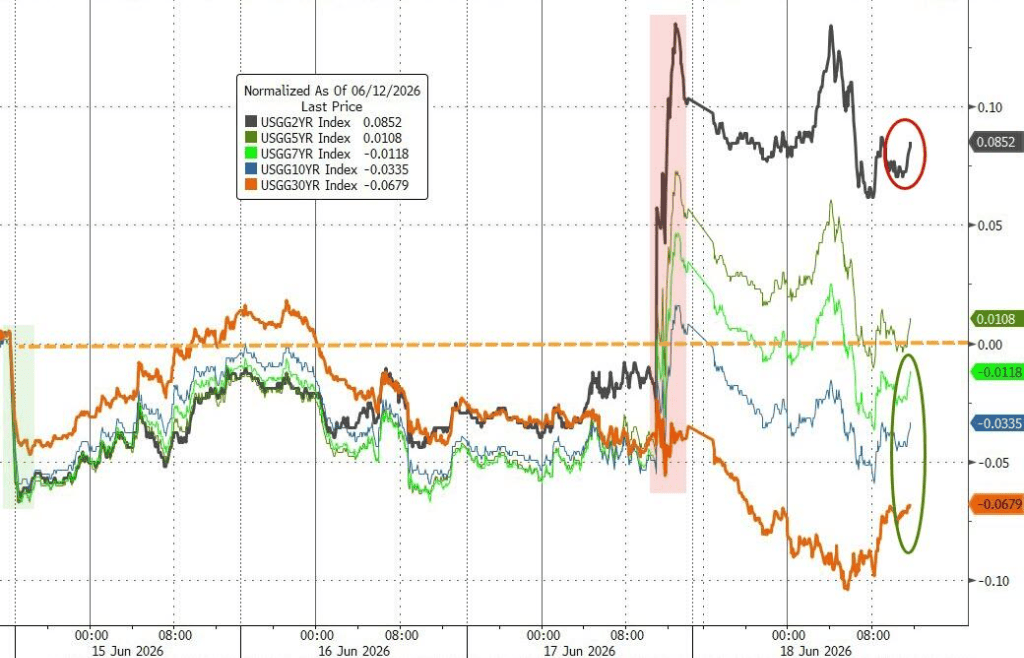

The easing effect of falling oil prices on inflation offset pressure from the Fed's policy shift. Long-end yields fell alongside oil prices, while short-end rates still faced significant upward pressure. The 10-year U.S. Treasury yield dropped 3 basis points to 4.45%, partially absorbing the hawkish impact from Fed Chair Warsh overnight. Bloomberg analyst Simon White noted that excess liquidity turned negative for the first time since 2021 and continues to decline, posing a growing headwind for stocks, with financial conditions clearly tightening.

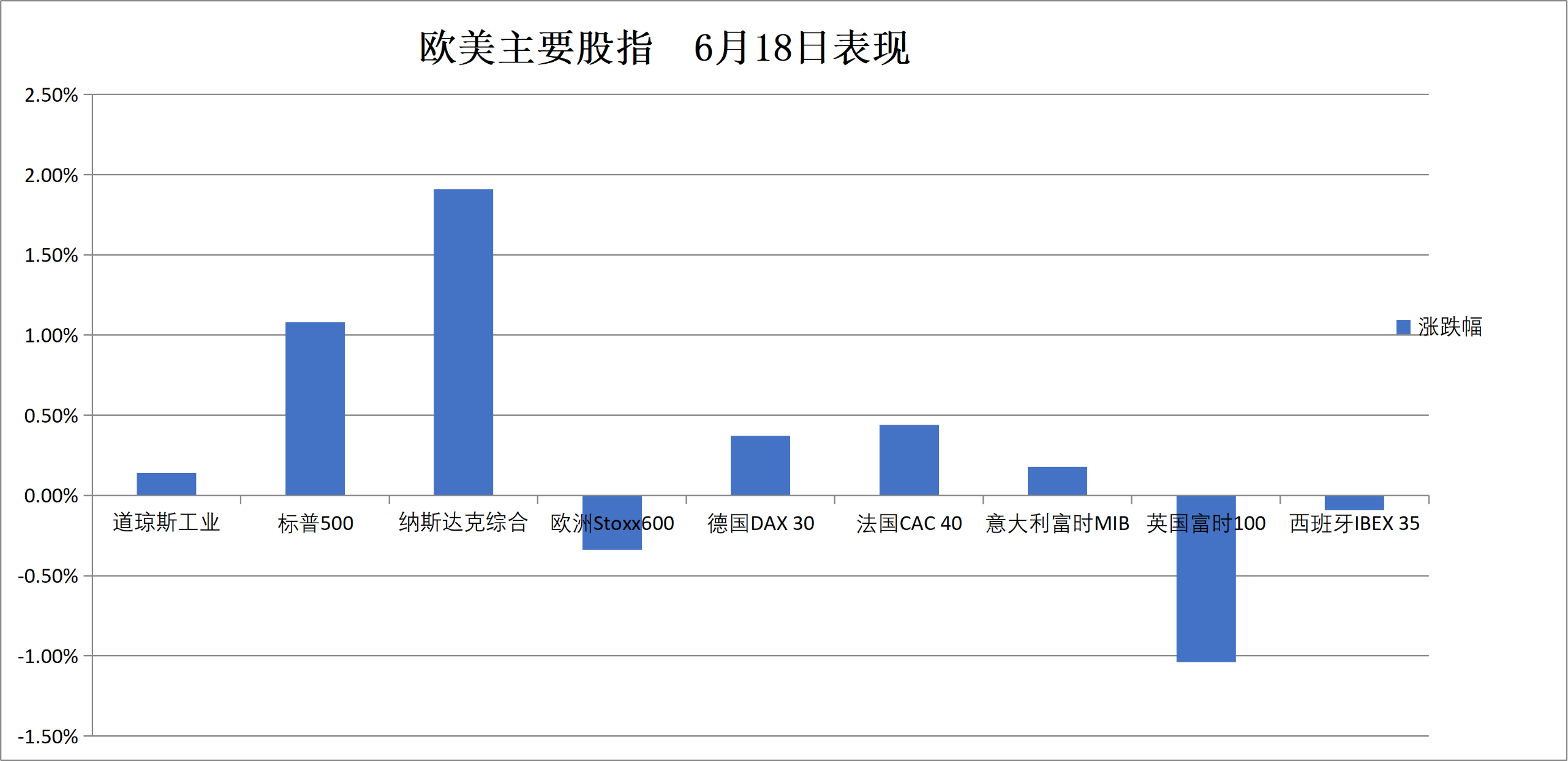

On Thursday, the S&P 500 closed up 80.48 points, or 1.08%, at 7,500.58. The Nasdaq 100 closed up 735.246 points, or 2.48%, at 30,406.194. Chip stocks led gains, with the Philadelphia Semiconductor Index closing up 864.711 points, or 6.42%, at 14,341.784, breaking its all-time closing high set on June 15. The Russell 2000 closed up 2.12% at 2,979.766, also breaking its all-time closing high from June 15. The VIX volatility index closed down 11.06% at 16.40. Trading volume on U.S. exchanges surged to a record high on Thursday, driven by over $7.5 trillion in options expirations. The trading week was shortened due to the Juneteenth holiday on Friday, with the Nasdaq ultimately becoming the only major index to fully recover from the losses caused by Warsh's hawkish statement.

Artificial Intelligence once again became the market's main theme, with bargain hunters flooding in and the semiconductor sector leading gains. Goldman Sachs partner Bobby Molavi pointed out that the market remains narrow and concentrated, driven by a single factor (momentum) and a single theme (AI computing and storage), continuously overcoming various challenges. However, corporate attitudes toward AI investment are shifting from "experimentation at any cost" to "cost-conscious focus on ROI."

At the individual stock level, SpaceX fell for a second consecutive day after its IPO, but its stock price remains well above the offering price, still up nearly 15% for the week. Tech stocks led gains this week, while the industrial sector also performed strongly, and energy stocks were the worst performers.

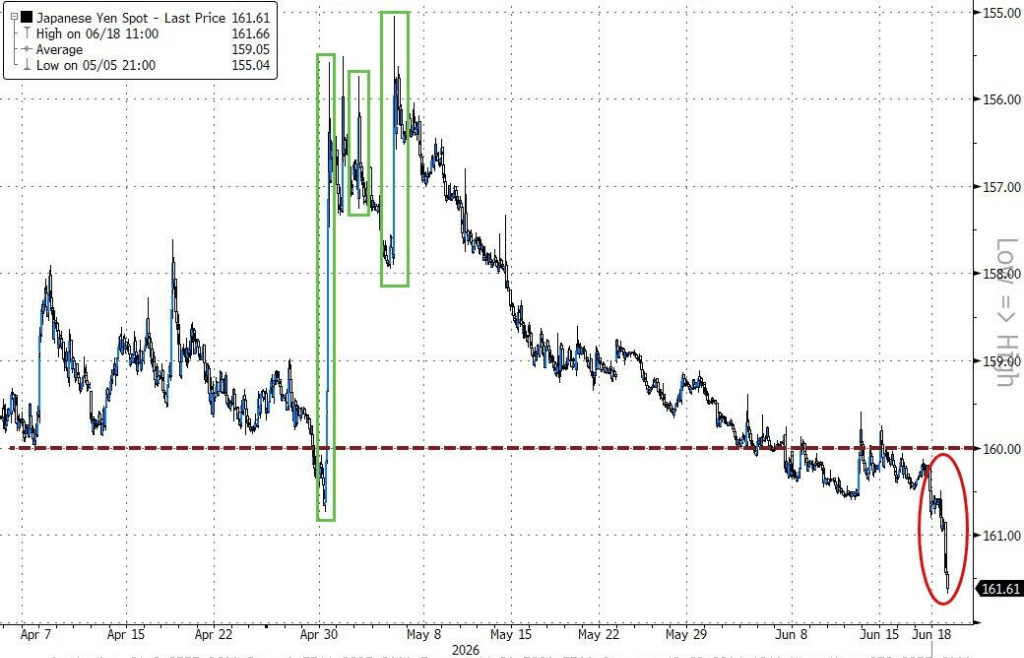

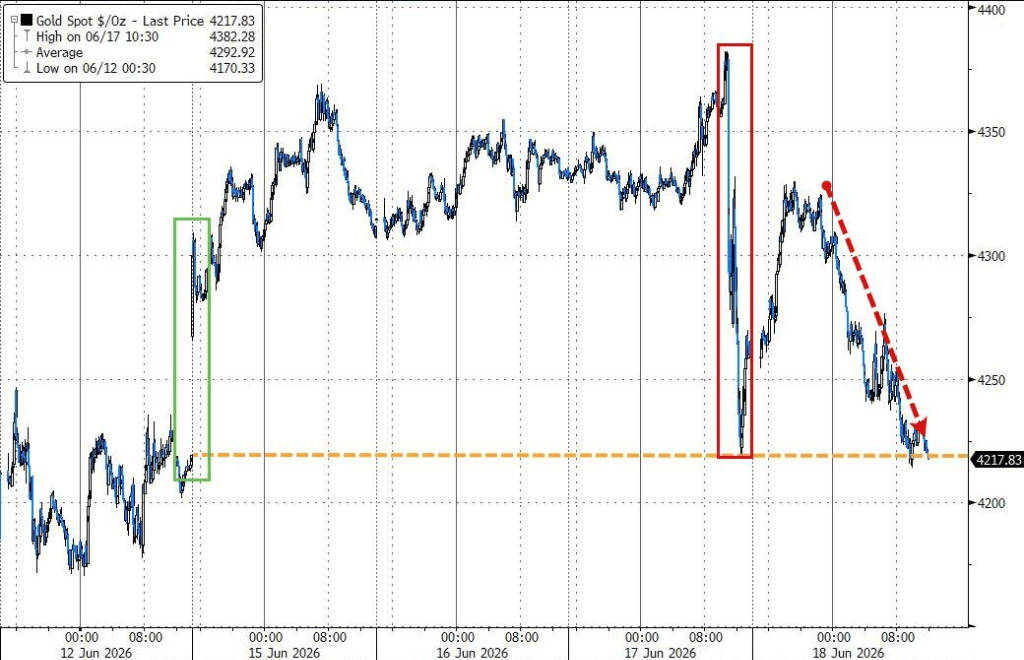

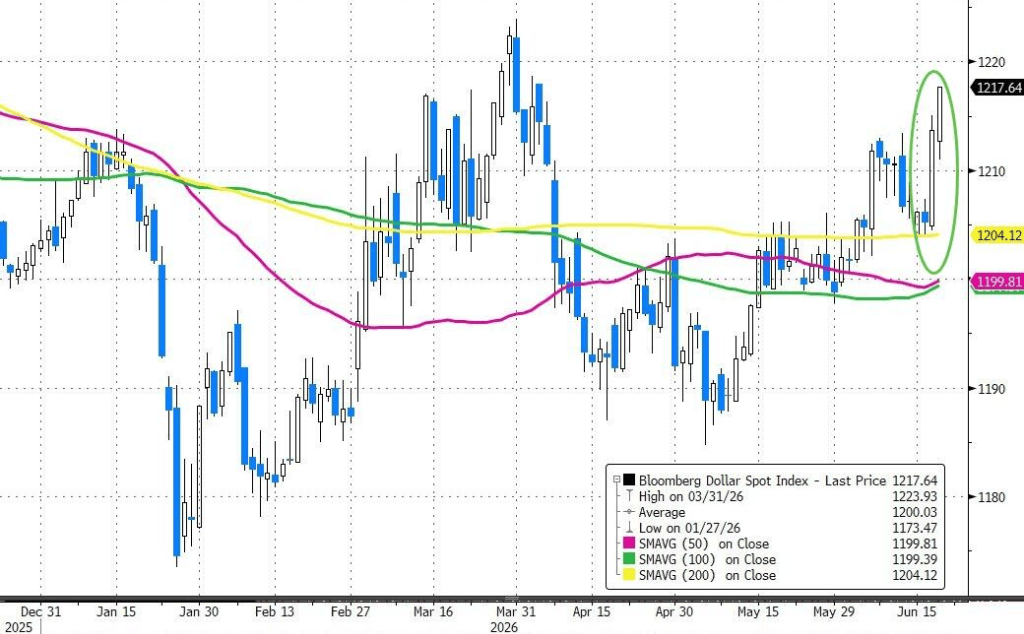

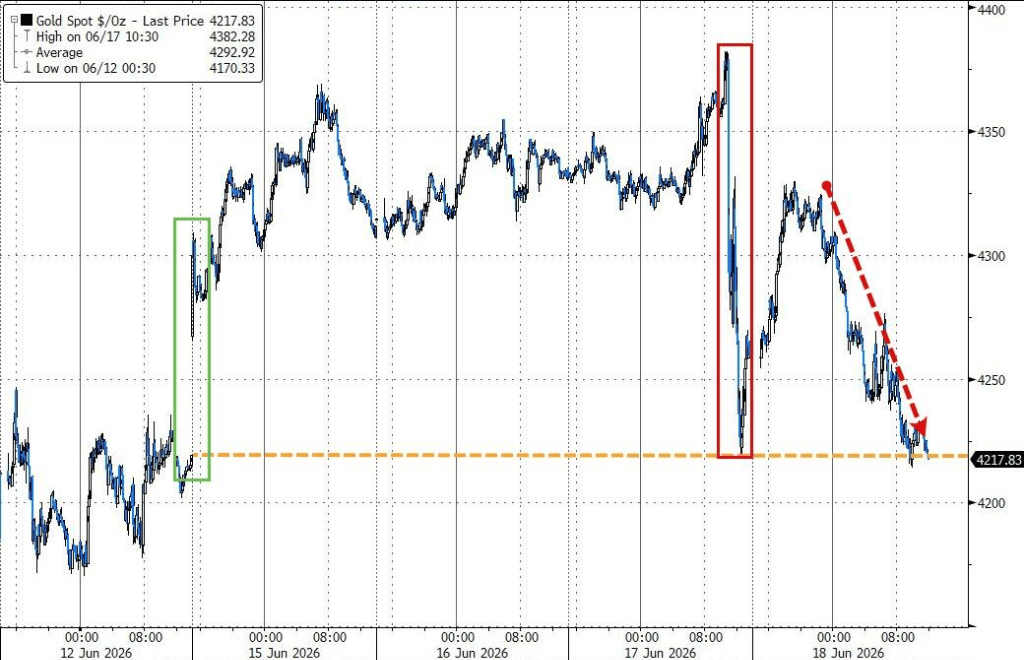

The U.S. dollar index recorded its largest two-day gain in three months this week, surging after a strong rebound from its 200-day moving average. The yen weakened past the 161 level against the dollar, prompting intervention warnings from Japanese officials. Spot gold fell 0.9% to $4,216.58 per ounce, and Bitcoin fell 1.9% to $63,124.21, both failing to follow the stock market rebound and remaining under pressure from a strengthening dollar.

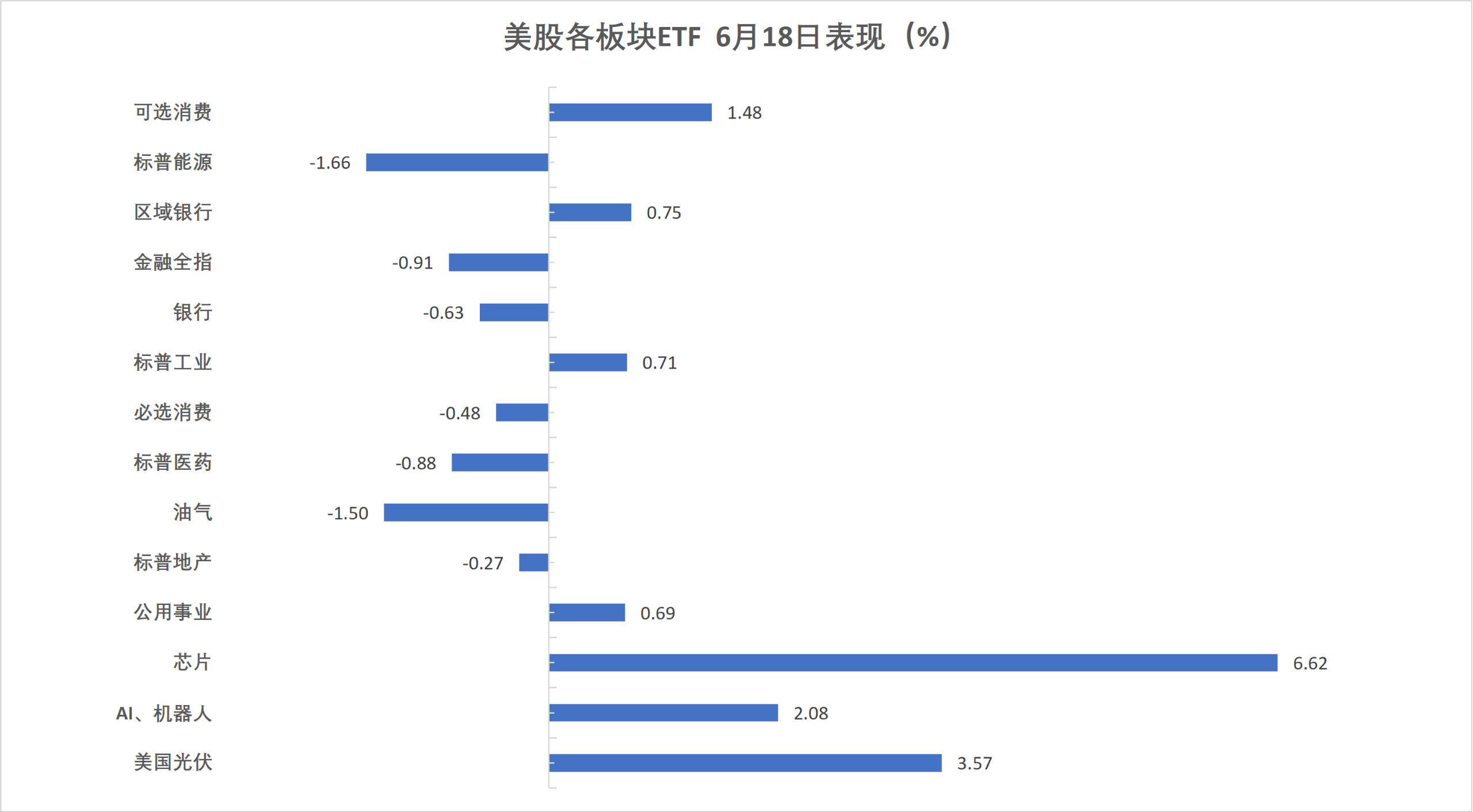

On Thursday, the Nasdaq Tech Index closed up over 3.2%, the Semiconductor Index rose over 6.4%, and small-cap indices hit record closing highs. Nvidia rose 2.95%. After Trump stated that Intel would partner with Apple to produce chips, Intel surged nearly 11%. Apple may raise prices due to high memory and storage chip costs, with SanDisk rising over 11% and Micron up nearly 9%. Among U.S. industry ETFs, the Semiconductor ETF rose 5.76%, the Global Tech Index ETF, Tech Sector ETF, and Global Airline ETF rose up to 3.75%, the Internet Index ETF rose 1.11%, while the Healthcare ETF and Financial ETF fell up to 0.89%, and the Energy ETF fell 1.65%. The U.S. Tech Mega-Cap Seven Index rose 1.52% to 213.40 points, with Nvidia up 2.95%, Amazon up 2.90%, Meta up 1.70%, Google A up 1.17%, Tesla up 1.04%, Apple up 0.70%, and Microsoft up 0.13%. The Philadelphia Semiconductor Index closed up 864.711 points, or 6.42%, at 14,341.784, breaking its all-time closing high set on June 15. TSMC ADR rose 6.86%, and AMD rose 10.02%. The Nasdaq Golden Dragon China Index closed down 0.88% at 6,068.15 points, with 21Vianet down 4.8%, GDS down 4.3%, Kingsoft Cloud down 3.1%, New Oriental down 1.3%, and Alibaba down 0.2%. Among other stocks, Circle fell 0.48%, SpaceX closed down nearly 3.6%, and Accenture fell 18% due to concerns that AI is reducing consulting demand.

European stocks fell from all-time highs, while the Eurozone blue-chip index continued to hit record highs. Italian stocks and the banking sector continued to set new closing highs, the UK index fell 1%, and the defense ETF fell over 2.7%. The European STOXX 600 index closed down 0.34% at 637.14 points, ending a streak of five consecutive days of gains and record highs. The Eurozone STOXX 50 index closed up 0.37% at 6,323.27 points, hitting record closing highs for five consecutive days, accumulating a gain of 5.21% over the last six days. Germany's DAX 30 index closed up 0.37% at 25,026.80 points, France's CAC 40 index closed up 0.44% at 8,467.98 points, and the UK's FTSE 100 index closed down 1.04% at 10,399.70 points. Among Eurozone blue chips, Infineon closed up 6.42%, Siemens Energy up 4.70%, and Safran, Schneider Electric, Adidas, Airbus Paris, and Hermès rose between 2.92% and 2.05%, ranking among the top seven performers. Among all components of the European STOXX 600, Capgemini closed down 8.87%, Saipem down 7.34%, Hochschild Mining down 7.29%, the London Stock Exchange had the fourth-largest decline, and Kering rose 4.40%.

In the U.S. Treasury market, the 10-year yield fell 3.16 basis points to 4.4553% at the New York close, trading in a range of 4.4770% to 4.4178%. The 2-year yield fell 0.56 basis points to 4.1788%. In the European bond market, the German 10-year yield rose 0.2 basis points to 2.929% at the European close, trading in a range of 2.945% to 2.916%. The UK 10-year yield rose 0.6 basis points to 4.757%.

After the Fed's hawkish stance, the U.S. dollar index continued to rise, hitting a one-year high. At the New York close, the ICE U.S. Dollar Index rose 0.81% to 100.909 points, approaching the May 16, 2025 high of 101.259 points, accumulating a gain of 1.36% over the last two trading days. The Bloomberg Dollar Index rose 0.37% to 1,218.35 points, approaching the March 31 high of 1,233.93 points, rising 1.08% over the last two days. The yen weakened over 0.57% against the dollar to 161.81, erasing gains since Japan's intervention in late April, hitting a nearly two-year low. The euro rose 0.2% against the yen to 185.09, while the pound fell 0.11% against the yen to 213.244. Offshore yuan traded at 6.7784 per dollar, up 22 points from Wednesday's New York close, trading in a range of 6.7624 to 6.7810. In cryptocurrencies, spot Bitcoin fell over 2% at the New York close, and Ethereum fell 2.1%.

Oil prices experienced a V-shaped move, with WTI crude falling over 4% intraday before erasing most losses, and Brent crude falling nearly 4% before turning positive. WTI crude for July delivery closed down $0.19 at $76.60 per barrel, a decline of 0.25%, falling nearly 10% for the week. Brent crude for August delivery closed up $0.30 at $79.85 per barrel, a gain of 0.38%. NYMEX July gasoline futures closed at $2.9949 per gallon, NYMEX July heating oil futures closed at $3.1273 per gallon, and NYMEX July natural gas futures closed at $3.2330 per million British thermal units.

Gold and silver plunged sharply, with gold futures, which had risen for four consecutive days, falling over 3% intraday before a narrow rebound for the week. At the New York close, spot gold fell 1.10% to $4,210.35 per ounce, and COMEX gold futures fell 3.41% to $4,232.00 per ounce. Spot silver fell 3.27% to $65.7071 per ounce, falling for six consecutive weeks, the longest weekly losing streak in three years, and COMEX silver futures fell 3.09% to $66.385 per ounce. At the New York close, COMEX copper futures fell 1.76% to $6.4425 per pound, spot platinum fell 2.40%, and spot palladium fell 2.79%. LME copper closed down $124 at $13,690 per ton, LME tin closed down $1,691 at $53,653 per ton, and LME nickel closed down $218 at $17,842 per ton.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com