en.Wedoany.com Reported - The National Coil Coating Association (NCCA) gathered coil coaters and suppliers at its annual meeting to discuss economic and industry trends. In a keynote address, Dr. Anirban Basu of Sage Policy Group, Inc. noted that US GDP growth is expected to be 1.5%–2.5% in 2026, but discussions of a recession will increase. From May 2020 to May 2026, US inflation was significant, with energy prices rising by up to 74.4%, while overall prices increased by approximately 29.1% over the same period. Meanwhile, the job market is unstable, loan delinquency rates have surged, and consumer repayment is lagging.

Basu stated that despite a persistent housing shortage, high material and labor costs, along with worker shortages, have led to a decline in new construction investment. Commercial building construction spending is also declining, with high vacancy rates in major cities. The 2026 GDP growth forecast faces risks such as rising inflation, high interest rates, and overexpansion of assets, with most consumers financially strained.

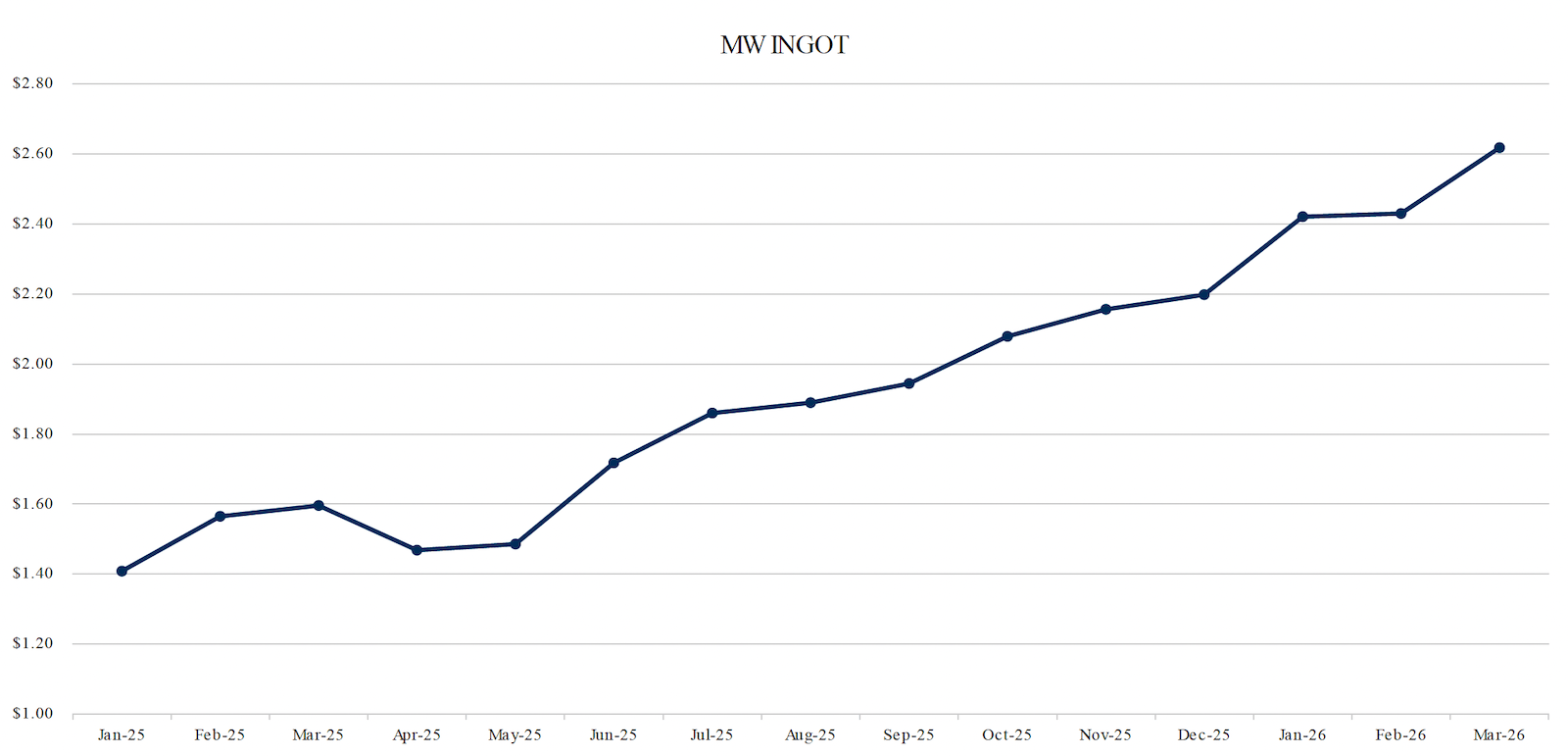

In the aluminum panel, Cameron Clark of Midwest Metals explained that the London Metal Exchange (LME) pricing and the Midwest premium together determine the cost of coil on the coating line, with the Midwest premium including freight, handling, warehousing fees, and tariffs, as presented by Platts and other price reporting agencies. From January 2025 to March 2026, the average LME price rose by 30%, while the Midwest premium surged by 350%, resulting in a total increase of over 80% in the Midwest aluminum ingot price. The cost of a 40,000-pound batch of aluminum ingot rose from $56,329.16 to $104,716.40, an increase of $48,387.24, driven by Section 232 tariffs, sanctions on Russian aluminum, and the Iran conflict. These increases have led to higher inventory costs, increased credit risk, potential project delays, and a market shift toward alternative products such as aluminum composite material (ACM) panels. Anti-dumping (AD) and countervailing duty (CVD) scope rulings will affect imported ACM panels, potentially leading to a decline in North American demand for aluminum, coil coatings, paints, and other chemicals.

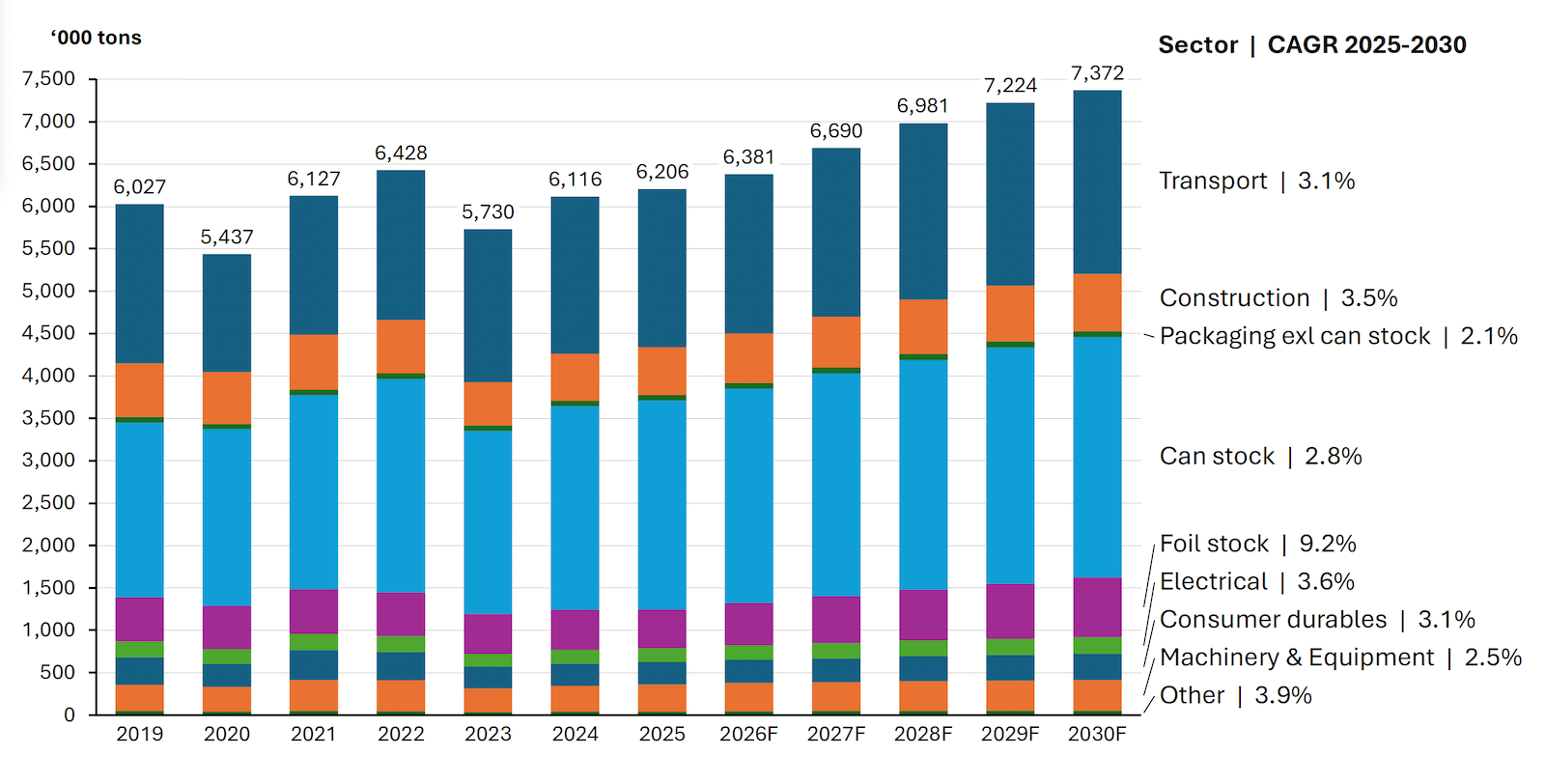

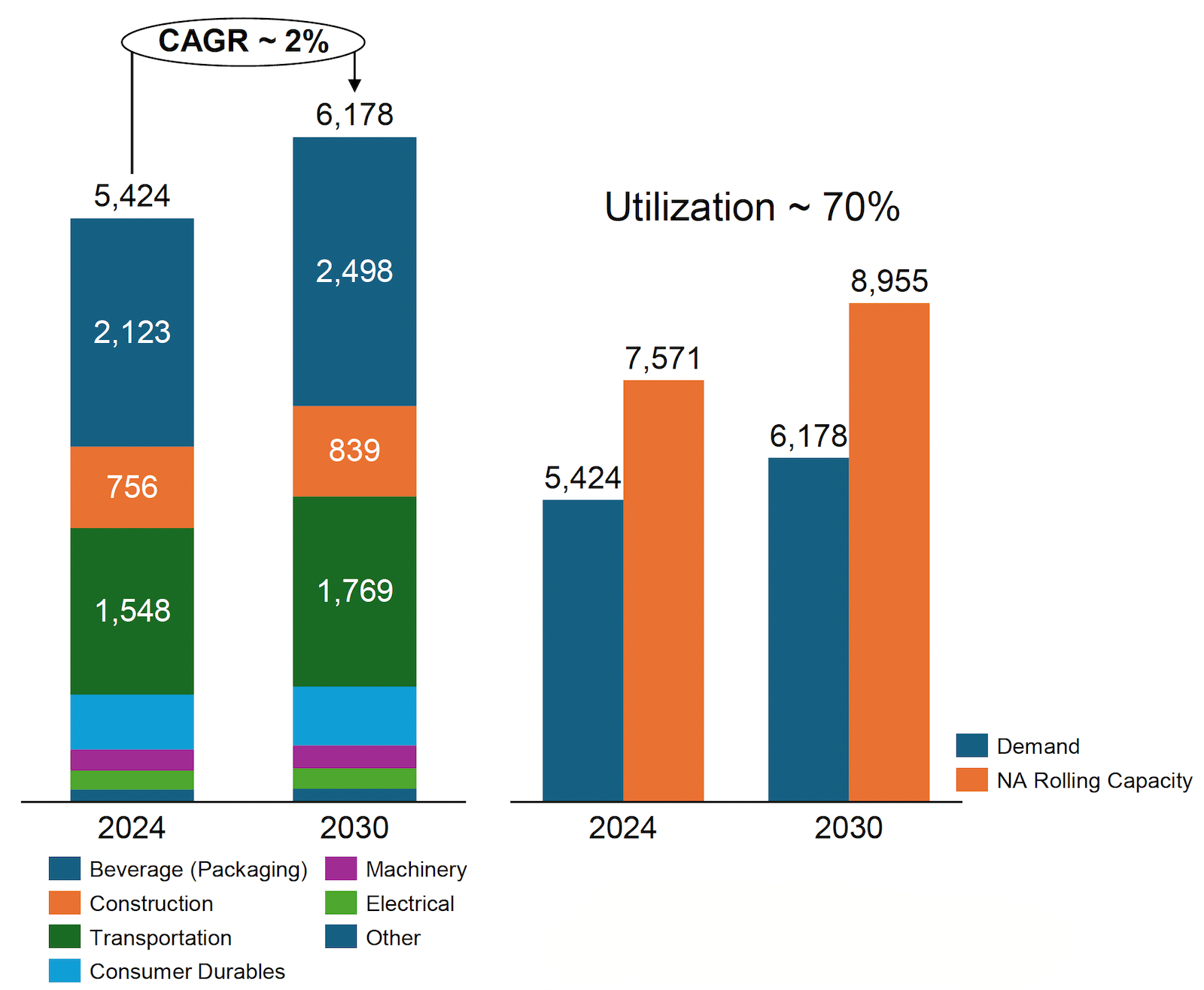

In a presentation on the import landscape, James Parks of Jupiter Aluminum noted that the Iran conflict has disrupted supply from the Middle East region (which accounts for approximately 27% of global primary aluminum supply, excluding China and Russia), with the market immediately reacting with a surge in aluminum prices. The Aluminum Association is studying ways to improve worker safety, find alternative metal sources, and increase domestic recycling. Davide Ricci of Novelis stated that North American demand for flat-rolled aluminum products continues to grow, with can stock as the primary driver. The company is investing $5 billion in the Bay Minette rolling mill, which will create 1,000 new jobs and produce 600,000 tons of finished products annually. Cold commissioning of the cold rolling mill is expected to be completed in the second half of 2026, with the hot rolling mill starting production in 2027.

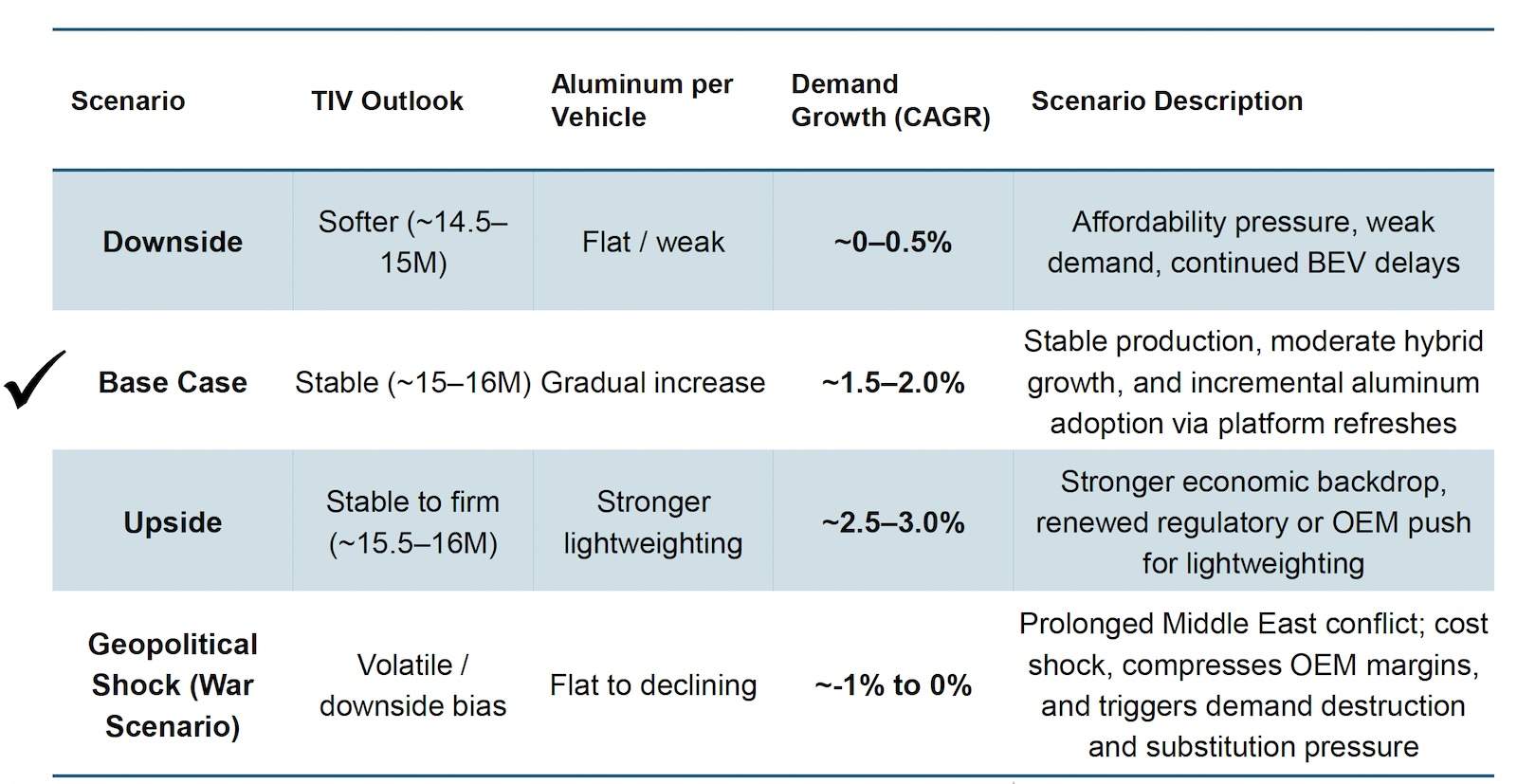

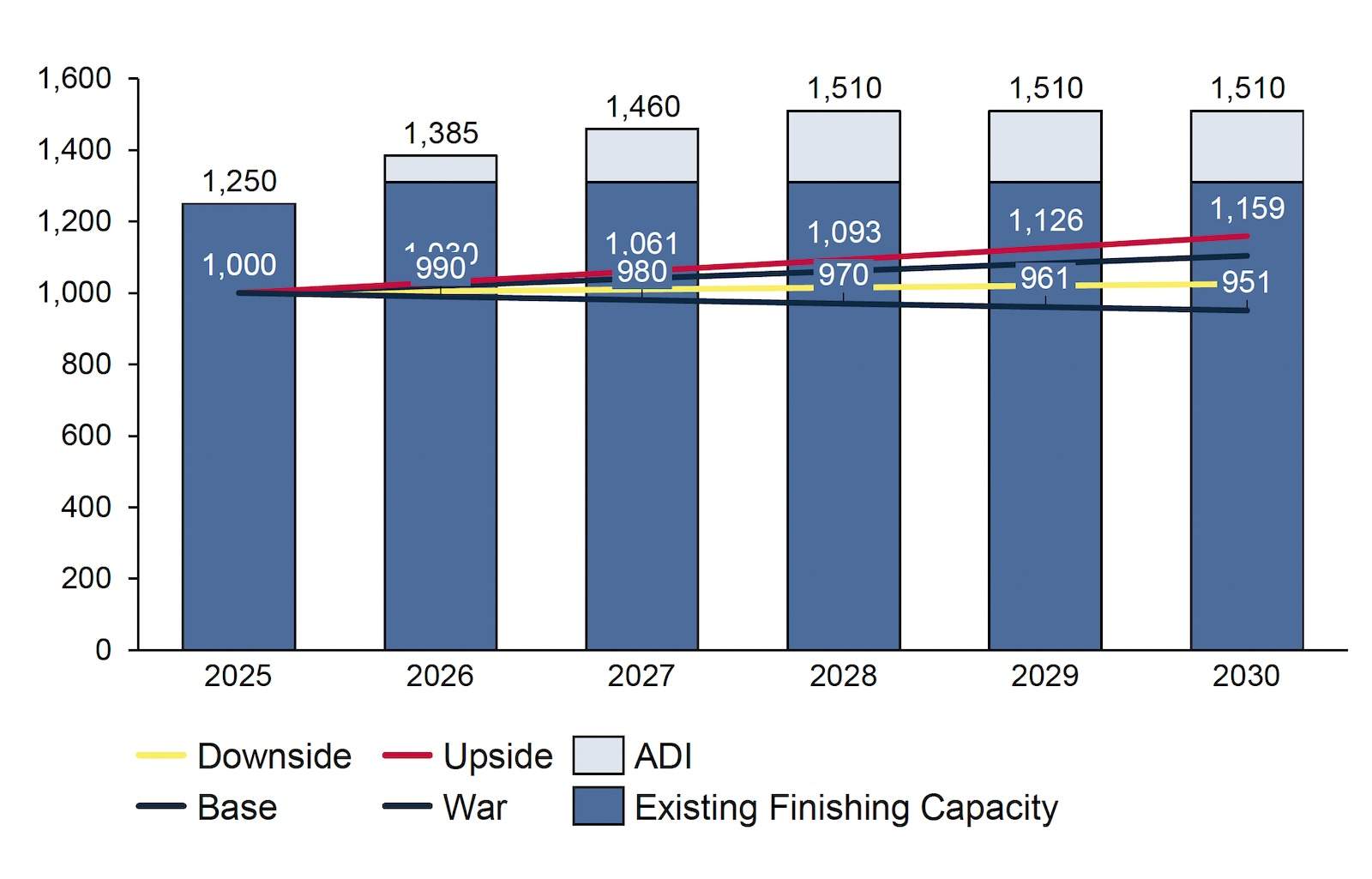

Kaustubh Chandorkar of Chandorkar Consulting LLC assessed end-market trends, noting that annual automotive production is stable at 15-16 million vehicles, with electric vehicle plans shelved due to the reversal of CAFE standards. Aluminum demand is relatively stable in the short term, but the longer high prices persist, the more likely substitution becomes. Automotive aluminum projects remain stable, with a base growth rate of 1.5-2% in aluminum usage per vehicle. In 2025, North America has approximately 1.25 million tons of continuous annealing line with pretreatment (CALP) coating capacity. With Aluminum Dynamics starting two CASH lines, total coating capacity is expected to increase to 1.5 million tons, sufficient to meet body panel demand. The food and beverage packaging market is expected to grow at a rate of 2-4%, but the US recycling rate for used beverage cans is only 43%. The construction market is stabilizing, with no significant growth in the short term.

The employee retention education workshop was hosted by Tracy Adams of Sherwin Williams. The current industry landscape faces high employee turnover rates (26-28%), labor shortages (over 5% of manufacturing positions vacant), and declining engagement (25% of workers are over 55). High turnover costs range from $7,800 to $11,900. Developing existing employees can be achieved through training and upskilling programs (40-50 hours of training per year is a good investment), creating career development paths, offering mentorship, and implementing retention frameworks. Mentorship helps reduce early-career departures (first 90-180 days). A retention framework should include recognition and communication, career development and a safe environment, flexible scheduling, and an inclusive culture. Additionally, automation is a viable option to reduce employee numbers, with approximately 60% of manufacturing operations able to automate at least 30% of tasks, and automation is expected to create 97 million new roles.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com