en.Wedoany.com Reported - The Democratic Republic of the Congo (DRC) recently announced that unused mining company export quotas for the first half of 2026 will automatically expire and be transferred to the strategic quota pool of the Strategic Minerals Market Regulatory Authority (ARECOMS). Boosted by this news, electrolytic cobalt prices stopped falling and rebounded, but the overall weak market demand trend remains unchanged.

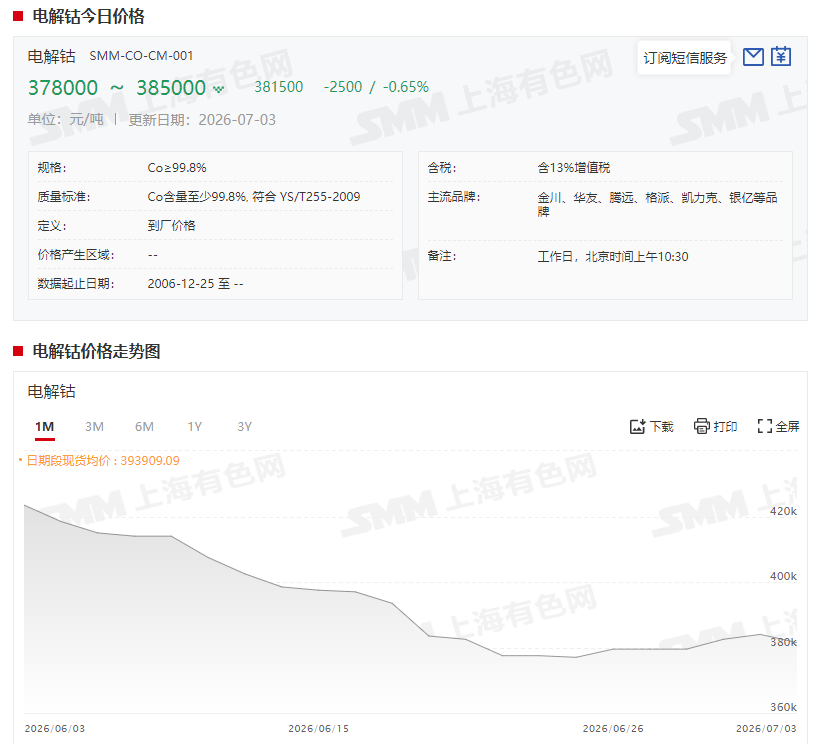

As of July 3, the spot price of electrolytic cobalt ranged from 378,000 to 385,000 yuan per ton, with an average price of 381,500 yuan per ton, up 2,000 yuan per ton from 379,500 yuan per ton on June 26, an increase of 0.53%. Mainstream smelters' ex-factory prices remained stable at 385,000 yuan per ton, with market basis trading in a range from flat to a premium of 10,000 yuan per ton. Inquiry activity from downstream end-users picked up slightly, but transactions were mostly for just-in-time advance stocking, and a substantive recovery in end-user demand has not yet materialized. Short-term downstream demand support is insufficient, coupled with high industry inventory levels, suggesting the market may continue to fluctuate.

Spot prices of cobalt sulfate remained stable after a slight decline on the first day, quoted at 85,000 to 87,000 yuan per ton as of July 3, with an average price of 86,000 yuan per ton, down 150 yuan per ton from June 26, a decrease of 0.17%. Primary smelter quotes were generally firm, with mainstream enterprises holding the minimum selling intention price at 85,000 yuan per ton. Boosted by the policy news, the willingness of some recycling smelters and traders to cut prices and offload inventory weakened, with low-priced supply quotes rising from 80,000 to 81,000 yuan per ton last week to 82,000 to 83,000 yuan per ton. Downstream companies generally adopted a production-based-on-sales model, with most enterprises maintaining a wait-and-see stance in early July, and substantive restocking likely postponed to mid-to-late July.

Spot prices of cobalt chloride fluctuated downward, falling to 102,500 to 104,000 yuan per ton as of July 3, with an average price of 103,250 yuan per ton, down 2,000 yuan per ton from 105,250 yuan per ton on June 26, a decrease of 1.9%. On Tuesday, the DRC announced the cancellation of unused quotas for the second quarter of 2026. This news only caused minor market fluctuations in the morning, calming down by the afternoon, indicating that market focus has shifted from supply-side disruptions to fundamentals and demand conditions. Smelter quotes began to stabilize, with some companies slightly raising prices to test the market. Although downstream inquiries increased, actual transactions were limited. Short-term cobalt chloride prices are expected to remain stable, with limited room for further declines.

Spot prices of cobalt tetroxide continued to fall, dropping to 315,000 to 330,000 yuan per ton as of July 3, with an average price of 322,500 yuan per ton, down 12,500 yuan per ton from 335,000 yuan per ton on June 26, a decrease of 3.73%. The market remained extremely sluggish, with very few actual transactions. After the mid-report window, most bearish companies had completed their shipments, and quotes stabilized this week. Downstream cathode material manufacturers remained on the sidelines, maintaining strong price pressure on purchases. Future trends still need to focus on the price direction of cobalt salts.

Spot prices of cobalt intermediate products (CIF China) fell slightly, quoted at $24.25 to $25.50 per pound as of July 3, with an average price of $24.875 per pound, down $0.25 per pound from $25.125 per pound on June 26, a decrease of 0.1%. Mainstream miners' offers remained firm at around $25.50 per pound, while the minimum selling price for small batches from some traders stabilized near $24.00 per pound. Calculated backward from current cobalt salt spot prices, the acceptable raw material purchase price for downstream smelters is only around $23.00 per pound, indicating a significant price gap between buyers and sellers. Short-term demand support from downstream smelting is weak, and intermediate product prices are likely to continue consolidating sideways.

The DRC, based on the Strategic Minerals Market Regulatory Authority (ARECOMS) press release No. 2026/003, announced that unused quotas for the first half of 2026 will be canceled and reallocated to the strategic quota pool. SMM estimated China's cobalt intermediate product supply (including some high-cobalt recycled supplementary materials) based on two assumptions: Assuming China imports 46,000 metric tons of cobalt metal in cobalt intermediates from June to December 2026, with domestic production of about 500 tons; in 2027, assuming mining companies allocate 80% of the 87,000 metric tons of cobalt intermediate quota to China, imports would be about 70,000 metric tons of cobalt metal, with domestic production of about 1,000 tons. With high economic viability leading to a significant increase in China's recycled cobalt production, considering supplementing some high-quality recycled cobalt as intermediates, the supplement would be about 18,000 metric tons of cobalt metal from June to December 2026, and about 36,000 metric tons of cobalt metal in 2027. China's demand for cobalt intermediates from June to December 2026 is about 58,000 metric tons of cobalt metal, a slight surplus of 6,000 metric tons; demand in 2027 is about 105,000 metric tons of cobalt metal, a slight surplus of 3,000 metric tons. This surplus remains uncertain: if mining companies reduce circulation to control intermediate product prices, the market could still face relative tightness; slow local approval progress may prevent full execution of basic export quotas. If imports fall short of expectations, the market could still face relative scarcity.