en.Wedoany.com Reported - According to the latest data from Omdia, the growth rate of China's semiconductor memory market in 2026 has been significantly revised upward to 262.9%, with the market size reaching $449.6 billion. China's semiconductor industry is fully entering an AI-driven technological era.

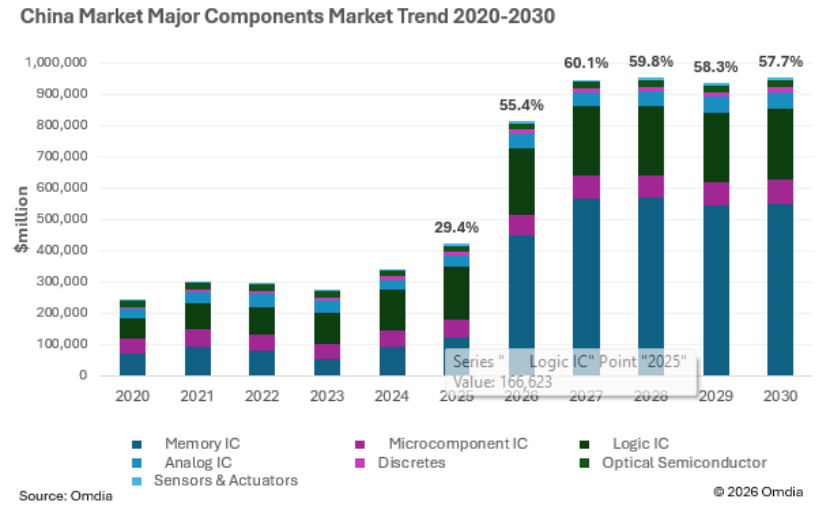

According to Omdia's "Semiconductor Application Market Forecast Tool (AMFT) - China Region, Q2 2026" report, by chip category, China's memory chip market share will grow from 29.4% in 2025 to 55.4% in 2026, and is expected to remain above half in the future. In 2026, the global semiconductor memory market size will reach $886.4 billion, accounting for 54.8% of the total market. AI infrastructure construction is the main driver of demand growth for semiconductor components. Cloud-based training and inference, as well as edge and endpoint inference, have significantly increased memory specifications and capacity requirements, further exacerbating the supply-demand tension in the memory market.

AI has also driven a growth rate of 27.9% for logic chips and 25.4% for analog ICs, particularly concentrated in high-end computing chips and high-specification power management chips related to servers. Microcontroller growth has also reached 15%, primarily driven by new application scenarios enabled by edge AI, especially physical AI. 2026 is being hailed as the year of AI inference explosion. Chinese domestic AI computing chip suppliers, leveraging their deep understanding of application scenarios, are providing more comprehensive hardware solutions at various levels of edge/endpoint computing. With the emergence of "chip-model synergy" opportunities, an increasing number of domestic AI models are closely coupling with local Chinese computing platforms in product definition and ecosystem co-building. The widespread adoption of AI is a significant boost to China's semiconductor industry foundation, especially against the backdrop of gradually expanding mature process and power device capacity, providing sufficient capacity demand for domestic chips.

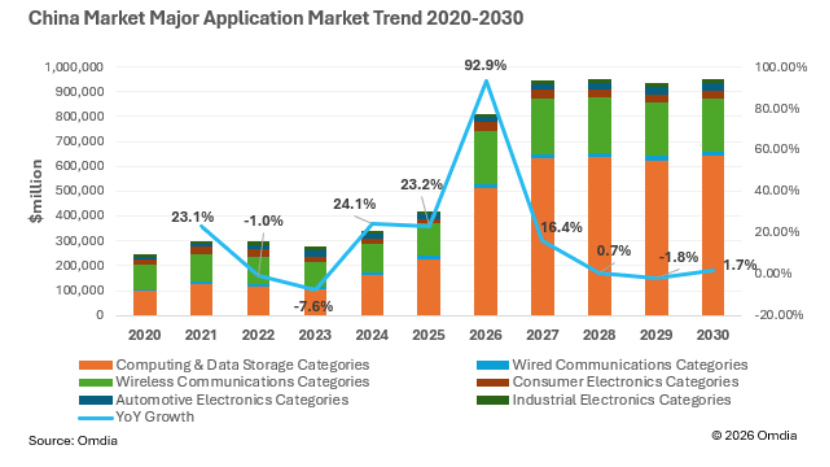

From the perspective of the global semiconductor market landscape, the global semiconductor market size will exceed $1.6 trillion in 2026, with the computing and storage category accounting for 60.7%. China's AI-related infrastructure construction will be carried out on a large scale in 2026, with the computing and storage category growing by 126%, accounting for 62.9% of the overall application market, indicating that the development pattern of China's semiconductor industry is now synchronized with the global market. In the wireless communications category, the growth rate is 68.8%, but the smartphone-dominated industry faces extreme conditions of sharply rising supply costs and accelerating contraction in shipments. This category's share of the overall market will decline from 30.43% in 2025 to 26.63% in 2026, and is expected to decline further in 2027.

According to China's Ministry of Industry and Information Technology, from January to May 2026, China's electronic information manufacturing industry experienced rapid production growth, stable export progress, and significantly improved efficiency. The added value of the electronic information manufacturing industry above designated size increased by 14.6% year-on-year, with growth rates 9.2 and 1.5 percentage points higher than the overall industry and high-tech manufacturing, respectively, for the same period. In May, the added value of the electronic information manufacturing industry above designated size increased by 17% year-on-year. Among major products, mobile phone production reached 562 million units, down 1.3% year-on-year, of which smartphone production was 477 million units, up 3.3% year-on-year; microcomputer equipment production was 119 million units, down 12.2% year-on-year; integrated circuit production was 228.6 billion units, up 25.4% year-on-year. From January to May, the cumulative export delivery value of the electronic information manufacturing industry above designated size increased by 6.1% year-on-year. According to customs statistics, during this period, China exported 42.6 million television sets, up 4.2% year-on-year; exported 272 million mobile phones, down 2.5% year-on-year; and exported 147.8 billion integrated circuits, up 8.7% year-on-year. From January to May, the electronic information manufacturing industry achieved operating revenue of 7.52 trillion yuan, up 17.1% year-on-year; total profit of 422 billion yuan, up 1.04 times year-on-year; and fixed asset investment increased by 6.7% year-on-year, 6.6 percentage points higher than the growth rate of industrial investment for the same period.

Data from the Semiconductor Industry Association (SIA) shows that global semiconductor sales in May 2026 were $120.6 billion, up 9.2% from April and 104.1% from May 2025, setting a new all-time monthly sales record and achieving the 15th consecutive month of sequential growth. SIA President and CEO John Neuffer stated that sales growth continues to be driven by strong year-on-year gains in the Americas, Asia-Pacific, and China. By region, year-on-year growth in May was: Americas 132.2%, Asia-Pacific/Other 118.9%, China 88.8%, Europe 60.7%, Japan 23.8%; sequential growth was: China 10.7%, Asia-Pacific/Other 9.2%, Americas 8.6%, Europe 7.3%, Japan 6.4%. The SIA formally endorsed the WSTS Spring 2026 global semiconductor sales forecast in June 2026, indicating that global annual sales will grow by 90% in 2026 to reach $1.5 trillion, and are expected to exceed $1.9 trillion in 2027. Logic chips and memory chips are the fastest-growing product categories. In 2025, logic chip sales reached $301.9 billion, up 39.9% year-on-year; memory chip sales reached $223.1 billion, up 34.8% year-on-year.