en.Wedoany.com Reported - The global semiconductor memory market is currently experiencing its steepest growth curve in history. According to data from the World Semiconductor Trade Statistics (WSTS), as of May 2026, monthly memory shipments had climbed to $63.3 billion, an increase of more than 11 times from approximately $5.6 billion in 2016, with a year-on-year growth rate of a staggering 285%, far exceeding any previous industry boom cycle.

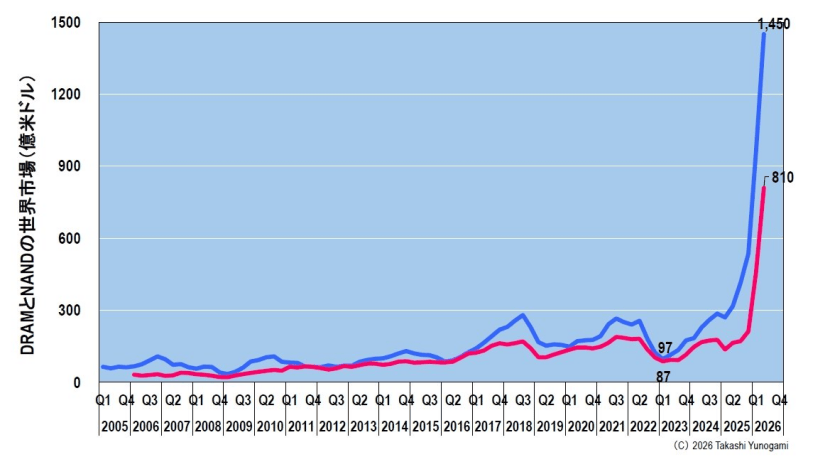

This growth is primarily driven by two major products: DRAM and NAND flash memory. According to data from research firm TrendForce, at the trough of the industry downturn in early 2023, the DRAM market size was only $9.7 billion, and NAND was $8.7 billion; it is estimated that by the second quarter of 2026, the DRAM market size will surge to $145 billion, and NAND to $81 billion, with a total quarterly amount of $226 billion, translating to an annual scale exceeding $900 billion. The DRAM and NAND markets have grown approximately 15 times and 9 times, respectively, from their lows in early 2023.

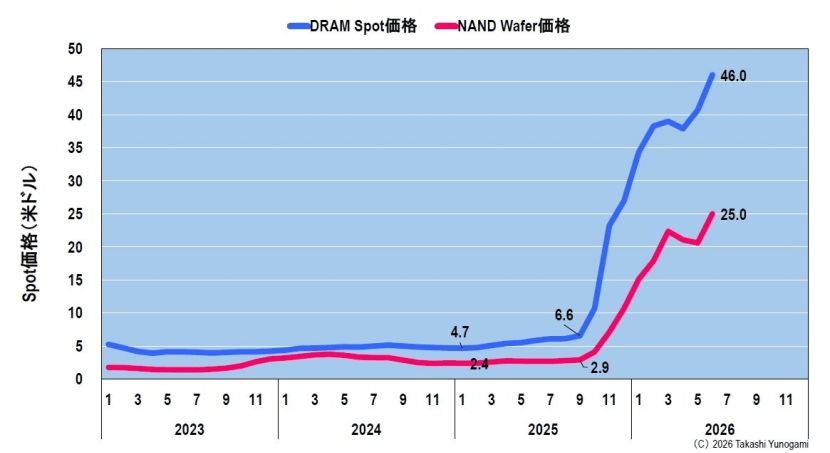

The core driver of this explosive market expansion is the abnormal surge in memory unit prices, rather than a proportional increase in shipment volumes. Data shows that the spot price of DDR5 16Gb 2Gx8 DRAM has risen from $4.70 in early 2025 to a recent $46.00, an increase of about 10 times; the price of 1Tb TLC NAND wafers has also risen from $2.40 to $25.00. The fundamental reason for the price surge is severe supply shortages, while the immense pressure on the demand side comes from the massive capital expenditures of hyperscale data center operators.

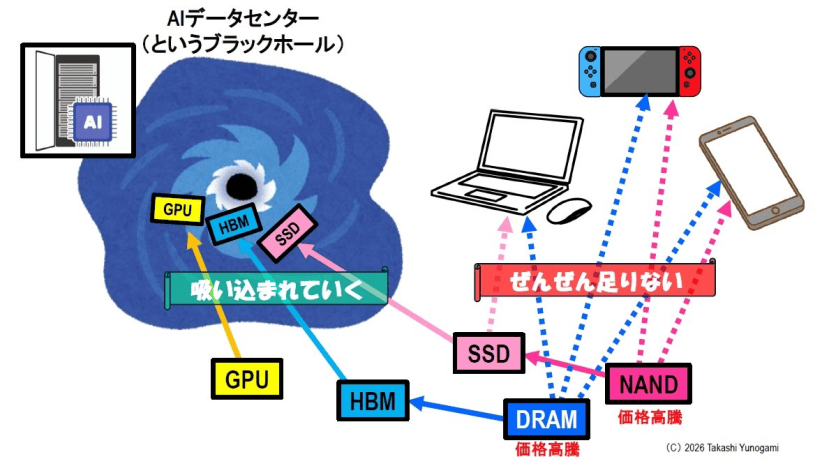

The total capital expenditures of the four major hyperscale data center operators—Amazon, Google, Microsoft, and Meta—are projected to rise from $21 billion in 2015 to $755 billion in 2026, an increase of about 36 times in just over a decade. These funds are primarily directed towards AI data centers, with large-scale procurement of GPUs from companies like Nvidia, high-bandwidth memory (HBM), and high-capacity SSDs. Memory manufacturers prioritize allocating production capacity to higher-margin AI products, leading to severe supply shortages of DRAM and NAND for consumer electronics sectors such as PCs, smartphones, and gaming consoles, further driving up overall memory prices.

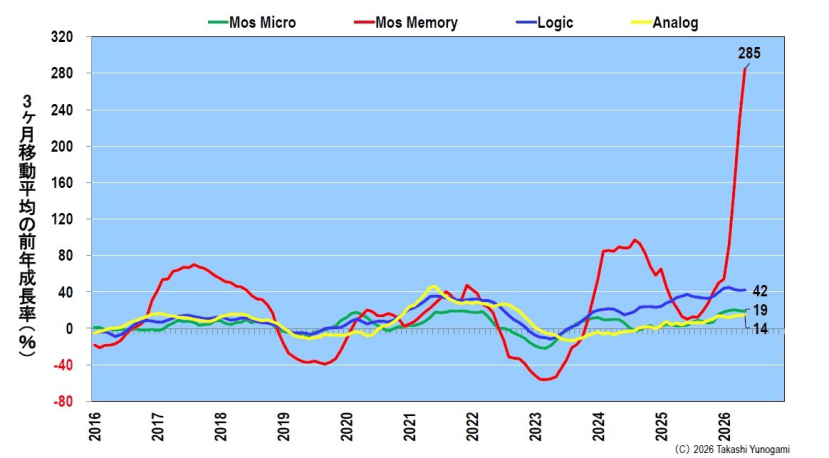

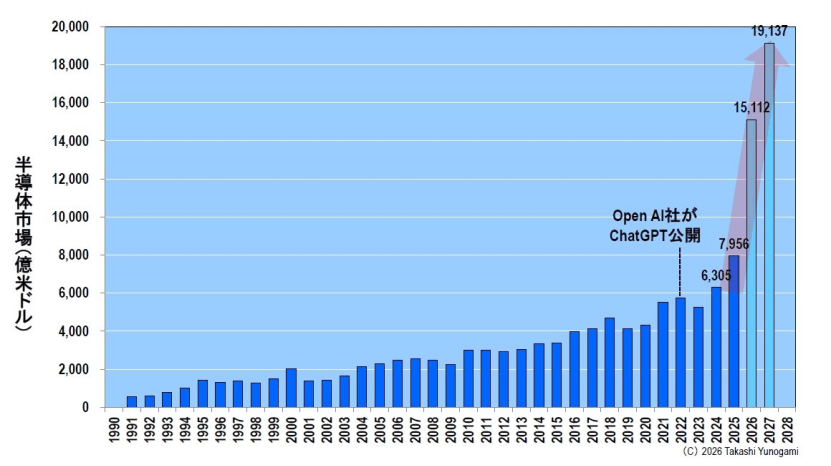

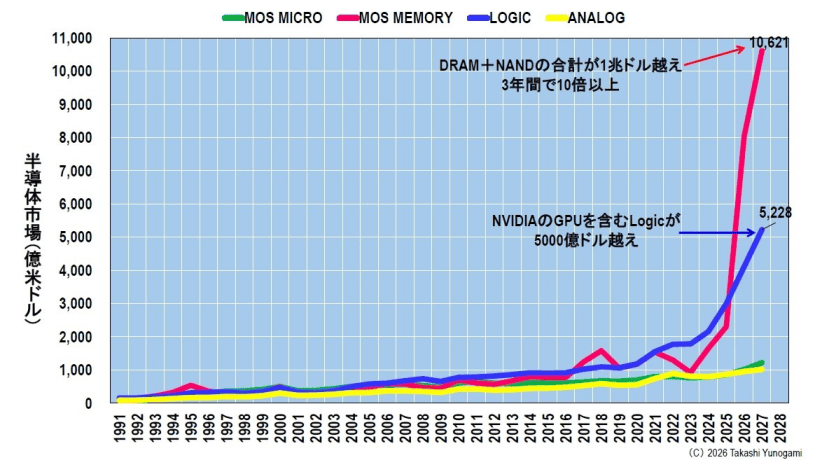

In its spring 2026 forecast, WSTS significantly raised market expectations: the global semiconductor market size was $630.5 billion in 2024, $795.6 billion in 2025, and is expected to surpass $1.5 trillion to reach $1.5112 trillion in 2026, further growing to $1.9137 trillion in 2027. Among this, the memory market is expected to exceed $1 trillion by 2027. This round of growth is mainly concentrated in two AI-related areas—memory and logic circuits—while the analog circuit and micro-semiconductor markets remain relatively stable, presenting a highly uneven growth structure.

Looking back at 35 years of historical data for the memory market, the longest sustained period of positive annual growth is only five years. This pattern stems from the "silicon cycle": surging demand drives up prices, companies increase investment, ultimately leading to oversupply and price collapses. History also shows that the higher the peak, the deeper the subsequent trough often is. During the IT bubble, the peak annual growth rate exceeded 50%, only to plummet by 49.5% the following year; during the 2017-2018 memory bubble, the peak exceeded 60%, followed by a 33% decline in 2019.