en.Wedoany.com Reported - Water-related spending in the European data center industry is projected to reach €6.8 billion by 2036. According to the report "Europe Water for Data Centers: Market Trends, Opportunities, and Forecasts, 2026–2036" published by Bluefield Research, the rapid development of artificial intelligence (AI) is a primary driver of this growth, placing additional pressure on power grids, water resources, and permitting systems.

Zineb Moumen, an analyst at Bluefield Research, stated that the rapid advancement of AI and hyperscale computing is reshaping the relationship between Europe's digital infrastructure and water systems. Water resources are becoming a critical design, operational, and permitting factor influencing data center siting and operations. The industry's growth is facing increasingly stringent regulatory and physical constraints. New EU reporting requirements for electricity and water usage, coupled with stricter local permitting regimes, intensifying regional water stress, and strained energy systems, are making water availability, alongside power access, a key determinant of project feasibility, siting, and development timelines.

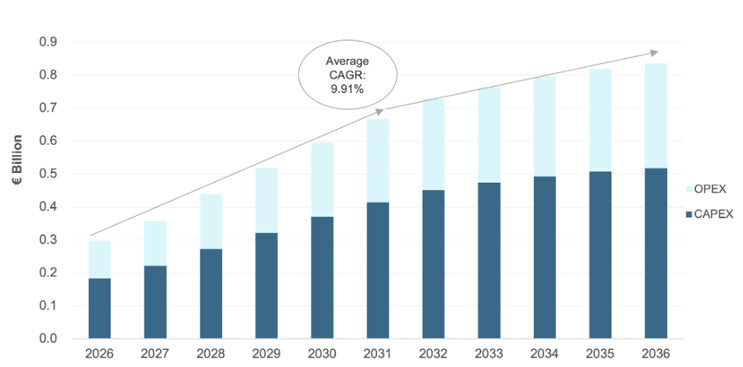

Under Bluefield Research's base case scenario, cumulative water-related spending is expected to reach €6.8 billion by 2036. In a high-growth scenario driven by accelerated AI adoption and more favorable permitting conditions, this spending could climb to €7.1 billion. Even under a low-growth outlook, the market is projected to reach €4.7 billion. Moumen believes that as the European data center market becomes more capital-intensive and resource-constrained, the investment case for water infrastructure is becoming undeniable. Enduring opportunities will come from solutions that not only facilitate project development but also help secure permits, enable efficient operations, and scale over time.

From a regional growth perspective, Germany, the United Kingdom, and France are expected to account for 40.5% of cumulative water-related spending in data centers by 2036. Future growth in these markets will be increasingly influenced by factors such as grid access, permitting requirements, energy efficiency targets, and heat reuse obligations. The next wave of expansion is emerging in Spain, Italy, Poland, and the Nordic countries, each facing distinct constraints and opportunities. Spain focuses on water-resilient development in water-stressed regions, Italy emphasizes land-use planning and regional permitting constraints, Poland prioritizes grid modernization and heat recovery integration, while the Nordic countries rely on low-carbon electricity and sustainable cooling strategies.

Regarding indirect water use, cooling system water consumption often receives the most attention, but a growing share of the data center water footprint is indirectly derived from electricity generation. Bluefield Research estimates that by 2036, indirect water consumption related to electricity consumption in European data centers will increase by 30%. This exposure varies by country; for example, markets more reliant on thermal power (such as Germany) exhibit higher indirect water intensity compared to markets with low-carbon electricity mixes (such as Austria, Sweden, and Denmark). Due to the highly interconnected nature of power systems, the situation in Europe is more complex, as data centers may rely on electricity from diverse sources, including nuclear, hydropower, natural gas, renewables, and imported power. Recent heatwaves have highlighted the vulnerability of these systems, with elevated river water temperatures limiting nuclear power output in several markets. Moumen explained that the indirect water footprint associated with electricity is an exposure most operators have not yet incorporated into their planning. As AI workloads expand and server density increases, operators need to understand not only how many megawatts are available but also how much water exposure is embedded within those megawatts.

In terms of cooling technology, as AI workloads increase computing density and heat loads, liquid cooling is transitioning from a niche technology to a core component of next-generation data center design. Bluefield Research predicts that by 2036, liquid cooling technology will account for approximately 20% of the European data center cooling market. This shift is redefining competitive dynamics in the cooling, water treatment, and infrastructure markets. Infrastructure suppliers such as Ecolab and Vertiv are expanding their capabilities through acquisitions, building integrated platforms encompassing cooling, water treatment, and system optimization. Meanwhile, water treatment suppliers are becoming attractive acquisition targets, as data center operators seek partners capable of supporting performance, water quality management, and regulatory compliance. Moumen stated that the European data center market is entering a phase where cooling can no longer be provided as a standalone system. As AI deployments scale up, operators must manage the entire thermal ecosystem, from liquid cooling and water quality to utility integration and operational performance. The companies most likely to achieve growth will be those that can offer these capabilities as integrated solutions.