Executive Summary

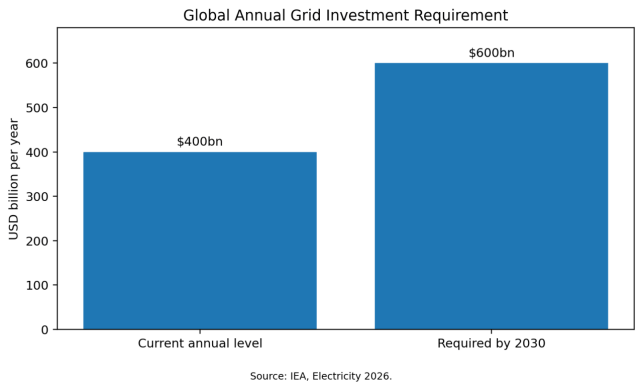

Global substations are entering a sustained investment cycle as electricity demand, renewable generation, data centers, industrial electrification and transmission expansion grow simultaneously. The International Energy Agency estimates that annual grid investment must rise by about 50% from today's approximately USD 400 billion to around USD 600 billion by 2030. Substations are a central beneficiary because every new transmission corridor, distribution upgrade and major load connection requires transformation, switching, protection and control.

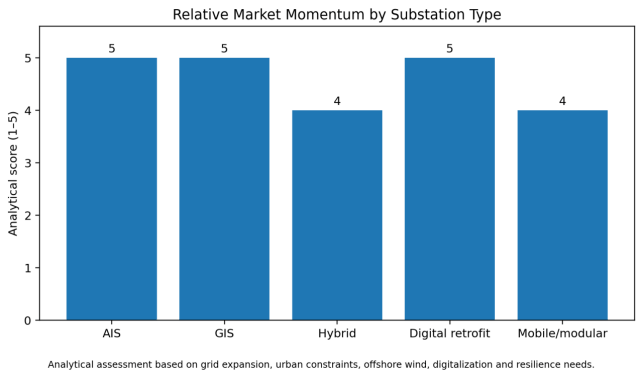

The market is shifting from conventional equipment packages toward integrated substations combining power transformers, air-insulated or gas-insulated switchgear, digital protection, IEC 61850 communication, condition monitoring and cybersecurity. Urban land constraints favor compact GIS, while cost-sensitive greenfield projects often continue to use AIS. Hybrid solutions are gaining ground where utilities need compactness without the full cost of GIS.

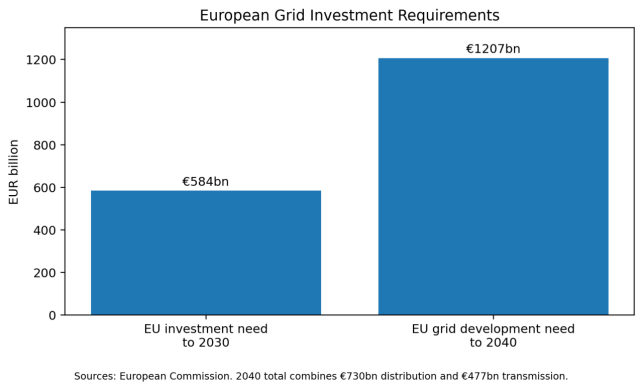

Europe is the most regulation-driven region. The European Commission estimates that EUR 584 billion in grid investment is required by 2030. Its 2040 guidance identifies approximately EUR 730 billion for distribution and EUR 477 billion for transmission development. At the same time, F-gas regulation and utility decarbonization are accelerating the adoption of SF6-free high-voltage equipment.

For buyers, substation procurement can no longer be reduced to a transformer-plus-switchgear quotation. Land, civil works, protection integration, communications, testing, outage planning, local certification and lifecycle service can determine the final project economics. Delivery risk is increasingly concentrated in large transformers, high-voltage GIS, protection engineering and skilled commissioning resources.

Key Findings

- Global grid investment must increase to roughly USD 600 billion annually by 2030, supporting a multi-year substation demand cycle.

- European grid investment requirements exceed EUR 584 billion to 2030 and approximately EUR 1.2 trillion to 2040.

- Digital substations are moving from pilot status toward mainstream utility deployment, particularly through IEC 61850 process-bus architectures.

- GIS is favored in urban, offshore and space-constrained applications, while AIS remains cost-effective for many greenfield projects.

- SF6-free high-voltage equipment is becoming a strategic procurement requirement in Europe and a growing differentiator globally.

- Transformer and GIS lead times can dominate project schedules; early capacity reservation is increasingly important.

- International procurement is shifting from lowest equipment price toward integrated delivery, interoperability, cybersecurity and lifecycle service.

Figure 1. Global annual grid investment requirement.

1. Market Definition and Scope

A substation is an integrated electrical facility that transforms voltage, switches circuits, protects equipment and controls power flow. Depending on voltage and application, it may include power transformers, circuit breakers, disconnectors, busbars, current and voltage transformers, surge arresters, reactive-power equipment, station-service systems, protection relays, batteries, SCADA and communication systems.

The market includes transmission substations, distribution substations, renewable-energy collector substations, industrial substations, urban GIS substations, offshore substations, mobile substations and digital retrofit projects. Contract scope varies from individual equipment supply to complete engineering, procurement and construction packages.

Commercial market-size estimates vary substantially because some count only primary equipment while others include civil construction, automation, engineering and services. This report therefore uses grid investment, project pipelines, equipment capacity and authoritative public data rather than relying on a single commercial market-value estimate.

|

Substation Type |

Typical Application |

Main Strength |

Key Constraint |

|

AIS |

Transmission and distribution greenfield sites |

Lower equipment cost and easy visual inspection |

Large land footprint |

|

GIS |

Urban, offshore, industrial and high-pollution sites |

Compact footprint and sealed equipment |

Higher cost and specialized service |

|

Hybrid |

Retrofits and constrained sites |

Balances footprint and cost |

Interface complexity |

|

Digital substation |

New and retrofit projects |

Less copper wiring, better data and diagnostics |

Cybersecurity and engineering capability |

|

Mobile/modular |

Emergency, mining and temporary connections |

Fast deployment and flexibility |

Transport and rating limits |

2. Global Demand Drivers

Electricity demand is rising faster than in the previous decade. Data centers, electric vehicles, heat pumps, industrial electrification and new manufacturing loads are creating both transmission and distribution bottlenecks. Substations are required not only for new capacity, but also to improve resilience and sectionalize existing networks.

Renewable deployment is another major driver. The IEA expects around 4,600 GW of renewable electricity additions during 2025–2030. Solar, wind and storage projects require collector substations, step-up transformers, reactive-power control, protection coordination and grid-code compliance.

Replacement demand is equally important. Many utilities operate substations installed decades ago. Modernization programs replace circuit breakers, protection relays, instrument transformers and control systems while retaining selected civil structures and transformers. This creates a substantial retrofit market separate from greenfield construction.

Figure 2. Relative market momentum by substation type.

3. Regional Market Analysis

3.1 North America

Demand is driven by data centers, manufacturing reshoring, renewable interconnection, wildfire resilience and replacement of aging utility assets. Buyers emphasize ANSI/IEEE compliance, seismic qualification, cybersecurity and local service. Long transformer and breaker lead times are encouraging framework agreements and early equipment reservation.

3.2 Europe

Europe combines high grid investment with the fastest shift toward digital and SF6-free substations. Urban density and offshore wind favor GIS. Utilities increasingly use IEC 61850 process-bus systems and low-power instrument transformers. The EU's F-gas policy is accelerating qualification of clean-air and vacuum-based high-voltage platforms.

3.3 China and Asia-Pacific

China has one of the world's largest substation engineering and manufacturing ecosystems, including UHV, GIS, transformers, protection and automation. India and Southeast Asia are expanding transmission and distribution infrastructure rapidly. Japan, South Korea and Australia remain high-specification markets with strict utility qualification.

3.4 Middle East and Africa

The Middle East is supported by new generation, desalination, data centers, rail, oil and gas and large solar projects. High temperature, dust and corrosion affect equipment design. Africa offers major electrification and mining opportunities, but financing, currency and service logistics remain important risks.

3.5 Latin America

Renewable expansion, mining and transmission concessions support demand in Brazil, Chile, Peru, Colombia and Mexico. Retrofit opportunities are growing as utilities modernize protection and control. High altitude, seismic requirements and long-distance logistics are common design considerations.

Figure 3. European grid investment requirements.

4. Technology Routes: AIS, GIS, Hybrid and Digital

AIS remains the reference choice for many greenfield projects because it is comparatively simple, inspectable and economical where land is available. Its disadvantages are footprint, exposure to pollution and weather, and larger civil works.

GIS uses sealed metal enclosures and gas or alternative insulation to achieve compact layouts. It is favored in cities, offshore platforms, tunnels, industrial plants and high-pollution environments. The trade-off is higher equipment cost, more specialized installation and a greater dependence on manufacturer service.

Digital substations use IEC 61850-based communication, process-bus architectures and intelligent electronic devices. They can reduce copper wiring, improve diagnostics and support remote operation. Türkiye's first digital substation pilot announced in 2026 used a parallel feeder protection and control bay with process-bus technology to compare digital and conventional performance.

SF6-free high-voltage technology is moving into commercial deployment. Siemens Energy's Burladingen project uses 145 kV clean-air GIS, while its 420 kV LIFE Blue project aims to demonstrate F-gas-free GIS at transmission voltage. Beijing's Daying 110 kV substation uses F-gas-free GIS and ester-filled transformers.

5. Cost Structure and Project Economics

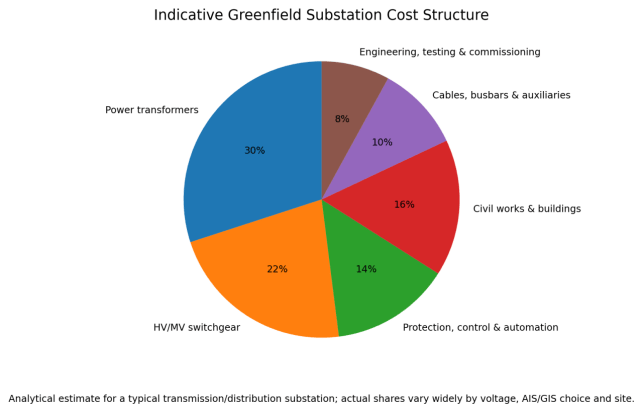

Substation cost depends on voltage, MVA capacity, short-circuit level, land, AIS/GIS selection, redundancy, civil conditions and automation scope. Large power transformers are often the single largest equipment item, followed by HV/MV switchgear and civil works.

GIS can reduce land and building cost enough to offset part of its equipment premium in dense urban environments. AIS may remain cheaper in rural locations. Digital designs can reduce control cabling and commissioning effort, but require more engineering, cybersecurity and lifecycle software support.

Project economics should include outage cost, schedule delay, energy losses, maintenance and future expansion. A lower equipment quotation can become more expensive if it requires larger buildings, longer outages or weak local service.

Figure 4. Indicative greenfield substation cost structure.

6. Supply Chain and Delivery Risk

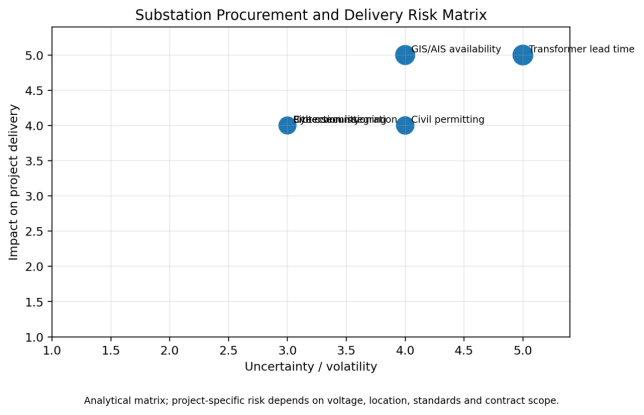

Large transformers remain the most critical long-lead item. High-voltage GIS, bushings, tap changers, protection relays, instrument transformers and test capacity can also constrain schedules. Equipment manufacturing expansion takes time because factories require specialized machinery, clean assembly, test laboratories and qualified labor.

Substation delivery risk extends beyond equipment. Permitting, land acquisition, civil works, cable interfaces, protection studies, telecom integration and outage windows can delay energization. Turnkey contracts reduce interface count but place more risk on the EPC supplier.

Mobile and modular substations are gaining interest for emergency restoration, mining, temporary grid connections and phased capacity. Hitachi Energy's 2026 mobile digital substation project in Chile illustrates the value of flexible high-voltage solutions for critical mining environments.

Figure 5. Substation procurement and delivery risk matrix.

7. Digitalization, Automation and Cybersecurity

Digital substations replace some conventional copper-based measurement and control circuits with sensors, merging units and communication networks. Benefits include faster commissioning, reduced wiring, remote diagnostics and improved asset visibility.

IEC 61850 is the core interoperability framework, but implementation quality varies. Buyers should specify system architecture, data models, time synchronization, redundancy, testing and multivendor interoperability.

Cybersecurity is now a lifecycle requirement. Procurement documents should define network segmentation, secure remote access, firmware governance, patch responsibility, event logging, account management and data ownership. A technically advanced system without long-term software support can create higher risk than a conventional design.

8. International Standards and Procurement Requirements

|

Area |

Typical Standards / Requirements |

Main Buyer Risk |

|

Primary equipment |

IEC 62271, IEC 60076 or ANSI/IEEE equivalents |

Mixing incompatible rating and test philosophies |

|

Substation automation |

IEC 61850 |

Interoperability and configuration-management gaps |

|

Cybersecurity |

IEC 62351, national utility requirements |

Unclear patching and remote-access responsibility |

|

Civil and seismic design |

Local building and seismic codes |

Underestimating site-specific engineering |

|

Environmental compliance |

EU F-gas rules and local permitting |

Selecting equipment incompatible with future operation |

|

Testing and commissioning |

FAT, SAT, primary/secondary injection, end-to-end tests |

Incomplete ownership of interface testing |

9. Competitive Landscape

The global market includes Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, ABB, Mitsubishi Electric, Toshiba and major Chinese and regional EPC suppliers. Competitive position differs by voltage and contract scope. High-voltage turnkey projects require stronger engineering, testing and installed-base support than standard distribution substations.

Competition is moving toward integrated solutions, digitalization, low-carbon equipment and lifecycle service. Suppliers with transformer, switchgear, protection and automation portfolios can reduce interface risk, while specialist EPC contractors compete through local execution and project management.

Chinese suppliers are competitive in equipment cost, manufacturing scale and turnkey capability. Their main international challenges are utility qualification, destination-market certification, documentation, financing, local service and bankability.

10. Real Project Cases

|

Project |

Date |

Market Significance |

|

Türkiye first digital substation pilot |

2026 |

IEC 61850 process-bus deployment comparing digital and conventional systems. |

|

Chile mobile digital substation |

2026 |

Flexible high-voltage solution for mining and critical-load continuity. |

|

Beijing Daying 110 kV zero-carbon substation |

2025 |

F-gas-free GIS, ester transformers and digital integration. |

|

Brazil AXIA Energia retrofit |

Current program |

More than 1,000 components across 40 substations replaced in a major modernization program. |

|

Burladingen 145 kV substation, Germany |

Operational reference |

Clean-air GIS and digital measurement demonstrate SF6-free transmission technology. |

11. Procurement Recommendations

- Freeze voltage, MVA, short-circuit, redundancy and protection philosophy early.

- Select AIS, GIS or hybrid design using total project cost, not equipment price alone.

- Reserve transformer and GIS manufacturing capacity before final civil completion.

- Define all interfaces among transformer, switchgear, protection, telecom and civil packages.

- Require valid type tests and destination-market certification.

- Specify IEC 61850 architecture, cybersecurity and software support in contractual terms.

- Use staged design review, factory inspection, FAT, site acceptance and end-to-end testing.

- Price critical spares, emergency support and long-term service at contract award.

- Evaluate outage, delay and energization risk as part of TCO.

- Verify local construction capability, permits, logistics and commissioning resources.

12. Market Outlook, 2026–2030

The global substation outlook remains strong because investment is being pulled by both new demand and replacement of aging infrastructure. Transmission and distribution projects, offshore wind, large solar, storage and data centers will sustain equipment demand.

Digital substations will expand from protection-and-control upgrades into full process-bus architectures. Adoption will be fastest where utilities have strong engineering capability and standardized IEC 61850 practices.

GIS and hybrid substations will gain share in space-constrained and offshore applications, while AIS will remain important in cost-sensitive greenfield markets. SF6-free technology will move from European regulatory compliance toward a broader global specification preference.

Prices are unlikely to return quickly to pre-2021 conditions for critical high-voltage equipment. Capacity expansion may moderate lead times, but transformer, GIS and skilled-engineering bottlenecks will remain strategically important.

Conclusion

The global substation market is moving beyond conventional equipment replacement into a broader transformation of electrical infrastructure. Growth is being driven by grid investment, renewable integration, data centers, industrial electrification and resilience.

The most valuable projects will combine reliable primary equipment, digital protection, cybersecurity, low-carbon technology and disciplined lifecycle service. Buyers should evaluate complete delivered value and interface risk rather than lowest equipment price.

Through 2030, suppliers with qualified manufacturing capacity, integrated engineering, digital capability and local execution will be best positioned.