Executive Summary

Energy storage power conversion systems (PCS) are becoming one of the most strategically important components in modern power systems. A PCS converts battery DC output into grid-compatible AC power and performs the reverse conversion during charging. Its commercial role now extends well beyond energy conversion: advanced systems provide reactive power, frequency response, voltage control, black start, islanding support, fault ride-through and, increasingly, grid-forming capability.

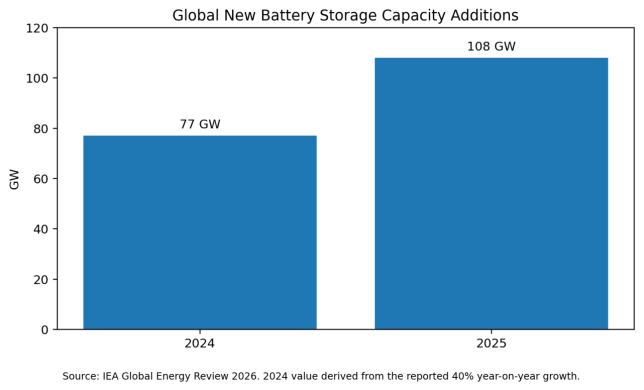

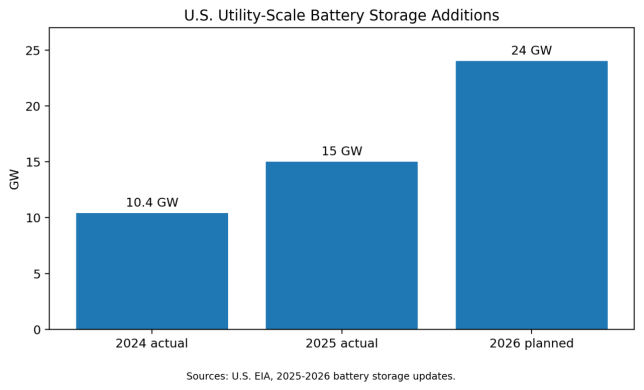

The market is expanding rapidly because battery storage deployment is accelerating. The International Energy Agency reported that 108 GW of new battery storage capacity was deployed globally in 2025, 40% more than in 2024. Installed capacity was eleven times higher than in 2021. In the United States, the Energy Information Administration reported a record 15 GW of utility-scale battery additions in 2025 and 24 GW planned for 2026.

PCS demand therefore depends not only on the number of battery containers sold, but also on project power ratings, duration, DC/AC ratio, grid-code requirements, system architecture and revenue model. A four-hour battery may use the same PCS power rating as a two-hour system with twice the energy, which means PCS demand should be analyzed in GW rather than GWh alone.

The most important technology shift is from grid-following to grid-forming control. Grid-following PCS synchronizes to an existing voltage waveform, while grid-forming PCS can establish voltage and frequency references and support weak or islanded networks. This capability is increasingly valuable in systems with high shares of inverter-based resources, but it requires validated controls, accurate models, sufficient DC energy, thermal headroom and clear performance specifications.

Key Findings

- Global battery storage additions reached 108 GW in 2025, creating a strong structural demand base for PCS.

- PCS competition is shifting from conversion efficiency and price toward grid-code compliance, validated dynamic models and grid-forming capability.

- Central PCS remains attractive for large utility projects, while string PCS is gaining share where modularity and fault isolation are valued.

- Power semiconductors, magnetics, thermal systems, controls and certification are the main PCS cost drivers.

- Low equipment price can be offset by derating, weak fault ride-through, model mismatch, harmonic issues or limited local service.

- Regional standards differ materially: IEEE 1547 and IEEE 2800 matter in North America, ENTSO-E and national grid codes shape Europe, and IEC 62933 provides a global storage-system framework.

- International buyers should evaluate delivered lifecycle value, not only USD/kW.

Figure 1. Global new battery storage capacity additions.

1. Product Definition and Market Scope

A PCS is a bidirectional converter that connects batteries or other DC storage media to an AC grid or load. Typical equipment includes power semiconductor modules, DC link, inductors or transformers, filters, protection, control processors, communication interfaces, cooling systems and enclosures.

The product can be sold as a standalone inverter cabinet, an outdoor skid, a containerized unit or an integrated medium-voltage block combining PCS, transformer and switchgear. Project boundaries vary significantly. Some quotations include only the converter; others include MV transformer, auxiliary power, HVAC, EMS interface, protection studies, commissioning and grid-code validation.

PCS market analysis must therefore distinguish power from energy. Battery cells and racks are usually measured in MWh or GWh, while PCS is primarily sized in MW or GW. A falling DC battery price does not automatically imply the same percentage decline in PCS pricing.

|

PCS Type |

Typical Application |

Main Advantages |

Primary Trade-Off |

|

Central PCS |

Large utility-scale BESS |

High power density, fewer units, simpler MV aggregation |

Larger fault domain and lower modularity |

|

String PCS |

Distributed blocks and modular utility projects |

Better fault isolation, flexible augmentation, granular control |

More units, communication complexity and balance-of-system interfaces |

|

Grid-forming PCS |

Weak grids, islands, high-IBR systems, black-start projects |

Voltage/frequency support and system-strength services |

More demanding controls, validation and energy-management requirements |

|

MV-integrated PCS |

Large utility-scale projects |

Lower cabling, compact block design and faster installation |

Greater supplier dependence and more complex replacement |

2. Global Demand Outlook

Battery storage is now the fastest-growing power technology. The IEA's 2026 review shows that deployment is moving from early ancillary-service markets into mainstream capacity, arbitrage, renewable integration and network support. LFP chemistry accounts for around 90% of recent deployments, improving cost predictability for system integrators.

PCS demand grows with storage power capacity and with the increasing complexity of grid services. Systems that provide only energy shifting may require standard bidirectional conversion, while projects providing fast frequency response, synthetic inertia, voltage support or black start require more advanced controls and testing.

The commercial value of PCS is therefore rising even as average hardware prices face pressure. Buyers increasingly pay for performance guarantees, plant-level controls, validated simulation models, compliance testing and local service.

Figure 2. U.S. utility-scale battery storage additions.

3. Regional Market Analysis

3.1 China

China is the world's largest manufacturing base for PCS and battery systems. Domestic competition has driven rapid cost reduction, high power density and integrated DC-block plus PCS solutions. The market is moving from basic peak-shaving projects toward stronger requirements for grid support, safety and lifecycle operation. Export success depends on destination-market certification, grid-code models, cybersecurity and local service.

3.2 United States

The U.S. market is supported by rapid deployment in Texas, California and Arizona. EIA data show more than 40 GW of utility-scale battery capacity added over the five years to 2025, with another 24 GW planned for 2026. IEEE 2800, interconnection studies, NERC requirements and plant-controller validation are increasingly important. Domestic-content rules and service response also affect procurement.

3.3 Europe

Europe's market is driven by renewable balancing, capacity markets, congestion management and price volatility. Projects face national grid codes in addition to EU-level requirements. Grid-forming capability is becoming a major research and procurement theme, particularly in island systems and areas with declining synchronous generation.

3.4 Australia and Other Asia-Pacific Markets

Australia is an early market for large batteries and advanced grid-support services. Weak-grid conditions, system-strength requirements and high renewable penetration favor sophisticated PCS controls. Japan, South Korea and Southeast Asia offer opportunities in grid support, industrial backup and renewable integration, but local standards and utility qualification vary.

3.5 Middle East, Latin America and Africa

These markets are expanding through solar-plus-storage, isolated grids, mining, industrial power and resilience projects. High ambient temperature, dust, weak grids, limited service networks and project-finance risk make thermal design, derating and remote support especially important.

4. Technology Routes and Control Architecture

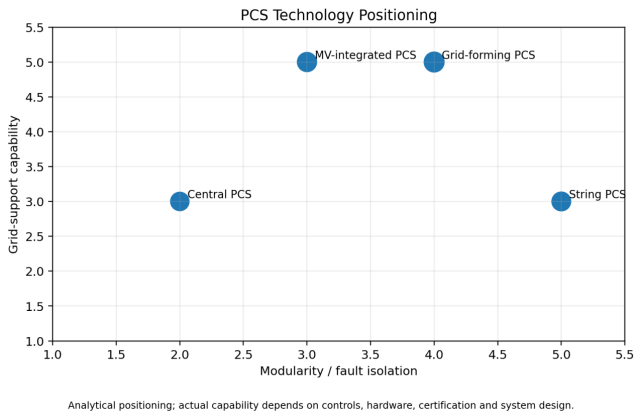

Central PCS architectures concentrate large power blocks, often from 1 MW to several megawatts per unit. They can reduce equipment count and simplify MV collection, making them attractive for large sites with standardized layouts.

String PCS divides the project into smaller power blocks. This improves modularity, fault isolation and augmentation flexibility. It can also allow different battery racks to operate closer to their optimal state, but the design requires more communication nodes and careful plant-level coordination.

Grid-following PCS uses a phase-locked loop to follow an existing grid waveform. Grid-forming PCS behaves more like a controlled voltage source and can support voltage and frequency in weak systems. DOE and IEA publications increasingly identify grid-forming inverters as a critical technology for systems with high shares of inverter-based resources.

Advanced PCS also provides black start, islanding, seamless transfer, reactive power at low active power, harmonic compensation and fast fault response. These functions should be specified through measurable performance tests rather than marketing labels.

Figure 3. PCS technology positioning.

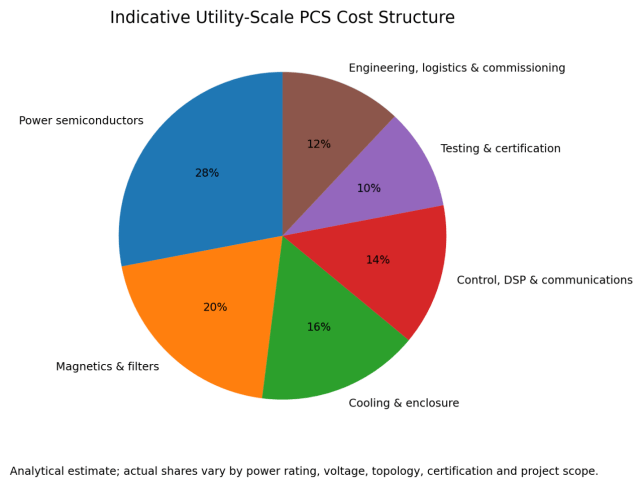

5. Price and Cost Structure

PCS prices are commonly compared in USD/kW, but the denominator can conceal important scope differences. A quoted price may exclude MV transformer, switchgear, EMS integration, commissioning, grid-model development, spare parts and extended warranty.

Power semiconductor devices are a major cost element. Silicon IGBT remains widely used, while silicon-carbide devices can improve efficiency, switching frequency and compactness in selected applications. Magnetics, filters and transformers determine harmonic performance and contribute significant material cost.

Cooling architecture is another economic variable. Air-cooled systems can reduce auxiliary complexity but may derate more sharply at high temperature. Liquid-cooled PCS can offer higher power density and stable thermal performance, but adds pumps, heat exchangers, leak management and maintenance requirements.

Price pressure is likely to continue in standardized hardware, especially from Chinese suppliers. However, engineering, certification, controls, service and grid-code compliance will represent a larger share of project value.

Figure 4. Indicative utility-scale PCS cost structure.

6. Supply Chain and Manufacturing

Critical inputs include IGBT or SiC modules, gate drivers, DC capacitors, reactors, transformers, control processors, current sensors, cooling components and industrial communication hardware. Semiconductor availability and qualification can influence delivery schedules.

PCS manufacturing requires power-stage assembly, insulation design, thermal management, firmware, hardware-in-the-loop testing, protection verification and high-power factory testing. The limiting resource may be engineering and validation capacity rather than physical assembly alone.

International projects add certification, packaging, freight, field commissioning and service risks. A low-cost factory offer can lose its advantage if local grid tests fail or firmware updates require long overseas response times.

7. Grid Codes, Standards and Compliance

|

Area |

Typical Reference |

Procurement Significance |

|

Energy storage system framework |

IEC 62933 series |

Defines terminology, performance, planning, environmental and safety requirements |

|

North American DER interconnection |

IEEE 1547 |

Relevant for distribution-connected storage and DER behavior |

|

North American transmission IBR |

IEEE 2800 |

Influences ride-through, reactive power, modeling and performance requirements |

|

European grid connection |

ENTSO-E requirements plus national grid codes |

Creates country-specific testing and model obligations |

|

Power conversion safety |

UL 1741 and applicable IEC standards |

Controls certification, protection and market access |

|

Communication and controls |

IEC 61850, Modbus, DNP3 and utility protocols |

Affects plant integration, interoperability and cybersecurity |

Buyers should require validated RMS and EMT models where applicable. Model mismatch between the interconnection study and delivered firmware can delay commissioning or reduce usable project capacity.

8. Total Cost of Ownership and Project Economics

TCO = Purchase + Balance of System + Losses + Auxiliary Energy + Maintenance + Compliance + Downtime Risk - Residual Value

Round-trip efficiency is often quoted at system level, but PCS conversion efficiency remains important because losses occur during both charge and discharge. Efficiency curves should be evaluated across expected loading, not only at rated power.

Thermal derating can reduce revenue in hot climates. A PCS that delivers full nameplate only at moderate ambient temperature may require oversizing or reduced dispatch. Buyers should request power-versus-temperature curves and auxiliary-consumption data.

Availability and service response are central to economics. A failed central PCS can remove a large project block, while string architecture may limit the outage. The correct architecture depends on spare strategy, service capability and revenue stacking.

Grid-forming capability may create additional system value, but only if market rules or network operators compensate the service. Buyers should avoid paying for unverified features that are not contractually testable.

9. Competitive Landscape

The global market includes specialized PCS manufacturers, solar-inverter companies, power-electronics groups and vertically integrated battery-system suppliers. Competitive position differs by region because grid codes, certification and utility references create barriers.

Chinese suppliers are strong in cost, manufacturing scale and integrated solutions. European, North American, Japanese and Korean suppliers often compete through grid integration, local service, utility qualification and advanced controls.

Competition is moving toward full-solution capability: PCS hardware, plant controller, EMS interface, dynamic models, grid-code testing, cybersecurity and long-term service. Suppliers that cannot support the complete commissioning process may struggle even with competitive hardware.

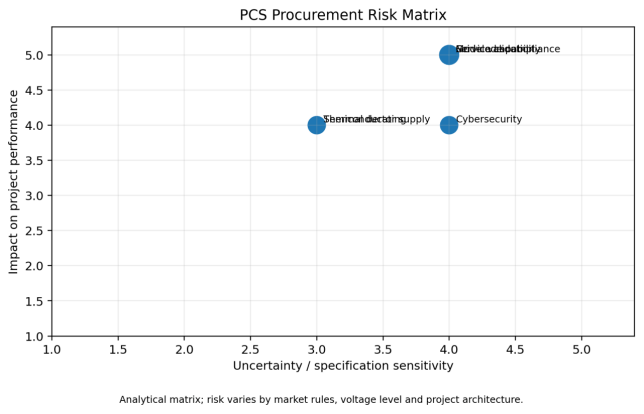

10. International Procurement Recommendations

- Compare PCS quotations on a common delivered scope, including MV transformer, switchgear, controls, testing and commissioning.

- Define grid-following and grid-forming requirements through measurable performance specifications.

- Require power-versus-temperature curves, efficiency curves and auxiliary-consumption data.

- Verify fault ride-through, reactive-power capability, black-start and islanding behavior where required.

- Request validated RMS and EMT models that match the delivered firmware version.

- Audit semiconductor, capacitor, reactor and cooling-system supply chains.

- Specify cybersecurity, remote access, firmware governance and data ownership.

- Evaluate central versus string architecture using availability, spares and augmentation strategy.

- Include local service response, strategic spares and long-term software support in the commercial evaluation.

- Use staged FAT, hardware-in-the-loop testing, site acceptance and grid-compliance verification.

Figure 5. PCS procurement risk matrix.

11. Market Outlook, 2026-2030

The PCS market is likely to grow rapidly through 2030 as battery deployment expands across utility, commercial, industrial and microgrid applications. Growth in MW will be especially important because PCS revenue follows power capacity more closely than stored energy.

Average standardized hardware prices will remain under pressure, but advanced controls, grid-forming functions, plant integration and service will support higher-value segments.

String architectures are likely to gain share in modular projects, while central and MV-integrated blocks will remain strong in large utility systems. Grid-forming capability will transition from selected projects toward broader grid-code adoption.

The main market risks are aggressive price competition, inconsistent grid-forming definitions, model-performance gaps, semiconductor supply concentration and inadequate local service.

Conclusion

The global energy storage PCS market is moving from a hardware-led growth phase into a grid-performance-led phase. Rapid battery deployment provides the volume base, but future competitive advantage will depend on controls, modeling, reliability and integration.

For buyers, the lowest USD/kW quotation is not necessarily the lowest-cost solution. Efficiency, thermal performance, availability, grid compliance and service response can materially affect project revenue and commissioning risk.

Through 2030, the strongest suppliers will be those that combine scalable power electronics with validated grid-forming capability, destination-market certification and long-term technical support.