Executive Summary

Industrial Ethernet switches are becoming core infrastructure for factories, substations, railways, mines, ports, oil and gas facilities, water systems and intelligent transport. Unlike office switches, industrial products are designed for wide temperature ranges, electromagnetic interference, vibration, redundant power, deterministic traffic and long service lives.

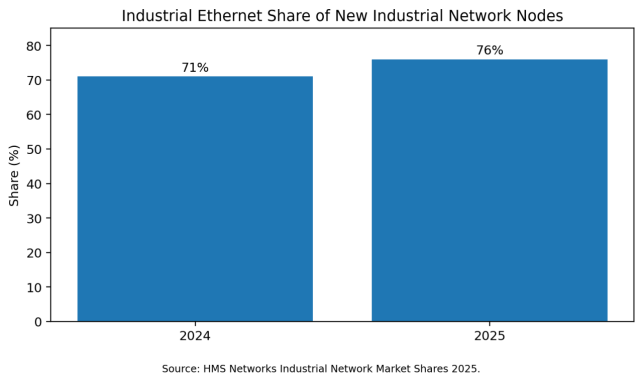

The market is supported by the continuing migration from fieldbus to Ethernet. HMS Networks reported that Ethernet-based technologies represented 76% of new industrial network nodes in its 2025 analysis, up from 71% in 2024. This shift expands demand for managed Layer 2 and Layer 3 switches, fiber aggregation, Power over Ethernet, edge security and network-management software.

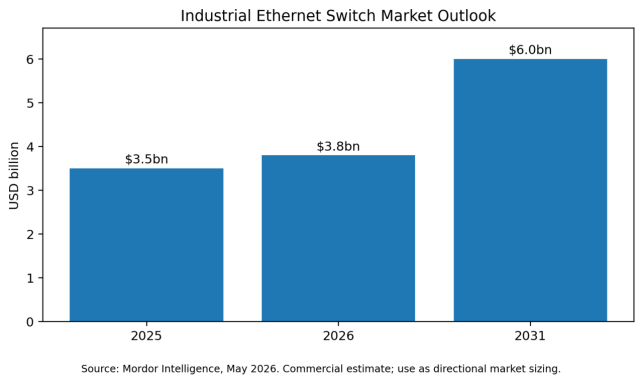

Commercial estimates place the industrial Ethernet switch market at roughly USD 3.5 billion in 2025 and about USD 3.8 billion in 2026, with growth toward USD 6.0 billion by 2031. Such estimates vary by whether software, services, routers and embedded switching are included, so this report treats them as directional rather than a single definitive market value.

The next technology cycle will be shaped by Time-Sensitive Networking, IT/OT convergence and cybersecurity. IEEE TSN standards allow time-critical traffic to share Ethernet infrastructure with other applications while maintaining bounded latency. The IEC/IEEE 60802 industrial automation profile is moving toward standardizing how TSN tools are applied in factories. At the same time, IEC 62443 is increasingly used to define security programs, system requirements and secure product-development practices.

Key Findings

- Industrial Ethernet represented 76% of new industrial network nodes in the 2025 HMS analysis, confirming Ethernet as the dominant factory-network technology.

- Demand is shifting from unmanaged connectivity toward managed, secure and remotely diagnosable switches.

- TSN is a long-term convergence technology rather than an immediate replacement for PROFINET, EtherNet/IP, EtherCAT and other established ecosystems.

- Industrial cybersecurity is becoming a product-selection criterion, with IEC 62443 increasingly referenced by asset owners and suppliers.

- Utility, rail and process applications require stronger redundancy, EMC immunity, time synchronization and environmental qualification than general factory automation.

- Hardware price is only one part of lifecycle cost; configuration, diagnostics, downtime, firmware support and spare compatibility can dominate TCO.

- Chinese manufacturers are competitive in hardware cost and port density, but international projects require protocol interoperability, certification, cybersecurity documentation and local support.

Figure 1. Industrial Ethernet share of new industrial network nodes.

1. Product Definition and Segmentation

An industrial Ethernet switch forwards Ethernet frames between controllers, drives, robots, cameras, remote I/O, sensors, HMIs, servers and gateways. The industrial design adds hardened power inputs, DIN-rail or rack mounting, wide operating temperature, shock and vibration resistance, electromagnetic compatibility and long product availability.

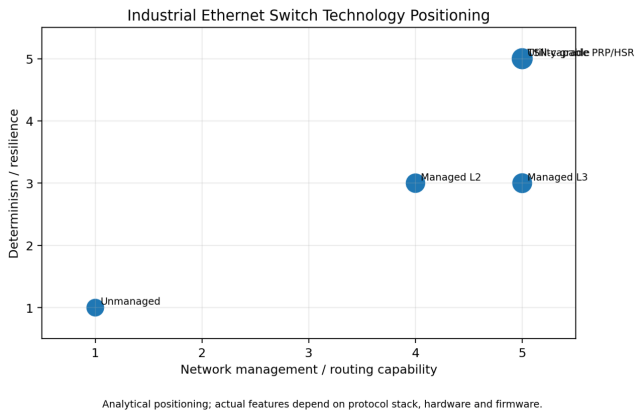

The market includes unmanaged switches, managed Layer 2 switches, Layer 3 routing switches, Power over Ethernet switches, fiber aggregation switches, TSN-capable products and utility-grade switches supporting PRP or HSR seamless redundancy.

Product boundaries vary. Some market studies include routers, wireless access points, network-management software and services; others count only standalone switches. Price comparisons also vary depending on port count, copper/fiber mix, PoE budget, certification and software license.

|

Product Type |

Typical Applications |

Main Value |

Main Limitation |

|

Unmanaged industrial switch |

Small machines, simple cells, basic edge connectivity |

Low cost and easy deployment |

Limited diagnostics, segmentation and security |

|

Managed Layer 2 |

Factories, water, transport and distributed control |

VLANs, redundancy, QoS, SNMP and diagnostics |

Requires network engineering and configuration |

|

Layer 3 / routing switch |

Large plants and converged OT networks |

Routing, segmentation, access control and scalability |

Higher cost and configuration complexity |

|

TSN-capable switch |

Motion, robotics and converged deterministic networks |

Time synchronization and bounded latency |

Interoperability and profile maturity remain important |

|

Utility-grade PRP/HSR switch |

Substations and critical infrastructure |

Zero-time recovery and high EMC resilience |

Higher hardware cost and specialized design |

2. Market Demand and Growth Drivers

Factory automation is the largest demand foundation. Robots, vision systems, servo drives and edge computers generate more data and require faster diagnostics than traditional serial fieldbus systems. Ethernet also simplifies data exchange between operational technology and manufacturing IT.

Critical infrastructure is another important market. Power substations require IEEE 1588 time synchronization, PRP/HSR redundancy and strong EMC immunity. Rail and intelligent transport need vibration resistance, fiber distance and PoE for cameras and wireless access points. Oil, gas, water and mining facilities value extended temperature, hazardous-location options and remote diagnostics.

Industrial AI and machine vision raise bandwidth requirements. Gigabit and 10-Gigabit uplinks are moving deeper into plants as high-resolution cameras, edge analytics and digital twins create more east-west traffic.

PoE is expanding the role of switches in powering cameras, access points, sensors, phones and edge devices. The commercial advantage is lower cabling cost, but thermal design and total PoE budget become critical in sealed cabinets and hot environments.

Figure 2. Directional industrial Ethernet switch market outlook.

3. Regional Market Analysis

3.1 North America

Demand is driven by automotive, semiconductor, logistics, oil and gas, utilities, data centers and manufacturing reshoring. EtherNet/IP has strong ecosystem support, while critical-infrastructure projects emphasize NERC-related security practices, IEEE 1613, PRP/HSR and local service.

3.2 Europe

Europe has a mature automation base in automotive, machinery, process industries and rail. PROFINET and EtherCAT are widely deployed, and IEC 62443 security requirements are increasingly incorporated into procurement. TSN, OPC UA and Single Pair Ethernet are important development themes.

3.3 China and Asia-Pacific

Asia-Pacific combines the world's largest electronics and manufacturing base with expanding rail, utility and smart-city investment. China has a broad supplier ecosystem and strong cost competition. Japan, South Korea and Taiwan emphasize precision automation and semiconductor production, while Southeast Asia benefits from new industrial investment.

3.4 Middle East and Africa

Oil and gas, utilities, desalination, mining, ports and transport are the main demand sources. High temperature, dust, long fiber distances and limited maintenance access make rugged design and remote management more valuable.

3.5 Latin America

Mining, energy, transport, food processing and water infrastructure support demand. Projects often require fiber rings, extended temperature, surge protection and strong distributor support.

4. Technology Trends

Managed networking is becoming the default for critical applications. VLANs, rapid spanning tree, ring redundancy, QoS, SNMP, port mirroring and event logging allow operators to isolate faults and reduce troubleshooting time.

TSN extends Ethernet with precise time synchronization, traffic scheduling and reliability mechanisms. IEEE states that TSN can carry time-critical applications on a shared network while providing bounded latency. The IEC/IEEE 60802 profile is intended to define TSN use for industrial automation.

PRP and HSR remain important in substations and other zero-recovery applications. Siemens utility-grade switches support PRP/HSR, IEEE 1588 and harsh electromagnetic environments, illustrating the specialization required beyond conventional office networking.

Single Pair Ethernet may extend Ethernet closer to sensors and actuators, while 5G and Wi-Fi remain complementary for mobile or difficult-to-cable assets. The likely architecture is hybrid rather than a complete replacement of wired industrial Ethernet.

Figure 3. Industrial switch technology positioning.

5. Cybersecurity and Standards

Industrial switches are now security enforcement points rather than passive connectivity devices. Secure boot, signed firmware, role-based access, SSH, HTTPS, SNMPv3, 802.1X, RADIUS, TACACS+, ACLs and event logging are increasingly expected.

IEC 62443 provides a framework for industrial automation and control-system security. IEC 62443-2-1:2024 defines asset-owner security-program requirements, IEC 62443-3-2 addresses risk assessment for system design, IEC 62443-3-3 defines system security requirements, and IEC 62443-4-1/4-2 cover secure product development and component requirements.

Buyers should distinguish between a supplier's development-process certification, product-level security capability and the security level of the deployed system. A compliant switch cannot compensate for weak architecture, shared credentials or unmanaged remote access.

|

Requirement |

Typical Reference |

Buyer Significance |

|

Industrial cybersecurity program |

IEC 62443-2-1 |

Defines asset-owner policies and lifecycle security management |

|

System risk assessment |

IEC 62443-3-2 |

Supports zoning, conduits and target security levels |

|

System security controls |

IEC 62443-3-3 |

Defines foundational system requirements |

|

Secure product development |

IEC 62443-4-1 |

Evaluates supplier development lifecycle |

|

Component security |

IEC 62443-4-2 |

Defines technical requirements for industrial components |

|

Time-sensitive networking |

IEEE 802.1 TSN and IEC/IEEE 60802 |

Supports deterministic converged industrial networks |

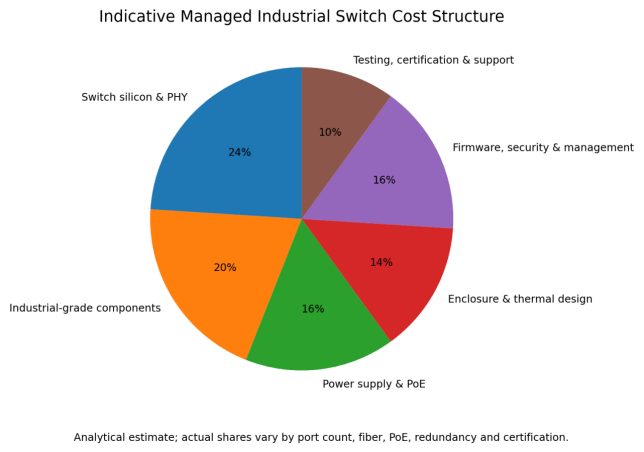

6. Cost Structure and Pricing

Industrial switch pricing can range from basic unmanaged DIN-rail products to high-port-density utility-grade platforms. Cost is driven by port count, Gigabit or 10-Gigabit capability, fiber transceivers, PoE power, operating temperature, redundant power, protocol support and certification.

Industrial-grade components and thermal design increase cost compared with commercial switches. Fanless construction, conformal coating, surge protection, isolated power inputs and extended-temperature semiconductors improve reliability in harsh environments.

Managed firmware and security features create significant lifecycle development cost. Buyers should evaluate whether software updates, vulnerability handling and configuration tools are included or require licenses.

Fiber modules and PoE budgets can materially change delivered price. Vendor-locked optics may raise lifecycle cost, while unsupported third-party optics can create reliability and warranty risk.

Figure 4. Indicative managed industrial switch cost structure.

7. Supply Chain and Product Lifecycle

Key inputs include Ethernet switch ASICs, PHYs, industrial processors, memory, power modules, magnetics, optical transceivers, connectors and rugged enclosures. Semiconductor shortages demonstrated that long industrial lifecycles can conflict with faster commercial-chip obsolescence.

Industrial users often expect ten or more years of product availability. Procurement should therefore examine last-time-buy policy, firmware support, replacement compatibility and configuration migration.

Manufacturing quality includes EMC testing, temperature cycling, vibration, shock, surge, ESD and burn-in. Utility and rail applications may require sector-specific approvals beyond general industrial standards.

8. Competitive Landscape

The market includes Cisco, Siemens, Belden/Hirschmann, Moxa, Phoenix Contact, Rockwell Automation, Schneider Electric, HPE Aruba, Advantech and numerous Chinese and regional suppliers. Competitive strength depends on the target vertical and protocol ecosystem.

Automation vendors benefit from integration with PLCs, drives and engineering tools. Networking vendors compete through routing, cybersecurity and centralized management. Industrial specialists differentiate through rugged design, long lifecycle and vertical certifications.

Competition is shifting from hardware specifications toward secure lifecycle management, network visibility, automation, remote diagnostics and multivendor interoperability.

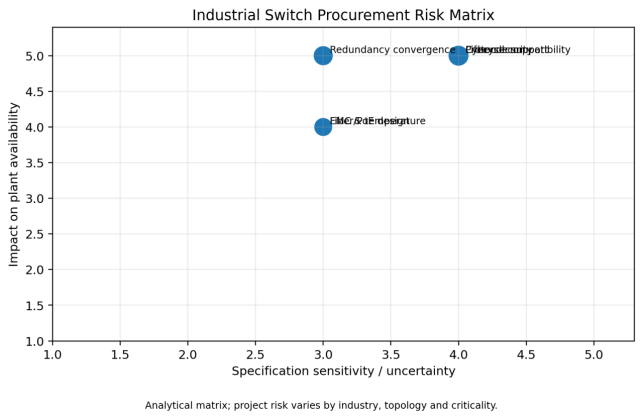

9. Total Cost of Ownership

TCO = Purchase + Engineering + Installation + Configuration + Maintenance + Downtime Risk + Cybersecurity - Residual Value

A low-cost unmanaged switch may be suitable for a simple machine, but it can increase troubleshooting time in a large plant. Managed diagnostics often justify a higher price by reducing production downtime.

Network convergence can reduce cabling and simplify architecture, but it also increases the consequence of configuration errors and cyber incidents. Redundancy and segmentation should match process criticality.

Lifecycle support is a major economic variable. A product that becomes obsolete without a compatible replacement can require engineering changes across an entire installed base.

Figure 5. Industrial switch procurement risk matrix.

10. International Procurement Recommendations

- Define topology, bandwidth, latency, redundancy and environmental requirements before selecting ports.

- Use managed switches for critical or geographically distributed systems where diagnostics reduce downtime.

- Verify support for the exact industrial protocols, multicast behavior and time-synchronization profiles.

- Specify temperature, EMC, vibration, surge, ingress protection and hazardous-area requirements explicitly.

- Evaluate IEC 62443 evidence, vulnerability-disclosure process and firmware-support policy.

- Confirm PRP, HSR, MRP, RSTP or other redundancy behavior through interoperability tests.

- Calculate PoE power budget at the highest ambient temperature and expected cable length.

- Standardize optics, connectors, firmware versions and configuration backups.

- Require FAT testing with representative PLCs, relays, cameras and network-management tools.

- Compare lifecycle support and downtime risk rather than purchase price alone.

11. Market Outlook, 2026-2030

The industrial Ethernet switch market is likely to maintain high-single-digit growth as Ethernet expands into new factory nodes and critical infrastructure. Managed products should grow faster than basic unmanaged devices.

TSN adoption will accelerate, but established protocol ecosystems will remain important. The likely market direction is convergence through common Ethernet infrastructure rather than immediate protocol uniformity.

Cybersecurity requirements will become stricter through regulation, customer policies and insurance. Secure development, signed firmware and long-term vulnerability support will become competitive differentiators.

10-Gigabit, PoE, fiber aggregation and edge-management functions will expand as machine vision and industrial AI increase traffic. The strongest suppliers will combine rugged hardware, secure software, vertical certification and global service.

Conclusion

Industrial Ethernet switches are evolving from connectivity components into operational infrastructure. Ethernet's share of new industrial nodes continues to rise, while TSN, cybersecurity and IT/OT convergence increase the value of managed and rugged platforms.

For buyers, the correct decision is based on availability, diagnostics, environmental performance, security and lifecycle support. The cheapest switch can become the most expensive option when production downtime or forced migration is included.

Through 2030, competitive advantage will move toward secure, deterministic and manageable industrial networks rather than hardware port count alone.