Executive Summary

Membrane bioreactors (MBRs) combine biological wastewater treatment with membrane filtration, replacing the conventional secondary clarifier and producing a consistently low-solids effluent. The technology is increasingly selected for water reuse, space-constrained plants, industrial recycling and projects that require reliable removal of suspended solids, bacteria and biodegradable contaminants.

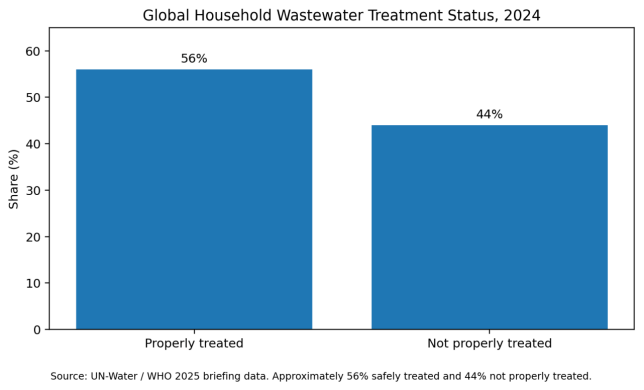

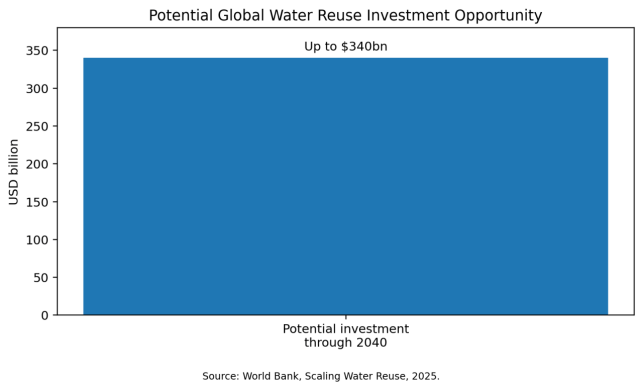

The market is supported by a large global wastewater-treatment gap. UN-Water's latest public data indicate that approximately 44% of household wastewater is not properly treated. At the same time, the World Bank estimates that municipal and industrial water reuse could unlock up to USD 340 billion of investment by 2040. MBR is well positioned within this investment cycle because it can produce an effluent suitable for direct reuse or as stable feedwater for reverse osmosis and advanced polishing.

MBR is not automatically the lowest-cost treatment route. It normally requires more membrane-area management, scouring air, pretreatment, cleaning and specialist operation than conventional activated sludge. The business case becomes strongest when land is expensive, discharge limits are strict, reuse water has economic value or the alternative requires large clarifiers and tertiary filters.

The key commercial variables are membrane flux, permeability, aeration demand, cleaning frequency, membrane life, recovery, sludge characteristics and guaranteed effluent quality. International procurement should therefore be based on normalized lifecycle performance, not simply the initial membrane or package price.

Key Findings

- Global wastewater-treatment and reuse investment provides a strong structural demand base for MBR technology.

- MBR is most competitive where footprint, reuse quality and process stability have high economic value.

- Submerged hollow-fiber and flat-sheet membranes dominate municipal and industrial applications, but each has different fouling, cleaning and maintenance characteristics.

- Membrane scouring and biological aeration are major operating-cost centers; poor air control can destroy lifecycle economics.

- Pretreatment quality strongly influences membrane life and cleaning frequency.

- MBR plus reverse osmosis is a leading configuration for high-grade industrial reuse, but concentrate management becomes a major project constraint.

- International buyers should specify guaranteed flux, permeability, energy consumption, cleaning regime, membrane life and replacement pricing.

Figure 1. Global household wastewater treatment status.

1. Product Definition and Market Scope

An MBR integrates an activated-sludge or other biological process with microfiltration or ultrafiltration membranes. The membrane physically retains suspended solids and biomass, allowing the biological reactor to operate at higher mixed-liquor concentrations than many conventional systems.

Most commercial systems use submerged membranes installed inside a bioreactor or separate membrane tank. Sidestream systems circulate mixed liquor through external membrane modules and are used in selected industrial or high-strength applications. Municipal systems commonly use hollow-fiber or flat-sheet submerged modules.

MBR equipment packages can include screens, equalization, biological tanks, membrane modules, blowers, pumps, chemical-cleaning systems, instrumentation, PLC/SCADA, sludge handling and commissioning. Commercial comparisons are difficult when suppliers include different civil, electrical and pretreatment scopes.

|

MBR Configuration |

Typical Application |

Main Advantages |

Main Trade-Off |

|

Submerged hollow fiber |

Municipal and industrial reuse |

High packing density and broad installed base |

Sensitive to hair, fibers and poor screening |

|

Submerged flat sheet |

Small to medium plants and industrial wastewater |

Robust operation and simpler visual inspection |

Lower packing density and larger membrane footprint |

|

Sidestream MBR |

High-strength industrial wastewater |

High crossflow and external module access |

Higher pumping energy and more complex hydraulics |

|

Anaerobic MBR |

High-strength wastewater and resource recovery |

Low aeration demand and biogas potential |

Membrane fouling, dissolved methane and temperature sensitivity |

|

MBR + RO |

High-quality industrial and municipal reuse |

Stable low-turbidity RO feed and high reuse quality |

Higher energy, chemical use and concentrate-management cost |

2. Global Demand Drivers

Water reuse is the strongest high-value growth driver. MBR effluent has low suspended solids and turbidity, making it suitable for irrigation, cooling, industrial washing and as pretreatment for advanced reuse. The World Bank expects reuse capacity to expand significantly by 2040 if regulations, finance and project structures improve.

Urban density supports compact MBR plants. Replacing secondary clarifiers and tertiary filters can reduce footprint, which is valuable in cities, resorts, airports, hospitals and industrial parks.

Stricter nutrient, pathogen and micropollutant rules create demand for stable biological and solids separation. The European Union's revised Urban Wastewater Treatment Directive entered into force on 1 January 2025 and strengthens treatment coverage, nutrient removal, micropollutant control and energy objectives.

Industrial water security is another major driver. Semiconductor, pharmaceutical, food, beverage, textile, chemical and mining companies increasingly treat wastewater as an internal resource rather than a disposal stream.

Figure 2. Potential global water-reuse investment opportunity.

3. Regional Market Analysis

3.1 North America

North American demand is concentrated in water-stressed states, industrial reuse, decentralized treatment and upgrades where land is constrained. MBR has a strong record in municipal reuse and industrial applications. Buyers emphasize operator support, energy guarantees, membrane replacement terms and local spare inventory.

3.2 Europe

Europe has a mature base of municipal and industrial MBR installations. The revised wastewater directive, water scarcity and stricter nutrient and micropollutant requirements support additional demand. Energy neutrality and chemical reporting will push suppliers toward lower-air-demand membranes and more intelligent control.

3.3 China and Asia-Pacific

China has one of the world's largest MBR manufacturing and project-delivery ecosystems, covering membranes, packages and EPC. Japan and South Korea have extensive membrane expertise, while Singapore and Australia emphasize water reuse. India and Southeast Asia offer growth through urbanization, industrial parks and decentralized infrastructure.

3.4 Middle East and North Africa

Severe water scarcity and high reuse demand favor MBR for municipal effluent polishing, hotels, industrial zones and compact urban plants. High temperature, salinity and energy cost require careful membrane, aeration and corrosion design.

3.5 Latin America

Industrial reuse, mining, food processing and urban growth create demand, particularly in Mexico, Brazil, Chile, Colombia and Peru. Projects must account for local operator capability, chemical supply and membrane logistics.

3.6 Sub-Saharan Africa

MBR opportunities exist in hotels, hospitals, industrial facilities, mining and high-value reuse, but the technology must be matched to reliable power, skilled operators and chemical availability. Simpler modular systems may be more viable than highly automated plants in remote locations.

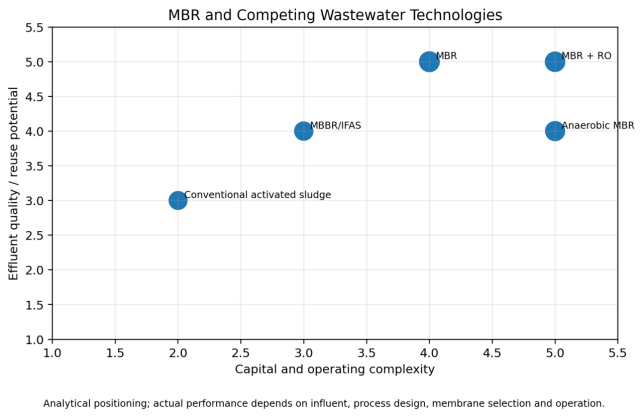

4. Technology and Membrane Selection

Membrane material, pore size, configuration and surface characteristics affect permeability, fouling and chemical tolerance. Common polymeric materials include PVDF, PES and related engineered polymers. Ceramic membranes are used in selected severe industrial applications but remain more expensive.

Hollow-fiber membranes provide high packing density and are widely used in large municipal systems. Flat-sheet modules can be robust and easier to inspect but require more tank volume for the same membrane area.

Flux should be evaluated as a seasonal and sustainable operating parameter rather than a maximum catalogue value. Temperature, mixed-liquor characteristics, salinity, fats, oils, fibers and cleaning strategy all affect sustainable flux.

The MBR should be designed as a biological and membrane system, not as a membrane attached to a conventional aeration tank. Sludge-retention time, dissolved oxygen, mixed-liquor suspended solids and nutrient-removal zones affect fouling and effluent quality.

Figure 3. MBR and competing wastewater-treatment technologies.

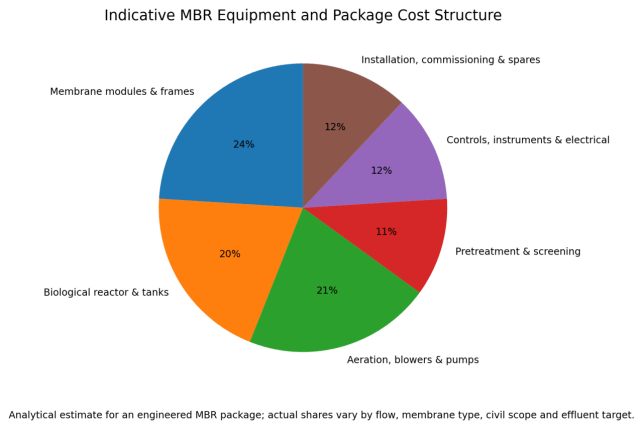

5. Price and Cost Structure

MBR project cost depends on hydraulic flow, organic and nutrient loading, membrane area, redundancy, pretreatment, civil construction and effluent requirement. A price per cubic metre per day is misleading when wastewater characteristics and operating guarantees differ.

Membrane modules and frames form a significant equipment-cost share, but aeration, pumps, tanks and controls are equally important. In retrofit projects, civil constraints and hydraulic modifications can be more expensive than the membrane itself.

Pretreatment is a critical economic item. Fine screening, grease removal, equalization and grit control reduce irreversible fouling and protect membrane modules. Saving money on pretreatment can increase cleaning, downtime and membrane replacement cost.

Buyers should request membrane replacement prices for multiple future years. Low initial package pricing can be offset by proprietary module dependence and high long-term replacement cost.

Figure 4. Indicative MBR equipment and package cost structure.

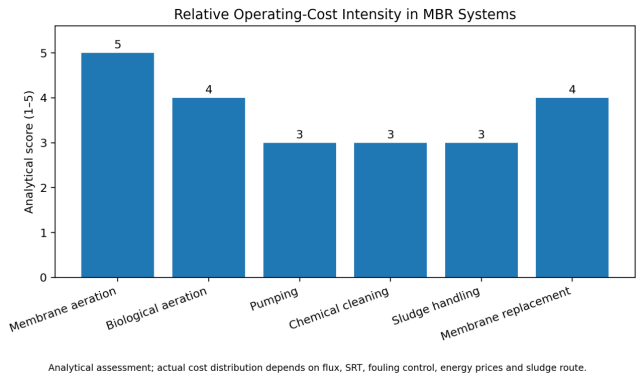

6. Operating Cost and Lifecycle Economics

Membrane scouring air is commonly one of the largest MBR operating costs. Continuous high-rate aeration can maintain permeability but waste electricity. Modern systems use intermittent scouring, cyclic relaxation, flux control and permeability-based cleaning to reduce energy.

Biological aeration remains important for carbon and nitrogen removal. Fine-bubble diffuser efficiency, blower turndown, dissolved-oxygen control and alpha-factor assumptions should be reviewed during procurement.

Chemical cleaning includes maintenance cleaning and recovery cleaning. Sodium hypochlorite, citric acid or other chemicals may be used depending on membrane and foulant. Cleaning frequency affects membrane life, labor and plant availability.

Membrane replacement is a periodic lifecycle cost rather than an emergency event. Expected life depends on operating discipline, chemical exposure, physical damage and module design. Buyers should compare expected replacement intervals under the guaranteed operating conditions.

TCO = Capital + Energy + Chemicals + Membrane Replacement + Labor + Sludge + Downtime - Reuse Water Value

Figure 5. Relative operating-cost intensity in MBR systems.

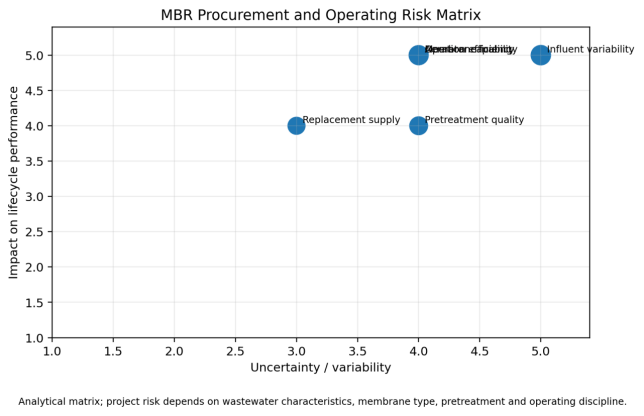

7. Fouling, Pretreatment and Process Risk

Fouling is the defining operational risk in MBR. It includes reversible cake-layer formation, pore blocking, organic adsorption, inorganic scaling and biological fouling. The correct response depends on the foulant; excessive chemical cleaning can damage membranes without correcting the root cause.

Influent fibers, hair, grease and plastics can wrap or blind membrane modules. Fine screening must match the membrane supplier's requirements and should include redundancy and bypass management.

High salinity, solvents, oils, shock toxic loads and rapid temperature changes can affect both biomass and membrane performance. Difficult industrial wastewater usually requires pilot testing or robust reference data.

Transmembrane pressure, permeability, airflow, mixed-liquor properties and cleaning history should be trended continuously. Performance guarantees should define the measurement conditions and required corrective actions.

Figure 6. MBR procurement and operating risk matrix.

8. Supply Chain and Manufacturing

The MBR supply chain includes membrane polymer or ceramic media, module housings, headers, diffusers, blowers, permeate pumps, backwash systems, instruments, chemicals and automation. Membrane-module compatibility is a strategic issue because replacement modules may be proprietary.

Factory manufacturing quality affects potting integrity, fiber breakage, weld quality, header sealing and module dimensions. Suppliers should provide traceability and quality-control records.

International projects require careful shipping and storage. Membranes may need wet preservation or controlled storage, and prolonged exposure to heat or freezing can damage some products. Commissioning should follow defined wetting and preservation procedures.

9. Digitalization and Performance Optimization

Digital control can improve MBR economics through flux optimization, aeration control, permeability-based cleaning and early fouling detection. The value depends on reliable sensors and competent process models.

Online transmembrane pressure, flow, temperature, dissolved oxygen, ammonia, nitrate and turbidity data can support predictive operation. However, sensors require cleaning and calibration, especially in high-solids environments.

Remote support is valuable for decentralized and industrial plants, but cybersecurity, access control, data ownership and software support should be contractually defined.

10. Competitive Landscape

The market includes global membrane and water-technology suppliers, specialist module manufacturers, EPC firms and regional package-system companies. Major participants include Kubota, Mitsubishi Chemical Aqua Solutions, Veolia Water Technologies, SUEZ, Toray, MANN+HUMMEL, Koch Separation Solutions and numerous Chinese and regional suppliers.

Competitive differentiation increasingly depends on sustainable flux, low aeration demand, module durability, cleaning recovery, replacement economics and long-term technical support.

Chinese suppliers are competitive in membrane cost, modular systems and complete EPC delivery. International growth depends on validated references, transparent guarantees, membrane traceability, local service and replacement availability.

11. International Procurement Recommendations

- Complete representative influent characterization, including peak and shock loads, before final design.

- Specify guaranteed net permeate flow at seasonal minimum temperature and defined cleaning downtime.

- Request sustainable flux and permeability data rather than maximum catalogue flux.

- Define guaranteed energy consumption separately for biological aeration, membrane aeration and pumping.

- Verify screen opening, grease control and pretreatment requirements.

- Specify cleaning chemicals, frequency, concentration, waste handling and membrane compatibility.

- Require membrane-life assumptions and future replacement pricing.

- Use pilot testing for difficult industrial wastewater or ambitious reuse targets.

- Define redundancy, bypass operation and response to fiber or module failure.

- Compare lifecycle cost and reuse-water value rather than initial module price.

12. Market Outlook, 2026-2030

The MBR market outlook is favorable because water reuse, urban density and industrial water security continue to improve the technology's business case. Growth is likely to be stronger in reuse-oriented projects than in basic discharge-only treatment.

Energy reduction will remain the main innovation target. Suppliers will compete through lower scouring-air demand, smarter cyclic operation, better diffuser design and more efficient blowers.

Industrial MBR applications will expand, but projects will remain wastewater-specific. Standard municipal designs cannot be transferred directly to oily, saline, toxic or high-strength effluents.

MBR plus RO and advanced oxidation will gain share in high-grade reuse, while anaerobic MBR may develop in high-strength and resource-recovery applications. Concentrate management and dissolved methane will remain constraints.

The strongest suppliers will combine membrane manufacturing, process engineering, digital optimization, transparent lifecycle guarantees and local replacement support.

Conclusion

The global membrane bioreactor market is moving from a premium wastewater-treatment niche toward a core technology for compact treatment and water reuse. Its growth is supported by treatment gaps, stricter regulation and the rising economic value of recycled water.

MBR economics depend less on the initial membrane price than on sustainable flux, aeration energy, fouling control, membrane life and operator discipline. Poorly designed pretreatment or unrealistic flux assumptions can erase the advantages of the technology.

Through 2030, the most competitive solutions will deliver reliable reuse-quality effluent with lower energy demand, transparent replacement economics and strong local technical support.