Executive Summary

Wastewater treatment equipment is moving from a compliance-driven market toward a resource-recovery and water-security market. Municipal utilities still need screens, clarifiers, aeration systems, pumps, blowers, sludge equipment and disinfection. Industrial customers increasingly require advanced biological treatment, membranes, dissolved-air flotation, evaporation, zero-liquid-discharge systems and digital monitoring to reduce fresh-water use and production risk.

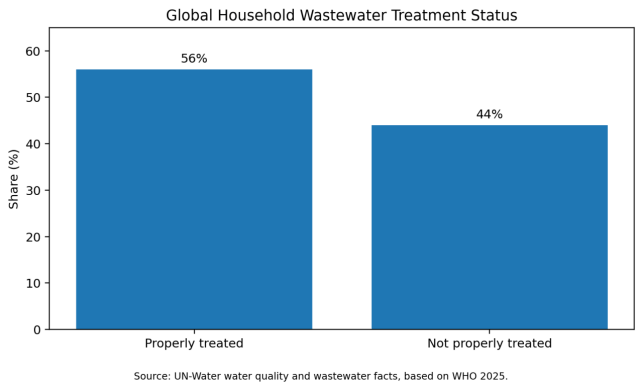

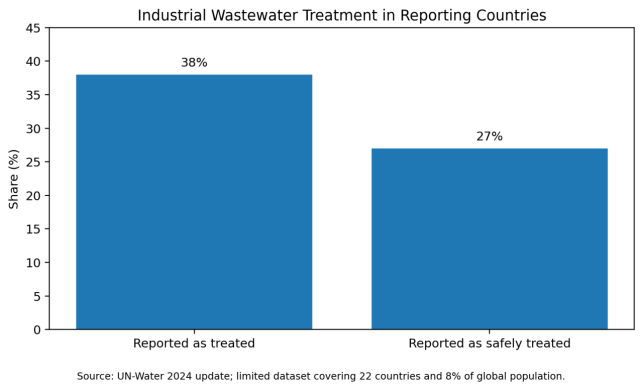

The underlying demand gap remains large. UN-Water reports that approximately 44% of household wastewater is not properly treated. Industrial reporting is more limited: in a dataset covering 22 countries and 8% of the global population, only 38% of industrial wastewater was reported as treated and 27% as safely treated. These figures should not be extrapolated mechanically to the whole world, but they show the scale of the unmet treatment need.

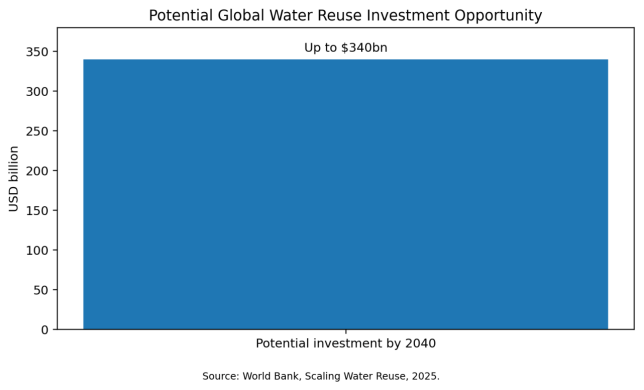

Water reuse is becoming a major investment driver. The World Bank's 2025 Scaling Water Reuse report estimates that expanded municipal and industrial reuse could unlock up to USD 340 billion of investment by 2040. This shifts equipment demand toward tertiary filtration, ultrafiltration, reverse osmosis, advanced oxidation, disinfection, monitoring and brine or concentrate management.

The key procurement lesson is that low capital cost does not guarantee low treatment cost. Electricity, aeration efficiency, chemical consumption, membrane replacement, sludge disposal, operator skill, influent variability and regulatory compliance determine the real total cost of ownership. Successful projects begin with wastewater characterization and guaranteed process performance rather than equipment catalogues.

Key Findings

- Global wastewater treatment gaps remain substantial in both municipal and industrial sectors.

- Water reuse, industrial circularity and drought resilience are becoming as important as discharge compliance.

- Aeration, pumping and sludge handling are major operating-cost centers, making energy efficiency central to equipment selection.

- MBR, advanced filtration and RO can produce high-quality reuse water but increase energy, fouling and concentrate-management requirements.

- Industrial wastewater markets are highly application-specific; food, chemicals, pharmaceuticals, mining, textiles and semiconductors require different process trains.

- Europe's revised urban wastewater rules are expanding treatment coverage, micropollutant removal and energy-neutrality requirements.

- International procurement should be based on guaranteed effluent quality, normalized energy and chemical consumption, sludge yield and lifecycle service.

Figure 1. Global household wastewater treatment gap.

1. Product Scope and Market Definition

Wastewater treatment equipment includes mechanical, biological, chemical, membrane and thermal systems used to remove solids, organic matter, nutrients, pathogens, metals, salts and micropollutants from municipal or industrial wastewater.

The equipment boundary can include intake screening, grit removal, equalization, pumps, clarifiers, aeration, biological reactors, media, membranes, chemical dosing, flotation, filtration, disinfection, sludge thickening, dewatering, digestion, odor control, instrumentation and supervisory control.

Market-size estimates vary because some studies count only equipment, while others include EPC, civil works, chemicals, membranes, operation and maintenance or complete water-reuse projects. This report therefore emphasizes treatment gaps, regulatory drivers, technology adoption and public investment signals rather than one unsupported global market value.

|

Equipment / Process |

Typical Function |

Main Applications |

Primary Cost Driver |

|

Screens, grit and primary treatment |

Remove large solids, sand and settleable material |

Municipal plants and industrial pretreatment |

Hydraulics, wear resistance and automation |

|

Activated sludge / biological reactors |

Remove biodegradable organics and nutrients |

Municipal and many industrial plants |

Aeration energy and process control |

|

MBBR / IFAS |

Increase biomass concentration in compact reactors |

Retrofits, municipal and industrial treatment |

Carrier media, aeration and retention |

|

MBR |

Combine biological treatment with membrane separation |

Reuse, space-constrained and high-quality effluent |

Membrane cost, aeration and fouling control |

|

DAF |

Remove oils, grease and fine suspended solids |

Food, pulp, mining and industrial pretreatment |

Chemicals, recycle pressure and sludge handling |

|

RO / NF polishing |

Remove dissolved salts and small contaminants |

High-grade reuse and ZLD pretreatment |

Energy, membrane replacement and concentrate |

|

Sludge dewatering |

Reduce sludge volume |

All biological and chemical plants |

Polymer, energy and disposal route |

2. Global Demand Drivers

The largest structural driver is incomplete sanitation and treatment infrastructure. Population growth, urbanization and industrialization continue to increase wastewater volumes faster than treatment capacity in many regions.

Water scarcity is changing the economics of treatment. Wastewater is increasingly treated as a local water source for industrial cooling, irrigation, groundwater recharge and, in selected cases, indirect or direct potable reuse. Reuse projects require more reliable tertiary and advanced treatment than conventional discharge-only plants.

Regulation is becoming stricter. The revised EU Urban Wastewater Treatment Directive entered into force on 1 January 2025. It expands obligations to smaller agglomerations, strengthens nutrient removal, introduces quaternary treatment for micropollutants and establishes energy-neutrality objectives for larger systems.

Industrial decarbonization and supply-chain resilience also support investment. Manufacturers seek lower water withdrawal, reduced discharge fees and more stable access to process water. Semiconductor, pharmaceutical, food, textile, chemical and mining facilities are major technology-intensive segments.

Figure 2. Industrial wastewater treatment in reporting countries.

3. Regional Market Analysis

3.1 North America

The market is driven by aging municipal infrastructure, nutrient limits, PFAS and micropollutant concerns, industrial reshoring and water reuse in dry western states. Utilities value energy-efficient blowers, advanced controls and asset renewal. Industrial projects require strong local service and regulatory familiarity.

3.2 Europe

Europe is entering a new compliance and modernization cycle under the revised Urban Wastewater Treatment Directive. Demand will expand for nutrient removal, advanced micropollutant treatment, energy recovery, digital monitoring and small-community treatment. Equipment suppliers must support stringent environmental, chemical and energy reporting.

3.3 China and Asia-Pacific

China has a broad treatment-equipment and EPC supply chain and significant experience in municipal, industrial and zero-discharge projects. India and Southeast Asia have large infrastructure gaps and growing industrial demand. Japan, South Korea, Singapore and Australia emphasize reuse, compact systems and advanced control.

3.4 Middle East and North Africa

Severe water scarcity makes reuse strategically important. Municipal treated sewage effluent, industrial recycling and desalination-brine integration are major opportunities. High salinity, temperature and energy cost strongly influence equipment design.

3.5 Sub-Saharan Africa

The region has substantial unmet sanitation and industrial-treatment needs. Decentralized, modular and low-energy systems can be more viable than complex centralized plants where grids, chemicals and skilled operators are limited. Project finance and long-term operation are critical.

3.6 Latin America

Municipal treatment expansion, mining, pulp and paper, food processing and urban reuse support demand. Brazil, Mexico, Chile, Colombia and Peru are important markets. Sludge disposal, energy cost and remote-site service are frequent project constraints.

Figure 3. Potential global water-reuse investment opportunity.

4. Technology Routes

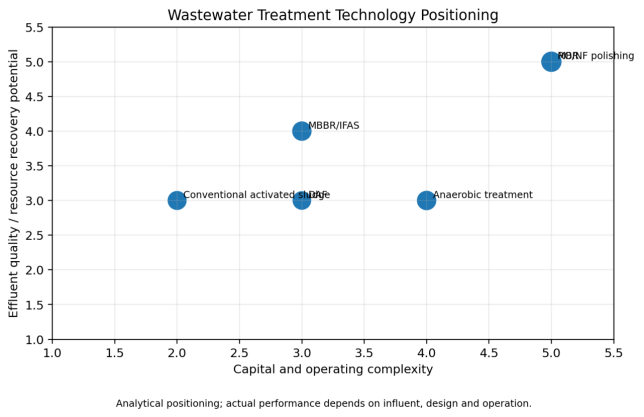

Conventional activated sludge remains the largest treatment base because it is proven and flexible. Its main weakness is energy-intensive aeration and the need for large clarifiers and skilled process control.

MBBR and IFAS add attached-growth media to increase biomass retention. They are attractive for plant upgrades where civil expansion is difficult, but media retention, mixing and aeration design are important.

MBR replaces secondary clarification with membrane separation. It produces low-solids effluent suitable for reuse and reduces footprint. The trade-offs are membrane capital cost, scouring energy, chemical cleaning and fouling risk.

DAF is widely used for oily wastewater, food processing, pulp and paper and algae removal. Performance depends on coagulation chemistry, recycle pressure, bubble generation and sludge handling.

Anaerobic treatment can recover biogas from high-strength wastewater and reduce aeration demand. It is especially relevant to food, beverage, pulp, distilling and selected chemical effluents. Stable temperature, toxicity control and post-treatment remain important.

RO, nanofiltration, advanced oxidation and activated carbon are increasingly used for reuse and micropollutant removal. These technologies shift the challenge from pollutant removal to concentrate, brine, spent media and energy management.

Figure 4. Wastewater treatment technology positioning.

5. Price and Cost Structure

Wastewater equipment prices depend on flow, contaminant loading, discharge limits, redundancy, automation and material selection. A price per cubic metre per day is only meaningful when influent and effluent specifications are identical.

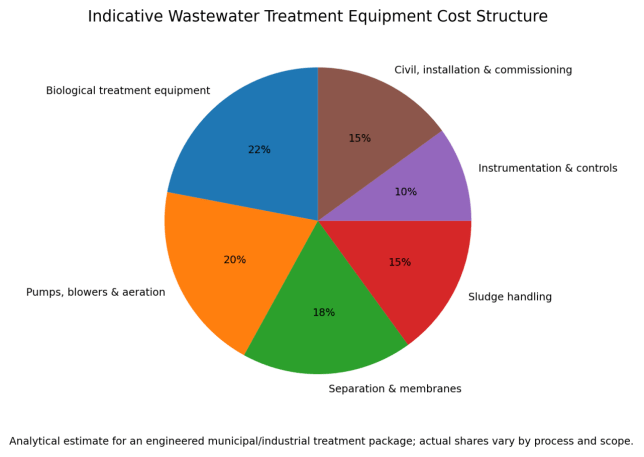

Biological equipment and aeration often represent a large share of municipal and industrial project cost. Pumps, blowers and diffusers influence both capital and long-term electricity consumption. Membranes can reduce footprint but add replacement and cleaning cost.

Corrosion resistance can materially affect price. Stainless steel, duplex alloys, FRP, coated carbon steel and engineering plastics are selected according to chlorides, pH, solvents and temperature.

Instrumentation and automation are becoming more valuable because online dissolved oxygen, ammonia, nitrate, phosphate, turbidity and membrane-pressure data allow plants to reduce energy and chemical use.

Figure 5. Indicative wastewater treatment equipment cost structure.

6. Energy, Chemicals and Lifecycle Economics

The water sector accounts for approximately 4% of global electricity consumption according to the IEA, and wastewater treatment represents roughly one quarter of water-sector electricity use. Aeration is commonly the largest electricity load in biological plants.

Energy performance should be evaluated as normalized consumption, such as kWh per cubic metre treated or kWh per kilogram of pollutant removed. Guarantees must specify influent loading, temperature and effluent requirements.

Chemical cost can be substantial in phosphorus removal, pH adjustment, flotation, membrane cleaning and sludge dewatering. A process with lower capital cost may use more chemicals and generate more sludge.

Sludge economics are frequently underestimated. Thickening, digestion, dewatering, transport and disposal can represent a large share of operating cost. Resource recovery through biogas, phosphorus or biosolids can improve economics where regulation and markets allow.

TCO = Capital + Energy + Chemicals + Membranes/Consumables + Labor + Sludge Handling + Compliance + Downtime - Recovered Water/Energy Value

7. Supply Chain and Manufacturing

Key components include pumps, blowers, diffusers, membranes, motors, drives, valves, sensors, dosing systems, filter media, dewatering machines and PLC/SCADA systems. Delivery risk can be concentrated in specialized membranes, large blowers, alloy equipment and certified electrical systems.

Local availability of chemicals, membrane cleaning agents, spare seals and bearings affects plant reliability. International buyers should not assume that all consumables are available in the project country.

Modular skid systems can shorten installation and improve factory quality, but they require accurate hydraulic interfaces and transport planning. Large municipal plants still rely heavily on site civil works and integration.

8. Digitalization and Automation

Digital control is moving from basic SCADA toward model-predictive control, aeration optimization, predictive maintenance and remote support. The business case is strongest where energy prices are high or operator capacity is limited.

Online analyzers can reduce laboratory delay and improve nutrient control, but sensors require calibration, cleaning and replacement. A digital system without maintenance resources can produce poor data and incorrect process decisions.

Cybersecurity is increasingly important because wastewater plants are critical infrastructure. Procurement should define network segmentation, remote-access controls, software backups, alarm management and long-term support.

9. Competitive Landscape

The market includes global water-technology groups, pump and aeration specialists, membrane suppliers, sludge-equipment manufacturers, automation companies and regional EPC contractors. Major names include Veolia Water Technologies, Xylem, SUEZ, Grundfos, Sulzer, Kubota, Toray, DuPont Water Solutions, Alfa Laval, ANDRITZ and many regional suppliers.

Competitive advantage differs by segment. Membrane suppliers compete through flux, fouling resistance and service life. Blower and pump suppliers compete through efficiency and reliability. EPC and system companies compete through process guarantees and integration.

Chinese manufacturers are competitive in tanks, pumps, screens, filters, MBR packages, sludge equipment and complete industrial systems. International growth depends on process references, guaranteed performance, documentation, local service and compliance with destination standards.

10. International Procurement Recommendations

- Complete representative wastewater characterization before final process selection.

- Define average, peak and shock loads rather than using only average daily flow.

- Compare guarantees for COD, BOD, TSS, nutrients, pathogens, salinity and reuse quality.

- Require normalized energy, chemical and sludge-production guarantees.

- Evaluate membrane replacement, diffuser life, blower efficiency and spare-parts availability.

- Verify corrosion materials against chloride, pH, solvent and temperature conditions.

- Use pilot testing for difficult industrial wastewater or ambitious reuse targets.

- Clarify civil works, hydraulic interfaces, electrical scope, installation and commissioning responsibilities.

- Assess operator skill, remote support and training requirements.

- Compare total lifecycle cost and compliance risk rather than the lowest equipment quotation.

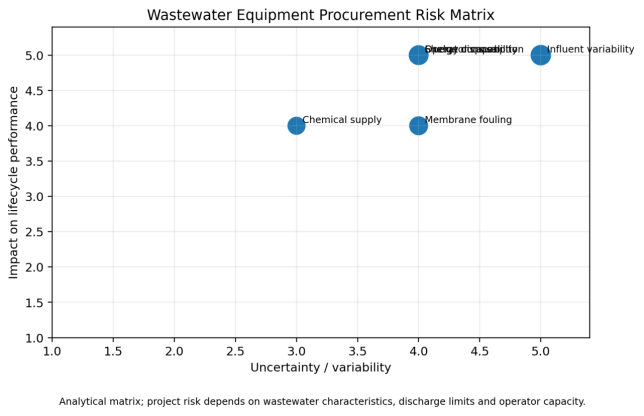

Figure 6. Wastewater equipment procurement risk matrix.

11. Market Outlook, 2026-2030

The global outlook is favorable because treatment gaps, water scarcity and regulation create simultaneous demand. However, growth will be uneven because many projects depend on public finance, tariffs and operating capability.

Water reuse will be one of the fastest-growing higher-value segments, supporting membranes, advanced oxidation, disinfection, monitoring and concentrate treatment.

Energy-efficient aeration, high-efficiency pumps, anaerobic recovery and digital optimization will gain importance as utilities face energy-neutrality and emissions targets.

Modular and decentralized systems will expand in industrial parks, hotels, remote communities and rapidly growing cities, while large urban systems will continue to require major civil and network investment.

Suppliers that combine proven treatment processes, low lifecycle cost, digital control and long-term service will outperform vendors competing only on equipment price.

Conclusion

The wastewater treatment equipment market is moving beyond basic pollution control. Water scarcity, reuse, industrial circularity, micropollutant regulation and energy neutrality are creating a more technology-intensive demand cycle.

For buyers, the most important variables are influent variability, effluent guarantee, energy, chemicals, sludge, operator capability and lifecycle service. A low capital price can create high operating cost or compliance risk.

Through 2030, the strongest opportunities will be in water reuse, industrial recycling, nutrient and micropollutant removal, energy-efficient biological treatment and digital plant optimization.