1. Global Demand and Market Structure

1.1 Automation investment remains structurally high

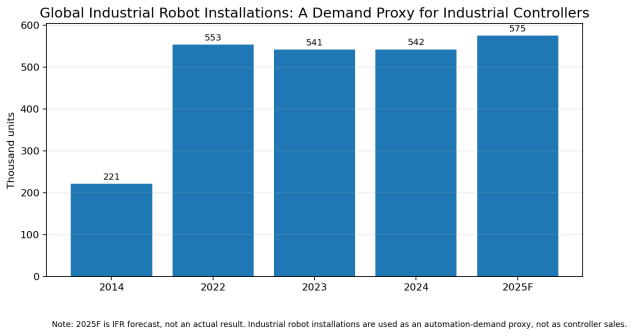

IFR data show that annual industrial robot installations remained above 500,000 units for a fourth consecutive year in 2024. Asia accounted for 74% of new deployments, Europe 16% and the Americas 9%. The installed base reached roughly 4.664 million robots, which implies a growing replacement, retrofit, networking and lifecycle-service requirement in addition to greenfield equipment demand.

Figure 1. Global industrial robot installations, selected years

Source: IFR World Robotics 2025. 2025 is an IFR forecast; 2014–2024 are reported values.

1.2 Asia leads volume; Western markets lead density and compliance intensity

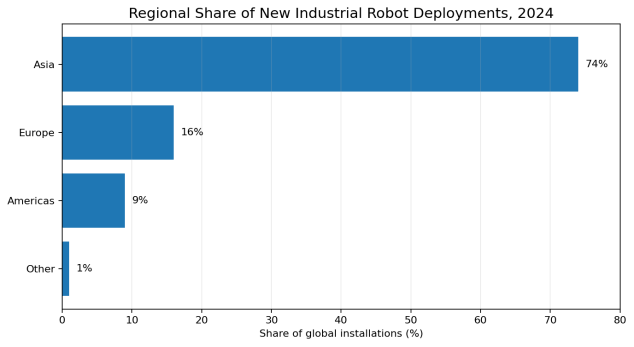

Asia is the dominant deployment region, driven by China, Japan and Korea as well as rising installations in India. However, volume alone does not equal market accessibility. China, Japan and Korea have deep domestic ecosystems and strong incumbent preferences. India and Southeast Asia are more open to new platforms where local machine builders need cost-effective architectures and application support.

Figure 2. Regional share of new industrial robot deployments, 2024

Source: IFR World Robotics 2025. Shares may not total 100% due to rounding.

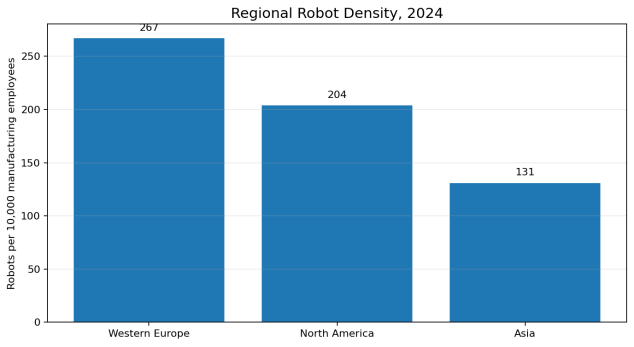

Western Europe reached 267 robots per 10,000 manufacturing employees in 2024, compared with 204 in North America and 131 in Asia. High density indicates a large installed base and recurring retrofit demand, but it also signals mature engineering expectations, strict qualification and strong incumbent ecosystems.

Figure 3. Regional robot density, 2024

Source: IFR, “Robot Density Surges in Europe, Asia, and Americas,” published April 2026.

1.3 Country demand is concentrated, but opportunity is not

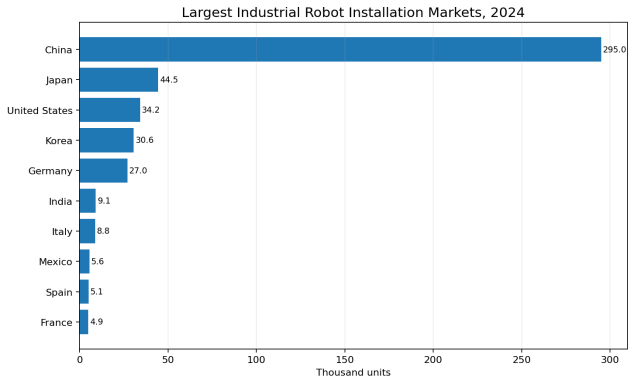

China represented 54% of global industrial robot deployments in 2024, while Japan, the United States, Korea and Germany remained major automation markets. India installed a record 9,120 units and ranked sixth worldwide. Mexico installed 5,600 units, with automotive accounting for 63% of installations. These figures point to different controller opportunities: mature markets emphasize replacement, security and integration; growth markets emphasize new capacity, OEM adoption and local application engineering.

Figure 4. Largest industrial robot installation markets, 2024

Source: IFR World Robotics 2025; values rounded in the chart.

1.4 Competition is shifting from hardware to architecture and lifecycle

The global controller landscape remains anchored by major automation vendors with extensive installed bases, engineering software, channel networks and certified product families. New entrants rarely displace an incumbent by offering a cheaper CPU alone. They win when they solve a defined problem: reducing machine cost, simplifying motion integration, supporting an unavailable legacy system, providing an open communication stack, meeting a cybersecurity requirement or delivering faster local engineering response.

2. Regional Market Opportunities

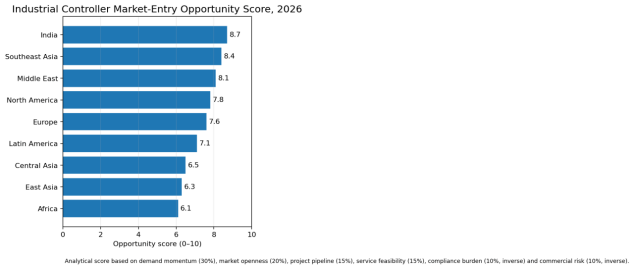

The opportunity ranking below is an analytical market-entry score, not a published market-size statistic. It combines verified demand signals with entry openness, service feasibility, compliance burden and commercial risk.

Figure 5. Industrial controller market-entry opportunity score, 2026

Source: Author analysis based on IFR data, official industrial programs, regulatory requirements and regional commercial conditions.

|

Region |

Opportunity |

Demand logic |

Best offerings |

Preferred entry |

Main barriers |

|

India |

High |

New factories, automotive/electronics expansion, capital-goods demand and rising automation adoption. |

PLC/PAC, distributed I/O, motion packages, machine OEM control, engineering libraries. |

Distributor + OEM design-in + local application team; later local assembly. |

Price pressure, localization expectations, fragmented service coverage. |

|

Southeast Asia |

High |

Manufacturing FDI, electronics, automotive, food, logistics and supply-chain diversification. |

Compact PLC, remote I/O, gateways, motion, machine controllers, energy monitoring. |

Country distributor plus regional application hub; OEM partnerships. |

Different standards and channels across ASEAN; integrator dependence. |

|

Middle East |

High / project-led |

Industrial diversification, utilities, water, oil and gas, mining and logistics projects. |

RTU/process controllers, remote I/O, redundant architectures, hazardous-area packages, service. |

EPC/panel-builder partnerships, approved vendor lists, local service and ICV strategy. |

Project qualification, payment cycles, local-content scoring and harsh environments. |

|

North America |

Medium-high |

Large installed base, reshoring, food/logistics growth and 2025 U.S. robot recovery. |

Certified PLC/PAC, edge control, migration, remote I/O, secure connectivity. |

OEM design-in, specialist integrators, UL/CSA certification and local stock. |

Incumbent lock-in, liability, cybersecurity and 24/7 support expectations. |

|

Europe |

Medium-high |

Large installed base, machinery exports, energy efficiency and regulatory-driven upgrades. |

CE-ready controllers, motion/safety, soft PLC, secure lifecycle, retrofit and migration. |

Machine-builder partnerships and technical distributors; EU documentation support. |

CRA, CE, Machinery Regulation, language and product-lifecycle obligations. |

|

Latin America |

Medium |

Automotive in Mexico/Brazil, food, mining, packaging, water and utilities. |

Compact PLC, I/O, gateways, process/RTU, retrofit kits and training. |

Local distributor/integrator, Spanish/Portuguese tools and regional spares. |

FX, financing, import procedures and uneven service networks. |

|

Central Asia |

Selective |

Mining, oil and gas, utilities, rail and water infrastructure. |

RTU, process controllers, rugged I/O, telemetry and skid packages. |

EPC-led entry and local technical partner. |

Sanctions screening, logistics, currency and project concentration. |

|

East Asia ex-China |

Selective / mature |

High automation intensity in Japan and Korea. |

Niche motion, semiconductor tools, open edge control and OEM modules. |

Technology partnership, local certification and deep OEM integration. |

Strong domestic incumbents, language and long qualification cycles. |

|

Africa |

Selective / project-led |

Mining, food, water, power and industrial zones. |

Rugged compact PLC, remote I/O, telemetry, solar-powered RTU and training. |

EPC, distributor and donor/utility projects; strong remote support. |

Payment risk, spare-parts logistics, skills gaps and fragmented demand. |

2.1 North America

The United States remains the largest automation market in the Americas. IFR reported 34,200 industrial robot installations in 2024, followed by preliminary growth of 11% to 38,000 units in 2025. The 2025 recovery was supported not only by automotive but also by food and other non-automotive industries, indicating demand for flexible machine automation beyond traditional large plants.

The best entry points are OEM machine builders, specialist integrators and retrofit projects where a supplier can prove UL/CSA certification, deterministic performance, secure remote access, diagnostics and North American spare-parts availability. Generic direct-to-end-user sales are less attractive because established plants carry high migration risk and prefer familiar engineering environments.

- Prioritize UL/CSA 61010-1 and 61010-2-201 certification for PLC-class products, plus FCC/EMC requirements where applicable.

- Offer migration tools, tag conversion, tested communication drivers and compatibility with common SCADA/MES architectures.

- Maintain local stock for CPUs, power supplies and I/O modules; buyers will not accept long downtime for imported spares.

2.2 Europe

Europe installed 85,000 industrial robots in 2024, the second-highest annual level on record despite an 8% year-on-year decline. The opportunity is strongest in machine-building supply chains, brownfield modernization, energy efficiency, safety upgrades and secure industrial connectivity. Germany remains the region’s largest market, while Italy, Spain and France support diverse machinery and automotive ecosystems.

Regulation is becoming a product-strategy issue. Regulation (EU) 2023/1230 on machinery applies from 20 January 2027. The EU Cyber Resilience Act (CRA) introduces reporting obligations from 11 September 2026 and its main obligations from 11 December 2027. A connected industrial controller sold into the EU therefore needs a security-by-design process, vulnerability handling, update policy and technical documentation—not only CE test reports.

- Build an EU technical file covering applicable EMC, electrical safety, RoHS, radio and machinery-related requirements.

- Prepare an SBOM, coordinated vulnerability disclosure process, signed firmware/update mechanism and defined support period.

- Use local-language manuals and provide traceable product versions; unstructured firmware variants create compliance and support risk.

2.3 India

India is the strongest broad-based growth opportunity. IFR recorded 9,120 industrial robot installations in 2024, up 7%, with automotive representing 45% of demand. The operational stock reached 52,570 units. Government data show that Production Linked Incentive schemes had attracted more than INR 2.16 trillion in cumulative investment by the end of 2025 across 14 sectors, reinforcing demand for machinery, electronics, automotive, renewable-energy and process-plant automation.

India is attractive for compact and modular PLCs, distributed I/O, servo/motion packages, machine-OEM controllers and application-specific libraries. However, low price alone is not enough. Successful suppliers typically need local field application engineers, training, fast warranty decisions and the ability to adapt to machine-builder requirements.

- Start with three to five OEM verticals—packaging, plastics, food, material handling and renewable-energy manufacturing—rather than nationwide generic distribution.

- Offer local assembly or configured-to-order production only after volume and quality-control processes are stable.

- Design the channel to protect engineering value; uncontrolled discounting can destroy distributor investment in application support.

2.4 Middle East

The Middle East opportunity is driven by industrial diversification and infrastructure projects. Saudi Arabia’s National Industrial Strategy targets more than 36,000 factories by 2035. The UAE’s Operation 300Bn aims to raise industrial GDP contribution from AED 133 billion to AED 300 billion by 2031, with a strong emphasis on advanced technology and In-Country Value. These programs support controllers used in water, oil and gas, mining, logistics, food, utilities and new industrial zones.

Entry should be project-led. Controllers are normally procured within panels, skids, packaged plants, warehouses or EPC systems. Success depends on approved vendor lists, local panel builders, environmental robustness, cybersecurity documentation, Arabic/English support and rapid commissioning response.

- Prioritize RTU/process control, redundant I/O, remote diagnostics, harsh-environment designs and protocol gateways.

- Build local-content evidence and a staged plan for service, configuration or assembly where tender scoring rewards localization.

- Use export-credit insurance and milestone-based payments for EPC and private industrial projects.

2.5 Southeast Asia

ASEAN attracted USD 226 billion in FDI in 2024, up 8% despite a decline in global flows. Manufacturing was a major recipient, and greenfield projects remained strong. Vietnam, Thailand, Malaysia, Indonesia and Singapore form different controller markets: Vietnam and Indonesia emphasize new capacity and cost-performance; Thailand has a mature automotive base; Malaysia and Singapore offer higher-value electronics, semiconductor and process applications.

The commercial model should combine country distributors with one regional application center. Documentation, training and support can be regionalized, but inventory, language and industry relationships remain country-specific.

2.6 Latin America, Africa and Central Asia

Mexico and Brazil are the principal Latin American targets. Mexico benefits from automotive and North American supply-chain integration, while Brazil supports food, mining, pulp and paper, packaging and water applications. Africa and Central Asia are better approached through EPC projects, utilities, mining, oil and gas, water and packaged equipment rather than broad distributor-led catalogue sales.

For these markets, ruggedness, remote support, spare-parts planning and payment protection are more important than offering the largest product range. A narrow, serviceable family of controllers and I/O modules is usually more credible than a fragmented portfolio.

3. Product and Supply Chain Opportunities

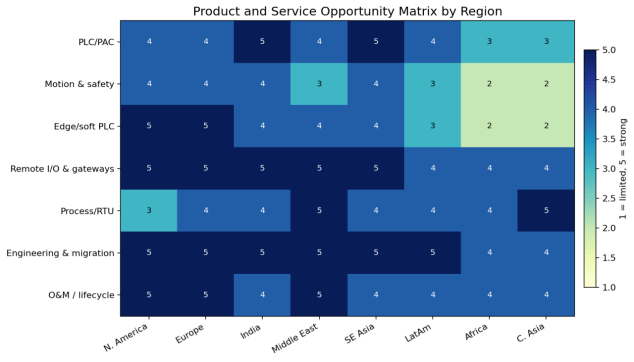

Figure 6. Product and service opportunity matrix by region

Source: Author assessment. Scores are qualitative and based on regional demand, procurement structure, compliance requirements and service economics.

|

Offering |

Best-fit applications |

Opportunity |

Critical condition |

|

Compact and modular PLC |

Machine builders, packaging, food, plastics, material handling. |

High volume and broad demand; suitable for India, ASEAN and Latin America. |

Competes directly on price; requires reliable software and channel discipline. |

|

PAC / high-performance controller |

Multi-axis machines, robotics cells, electronics and complex lines. |

Higher value, more open to performance and architecture differentiation. |

Requires deterministic benchmarks, advanced engineering tools and integration proof. |

|

Motion and safety control |

Servo machines, robotics, converting, presses and intralogistics. |

Strong margins and ecosystem lock-in when delivered as a tested package. |

Certification, functional safety competence and application support are essential. |

|

Remote I/O and protocol gateways |

Brownfield plants, distributed machines, utilities and multi-vendor systems. |

Often the fastest path into incumbent environments without replacing the main PLC. |

Protocol quality, diagnostics and environmental testing determine acceptance. |

|

RTU / process and infrastructure control |

Water, pipelines, power, mining, oil and gas and remote assets. |

High project value and demand in Middle East, Africa and Central Asia. |

Long qualification, cybersecurity, redundancy and environmental requirements. |

|

Edge and soft PLC |

IT/OT convergence, analytics, virtualized control and machine data. |

Differentiated growth segment in Europe and North America. |

Must prove real-time behavior, lifecycle support, container/OS security and licensing clarity. |

|

Engineering, migration and O&M |

Installed-base upgrades, legacy replacement and multi-site standardization. |

Recurring revenue and the strongest defense against hardware commoditization. |

Requires local experts, documentation, source-code governance and service SLAs. |

3.1 Opportunities for large suppliers versus SMEs

Large automation suppliers are best positioned for safety-certified platforms, process control, global OEM frameworks, redundant systems and multi-country lifecycle contracts. SMEs can compete more effectively in remote I/O, protocol conversion, machine-specific controllers, embedded OEM modules, engineering tools, vertical application libraries and regional retrofit services.

A small supplier should avoid copying a full-line automation portfolio. It should select one architectural advantage and one vertical use case—for example, EtherCAT motion for packaging machines, rugged RTUs for solar-powered water assets, or secure edge control for food processing—and build references around that combination.

4. Project-Based Delivery Pathways

|

Entry model |

Best use |

Advantages |

Risks |

Execution requirement |

|

Direct export to distributor |

Standard products with repeatable demand. |

Fast market coverage and low fixed cost. |

Weak application control and price erosion. |

Use selective distribution, certified training and protected project registration. |

|

OEM design-in |

Machine builders requiring recurring controller supply. |

Repeat volume, application lock-in and scalable references. |

Long validation and customization burden. |

Provide reference designs, sample kits, libraries and supply continuity commitments. |

|

Panel builder / integrator partnership |

Industrial projects and brownfield automation. |

Access to end users and engineering resources. |

Partner may favor incumbent brands. |

Create margin for engineering, joint demos and technical escalation support. |

|

EPC / packaged-system supply |

Water, oil and gas, power, mining and infrastructure. |

Large project value and cross-selling of I/O, networking and service. |

Tender qualification, payment and schedule risk. |

Bid through approved partners, define interfaces and insure receivables. |

|

Local configuration / assembly |

Markets with localization scoring or volume. |

Shorter lead times and stronger tender position. |

Quality drift, IP leakage and working-capital exposure. |

Begin with configuration and final test before deeper localization. |

|

Lifecycle service network |

Installed-base support, migration, cybersecurity and training. |

Recurring revenue and customer retention. |

Requires people, spare parts and governance. |

Use tiered SLAs, remote diagnostics and documented patch/support policies. |

4.1 Recommended staged entry sequence

- Phase 1 — Validate: select two target countries and two verticals; certify a narrow product family; recruit one technical distributor or OEM partner per market; close five reference projects.

- Phase 2 — Localize service: establish application engineering, spare-parts stock, training and warranty authority; create local-language documentation and vertical libraries.

- Phase 3 — Scale: add configured-to-order assembly, EPC frameworks, lifecycle service contracts and broader product families only after repeatable demand is proven.

5. Standards, Certification and Localization

Standards should be selected according to product function and target market. Listing every possible certification is neither accurate nor commercially useful. The matrix below identifies the most relevant frameworks for industrial controllers and controller-based systems.

|

Context |

Relevant frameworks |

Why they matter |

Required action |

|

Global product design |

IEC 61131-2; IEC 61131-3:2025; IEC 61010-2-201 |

Equipment requirements, programming languages and safety requirements for control equipment. |

Maintain traceable hardware/firmware versions and test evidence. |

|

Industrial cybersecurity |

IEC 62443-4-1 and 62443-4-2 |

Secure development lifecycle and technical security requirements for IACS components. |

Create SDL governance, threat models, SBOM, secure update and vulnerability handling. |

|

Functional safety |

IEC 61131-6; IEC 61508; IEC 62061; ISO 13849-1 as applicable |

Safety PLCs and safety-related control systems. |

Independent certification, safety manual, systematic capability and change control. |

|

European Union |

CE conformity; EMC, LVD, RoHS, RED where applicable; Machinery Regulation for relevant machinery/safety components; CRA for connected products in scope |

Market access, safety, EMC, environmental and cybersecurity obligations. |

EU technical file, declaration, responsible economic operator and lifecycle cybersecurity evidence. |

|

United States / Canada |

UL/CSA 61010-1 and 61010-2-201; FCC/EMC as applicable; panel/system rules such as UL 508A |

PLC product certification and integration into industrial control panels. |

Use accredited certification, controlled components and local field-evaluation planning. |

|

Hazardous areas |

ATEX / IECEx / North American hazardous-location certification as applicable |

Oil, gas, chemicals, mining and dust/gas environments. |

Do not claim suitability without certified enclosure/system configuration. |

|

Process and infrastructure projects |

Project specifications, IEC/IEEE/ISA requirements and owner cybersecurity standards |

Utilities, water, oil and gas, mining and transport. |

Comply with approved vendor lists, protocol profiles, redundancy and documentation templates. |

5.1 Cybersecurity is becoming a market-access capability

The EU CRA is especially important for connected controllers and associated software. Reporting obligations begin on 11 September 2026, while the main product obligations apply from 11 December 2027. Suppliers should not wait for the final deadline. Product architecture, vulnerability intake, incident reporting, update signing, support-period commitments and software component records require organizational changes that cannot be added at the end of a certification project.

In the United States, NIST SP 800-82 Rev. 3 remains a key OT security reference. It emphasizes security controls that account for operational availability, safety and real-time requirements. Controller suppliers should support asset inventory, least privilege, network segmentation, logging, secure remote access, backup/restore, patch governance and incident response without undermining process reliability.

5.2 Localization requirements are broader than local manufacturing

- Local engineering: response times, commissioning and troubleshooting capability.

- Local documentation: manuals, safety information, cybersecurity notices and training in the required language.

- Local commercial capability: tender registration, tax, customs, warranty authority and approved-vendor processes.

- Local lifecycle capability: spares, firmware control, repair, vulnerability notification and end-of-life management.

- Local value contribution: configuration, panel integration, assembly, testing or supplier-development evidence where procurement systems reward local content.

6. Risk Analysis

|

Risk |

Severity |

Trigger |

Commercial effect |

Mitigation |

|

Certification mismatch |

High |

Product marketed before applicable safety/EMC/cyber requirements are mapped. |

Certification delays, customs or customer rejection. |

Create a country-product compliance matrix before quotations. |

|

Cybersecurity lifecycle gap |

High |

No SBOM, signed update, vulnerability process or supported-lifetime policy. |

Loss of EU projects and critical-infrastructure buyers. |

Implement IEC 62443-aligned secure development and incident workflows. |

|

Installed-base incompatibility |

High |

Missing protocols, libraries or migration tools. |

OEM/end-user rejection despite lower price. |

Test against target architectures and publish validated compatibility. |

|

Channel underinvestment |

Medium-high |

Distributor sells hardware but cannot engineer applications. |

Price competition and weak references. |

Certify application engineers and protect registered projects. |

|

Spare-parts and obsolescence |

High |

Long lead times or uncontrolled component substitutions. |

Downtime claims and brand damage. |

Regional stock, PCN/EOL process and form-fit-function continuity. |

|

Payment and FX |

Medium-high |

EPC or distributor credit exposure in volatile markets. |

Margin loss and overdue receivables. |

Milestones, credit insurance, FX clauses and credit limits. |

|

Export controls and sanctions |

Medium-high |

Controllers, encryption or end users trigger restrictions. |

Legal exposure and shipment blocks. |

Screen products, destinations, owners and end use before contracting. |

|

IP and source-code leakage |

Medium |

Excessive customization or unmanaged local copying. |

Loss of differentiation. |

Modular licensing, access control, contracts and secure build systems. |

|

Product liability / safety |

High |

Controller failure contributes to machinery or process incident. |

Claims, recalls and exclusion from OEM programs. |

Document intended use, safety limits, validation and insurance. |

|

Overexpansion |

Medium |

Too many countries and product families launched at once. |

Support failure and inventory fragmentation. |

Scale by vertical and reference base, not by distributor count. |

7. Three-Year Market Entry Roadmap

|

Period |

Strategic objective |

Actions |

Decision gates |

|

0–6 months |

Portfolio and compliance readiness |

Define product scope; select India/ASEAN plus one mature-market niche; map standards; complete protocol and cybersecurity gap assessment. |

Country-product compliance matrix; target OEM list; product support policy; localized sales kit. |

|

6–12 months |

Reference acquisition |

Recruit technical partners; provide demo kits; execute pilot machines or retrofit cells; certify key products. |

5–10 reference projects; trained application partners; measured support response. |

|

Year 2 |

Local service and repeatability |

Open regional spares and application support; formalize warranty and patch process; create vertical libraries. |

Repeat OEM orders; lower commissioning time; service revenue; documented installed base. |

|

Year 3 |

Scale and localization |

Add configuration/assembly where justified; enter EPC frameworks; expand certified safety/motion or edge platform. |

Multi-country channels, project contracts, lifecycle SLAs and stronger localization score. |

Priority Market and Product Combinations

|

Market |

Priority offer |

Target applications |

Recommended route |

|

India |

Compact/modular PLC + motion + distributed I/O |

Packaging, plastics, food, material handling, electronics and renewable-energy manufacturing. |

OEM design-in with local application engineering. |

|

Vietnam / Thailand / Malaysia |

Machine controller + I/O + gateways + edge connectivity |

Electronics, automotive, food, logistics and export manufacturing. |

Country distributors supported by a regional technical hub. |

|

Saudi Arabia / UAE |

RTU/process controller + redundant I/O + remote diagnostics |

Water, oil and gas, mining, logistics, utilities and new industrial zones. |

EPC/panel-builder partnership plus local service/local-content plan. |

|

United States |

Certified PLC/PAC + migration + secure edge control |

Food, packaging, logistics, specialty machinery and brownfield modernization. |

OEM/integrator design-in with UL/CSA certification and local stock. |

|

Germany / Italy / Spain |

Motion/safety, secure controller platform and retrofit engineering |

Machine tools, packaging, material handling, automotive suppliers and energy efficiency. |

Machine-builder partnerships with EU compliance and cybersecurity documentation. |

|

Mexico / Brazil |

Compact PLC + remote I/O + retrofit and training |

Automotive suppliers, food, packaging, mining, pulp and water. |

Local integrator/distributor and Spanish/Portuguese support. |

Conclusion

Industrial controller market entry is no longer a simple export exercise. Hardware is only the starting point. The winning proposition combines a reliable controller architecture with open communications, secure development, certification, migration tools, local application engineering, spare-parts continuity and a transparent lifecycle policy.

India and Southeast Asia should be the first broad growth markets for suppliers seeking OEM volume and new manufacturing capacity. The Middle East should be approached through EPC, panel-builder and infrastructure projects. North America and Europe are attractive for higher-value, certified and secure platforms, but they require a stronger compliance and service foundation. Latin America, Africa and Central Asia offer selective opportunities where rugged products, remote support and project partnerships solve real infrastructure and industrial problems.

The central strategic choice is therefore not whether to export a PLC. It is whether the supplier can become a trusted automation partner for a defined machine, plant or infrastructure application. Companies that build that capability can move from one-time hardware sales to repeat OEM business, project participation and lifecycle service revenue.