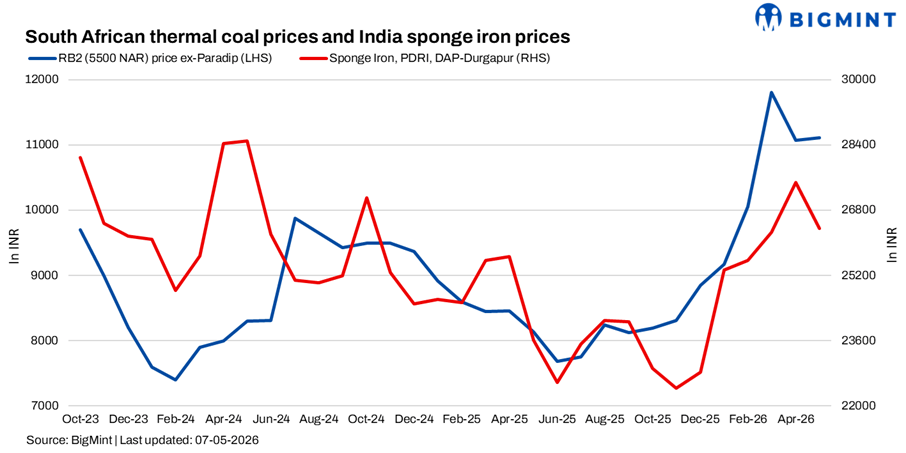

en.Wedoany.com Reported - As of May 7, 2026, price trends for South African thermal coal at Indian ports were mixed. Sponge iron prices fell by up to INR 1,000/ton week-on-week, while coal inventories at major ports climbed nearly 4%, extending the cautious market sentiment.

According to BigMint assessments, RB2 5500 NAR prices at Paradip and Visakhapatnam ports edged up by INR 50/ton to around INR 11,050/ton, while RB3 4800 NAR prices fell back by INR 50–100/ton to INR 9,650–9,700/ton. In April, India imported 1.97 million tons of non-coking coal from South Africa, a sharp 43.4% drop from 3.48 million tons in March, clearly reflecting weak industrial demand and the substitution effect of domestic coal.

Rising natural gas and crude oil prices drove international coal prices higher, leading to increased offers for South African thermal coal. The Indonesian HBA benchmark and climbing sea freight costs jointly pushed up landed costs. RB2 offers briefly rose to INR 11,300/ton but quickly corrected to around INR 11,000/ton due to insufficient buyer acceptance. Although some arriving cargoes were quoted at higher prices, inquiries were few. Downstream demand remained sluggish, and ample supply of cheap domestic coal left buyers unable to absorb high-priced shipments. In Mangalore, a user purchased approximately 2,000 tons of high-quality RB3 with 50% fixed carbon this week at an ex-works price of about INR 9,500/ton, whereas similar cargoes had traded at nearly INR 10,000/ton a few weeks prior. Local RB2 supply remained relatively scarce.

Weak demand in the sponge iron and steel sectors continued to pressure imported coal. DAP-Durgapur PDRI prices fell by INR 900/ton week-on-week to INR 25,750/ton, with market inquiries remaining cold and transactions limited. Users largely maintained hand-to-mouth purchasing, staying on the sidelines amid weakening steel prices and sluggish consumption of finished steel products. Trading in both semi-finished and finished steel was subdued, curbing raw material consumption. Traders reported that even when sellers lowered offer prices to stimulate inquiries, overall participation remained low, and the bid-offer spread continued to widen.

The cost advantage of domestic coal is prominent, especially for sponge iron producers facing narrowing margins, leading to a preference for domestic resources. In Week 18, non-coking coal inventories at major Indian ports increased by 3.7% week-on-week to 15.14 million tons, up from 14.60 million tons the previous week. Continuous inflow of cargoes at ports coupled with slow dispatch further reduced new import demand due to high stock levels.

In the short term, firm freight rates, strong international signals, and rising energy costs will likely keep offers for South African thermal coal elevated. However, the weak sponge iron market, ample port inventories, and the availability of low-priced domestic coal are expected to suppress procurement appetite.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com