en.Wedoany.com Reported - Shanghai Metals Market Information Technology Co., Ltd. (SMM) released its global nickel industry chain outlook at the 2026 Indonesia Mining Conference & Critical Metals Meeting - Nickel Cobalt Forum. SMM's Nickel Cobalt Lithium Industry Research Director, Feng Disheng, stated that SMM expects a supply deficit in the global primary nickel market in 2026, a continued surplus in 2027, and a potential shift to a tight balance by 2029. Regarding refined nickel prices, the global sulfur supply faces a sustained shortage over the next 2 to 3 years. Short-term Strait blockades keep sulfur prices high, strengthening cost support for the sulfur-MHP-refined nickel chain. On the macro front, the US-Israel-Iran conflict pushes up energy prices and inflation expectations, increasing short-term volatility in global commodity prices. Long-term geopolitical uncertainty may become the new normal, amplifying refined nickel price fluctuations.

Regarding the upstream Indonesian nickel ore sector, SMM analysis indicates that the Indonesian Ministry of Energy and Mineral Resources (ESDM) has denied rumors of a blanket 25% to 30% increase in RKAB production quotas. The government will strictly review supplementary quotas on a case-by-case basis starting from the second half of 2026, making orderly optimizations to the current ceiling of 260 to 270 million wet metric tons. As of April, Indonesia had approved cumulative RKAB quotas of 240 million wet metric tons, with mid-year supplementary quotas expected to be around 15%. The tight supply of domestic nickel ore will accelerate supplementary imports from the Philippines. It is estimated that Indonesia's nickel ore imports from the Philippines will rise from approximately 15 million tons in 2025 to 22 million tons this year. On the demand side, affected by tight sulfur supply, MHP output is falling short of expectations. SMM estimates that Indonesia's total nickel ore demand for 2026 will be revised down to 303 million wet metric tons.

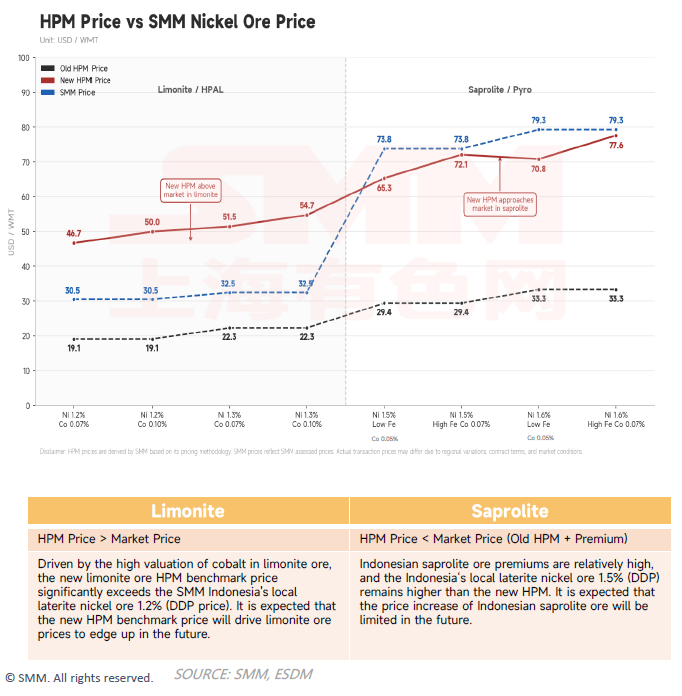

SMM also introduced adjustments to the Indonesian Nickel Ore Benchmark Price (HPM), incorporating pricing for associated elements such as cobalt, iron, and chromium into the benchmark to make it more reflective of actual transaction prices. Due to resource depletion, the grade of pyrometallurgical ore is structurally declining, leading to significantly higher medium-to-long-term prices. Hydrometallurgical ore prices also have upward momentum, influenced by stricter RKAB quota controls and the expansion of domestic MHP capacity. Overall, this will fundamentally raise raw material costs across Indonesia's entire nickel industry chain.

Regarding the Philippines, SMM expects a slight increase in Philippine nickel ore exports in 2026, with a particularly notable increase in exports to Indonesia. However, constrained by operational pressures and financial conditions, capacity expansion at major Philippine mines is essentially stalled in 2026. Periodic rainy seasons and fuel costs driven up by geopolitical conflicts further limit capacity release.

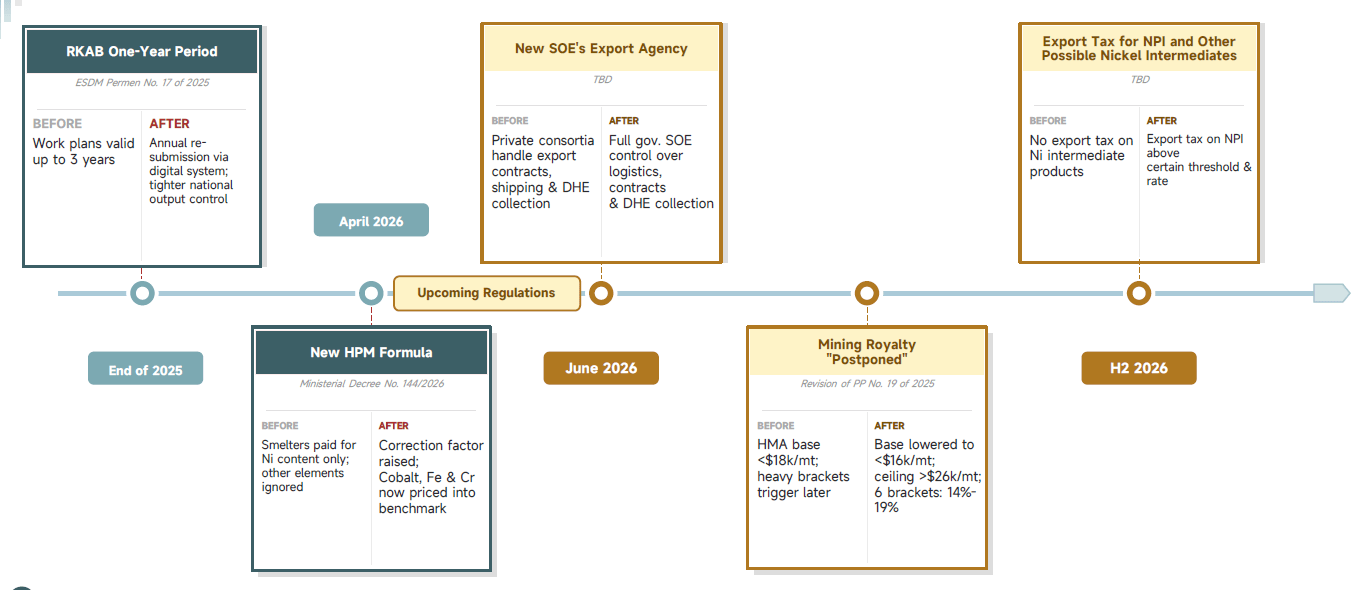

Starting from the fourth quarter of 2025, Indonesia implemented a series of new policies imposing comprehensive and strict controls across the entire nickel industry chain. This has narrowed profit margins for industry players, increased the number of approval and compliance procedures, and heightened administrative and operational resistance.

In the intermediate processing stage, Indonesia's MHP capacity continues to expand. SMM estimates that from 2026 to 2030, Indonesia's MHP capacity will grow at a compound annual growth rate (CAGR) of 21.7%, with output growing at a CAGR of 25.7%. Regarding the key auxiliary material sulfur, SMM's sulfur (CIF Indonesia) price has risen over 300% since March 2025. Scenario simulations for the Strait of Hormuz indicate that if shipping lanes are partially restored, prices are expected to fall back to $800-$900 per ton. If the blockade continues into the third quarter, prices are projected to rise to $1,300-$1,400 per ton.

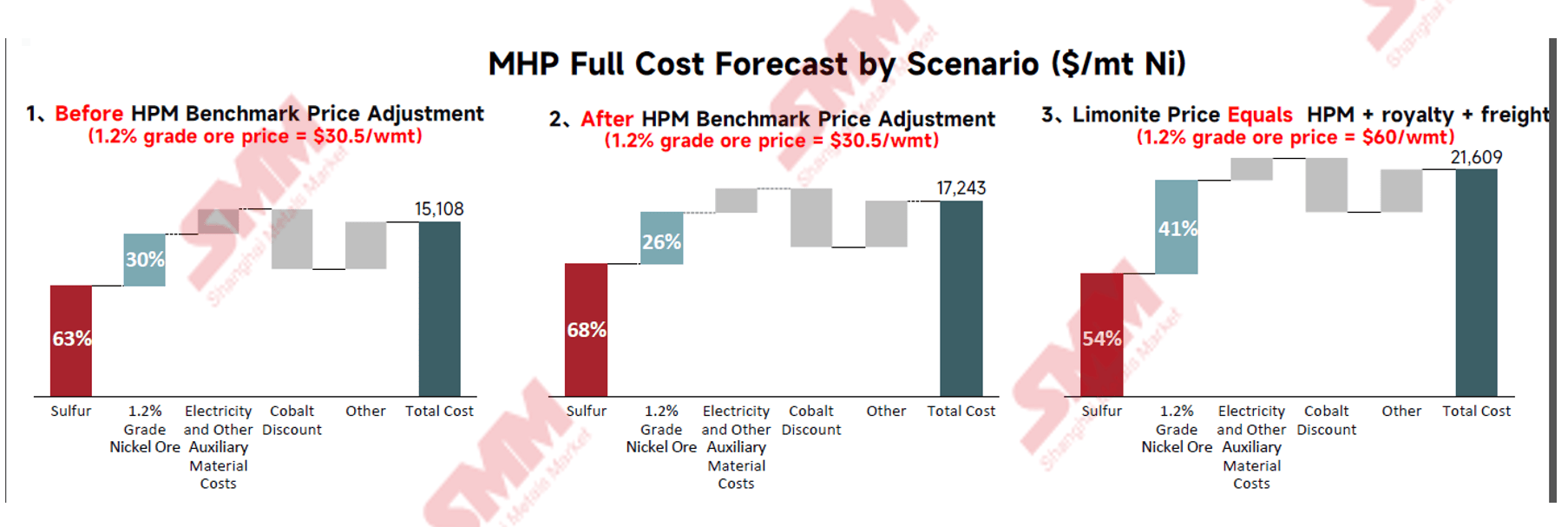

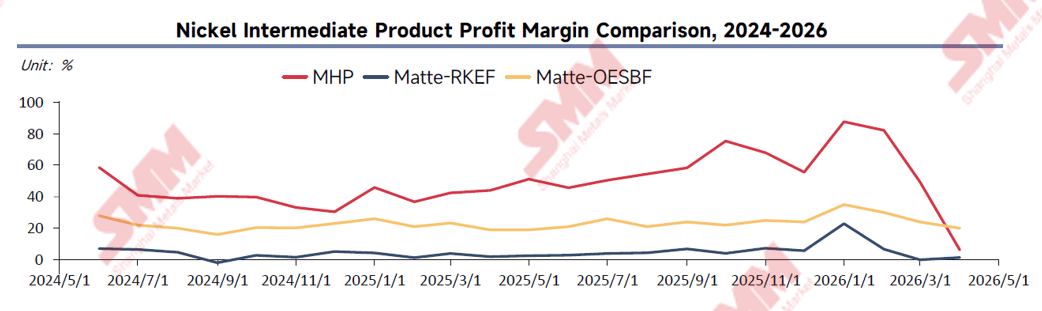

Concerning MHP production costs, SMM points out that while cost support from nickel ore for MHP production has not yet significantly increased, MHP production costs still face significant upward pressure due to high sulfur prices. In terms of profitability, the HPAL process has long maintained a profit margin exceeding 40%, but due to the surge in sulfur prices, it plummeted in the first quarter of 2026, falling below that of high-grade nickel matte. The profit margin for high-grade nickel matte produced via the RKEF process stagnated between 0% and 5%. In contrast, the OESBF process, utilizing autothermal reactions and compatibility with low-grade ore, maintains a stable profit margin of 15% to 30%. Overall, given the high short-term supply uncertainty and declining profit margins for MHP, high-grade nickel matte is expected to remain more economical in the third quarter. However, in the long term, MHP's outlook remains relatively certain.

For downstream nickel products, SMM's outlook for the nickel sulfate supply-demand balance from 2026 to 2030 predicts a supply shortage in 2026, with a tight balance persisting from 2027 to 2030. Regarding nickel pig iron (NPI), Indonesia's nickel ore mining is entering a depletion phase, with a reduction in high-grade saprolite ore. The average furnace feed grade is expected to potentially decline by 0.3 percentage points by 2030, accelerating the blending of low-grade ores. This will shift 8% to 10% NPI from marginal capacity to mainstream production, structurally raising the cost curve. The tight supply of high-grade NPI may peak around 2027, subsequently easing due to increased availability of substitutes like scrap, refined nickel, and ferronickel. Starting from 2026, price differentiation between different NPI grades has been formally established, with products containing 14% or more nickel commanding a clear premium over lower-grade products.

SMM calculations show that the profit per megawatt-hour for aluminum smelting is 36 times that of NPI. Given this profit disparity, even if only 15% of NPI capacity were to shift to the aluminum industry, it would directly tighten NPI supply by 5%. In the short term, NPI prices find bottom support, increasing procurement pressure for Chinese steel mills. In the long term, the pace of capacity transfer is expected to moderate.

On the demand side, SMM expects global lithium-ion battery production to grow at a CAGR of 18% from 2026 to 2030, with the market share of lithium iron phosphate (LFP) batteries potentially rising to 82% by 2030. Although LFP's market share will increase further in the short term, the total volume of the ternary battery market will continue to grow in the long term with the commercialization of solid-state batteries. In the stainless steel sector, SMM expects downstream demand to grow slowly at a CAGR of 2.8% from 2025 to 2030, with manufacturing replacing real estate as the primary driver. Overseas stainless steel demand is also expected to grow steadily from 2026 to 2030.

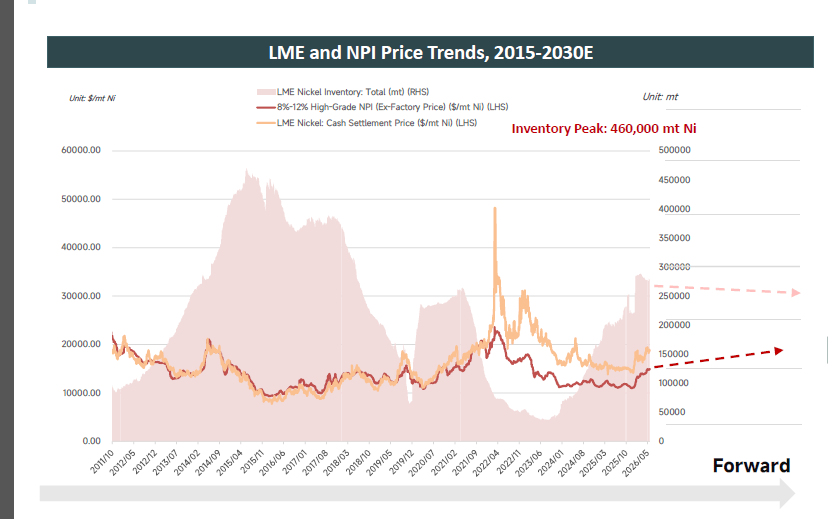

SMM expects a supply deficit in the global primary nickel market in 2026, a slight surplus in 2027, and a potential shift to a tight balance by 2029. In the long term, the global primary nickel market is expected to remain in a tight balance. Regarding refined nickel prices, global refined nickel inventories remain high, totaling 497,000 tons by the end of May, making significant demand growth difficult. On the cost side, sulfur shortages, rising NPI prices, HPM revisions, and declining nickel ore grades collectively raise the price floor. Macroeconomic and geopolitical factors increase price volatility.

As a globally leading third-party independent price reporting agency, SMM will continue to provide accurate price benchmarks, timely market news, comprehensive data coverage, and in-depth industry research reports.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com