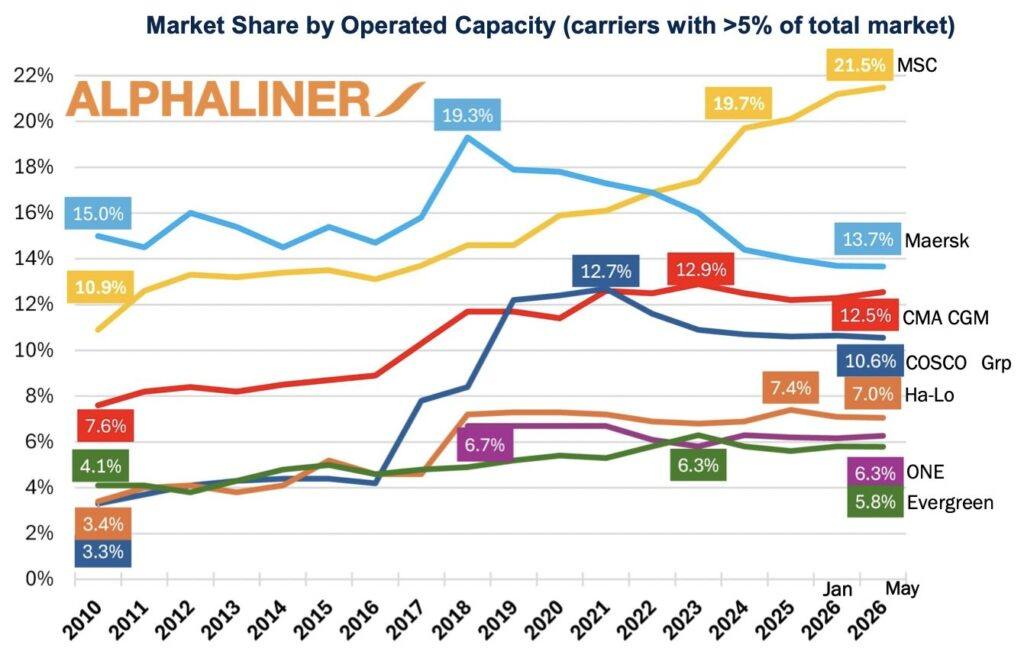

en.Wedoany.com Reported - Mediterranean Shipping Company (MSC) set a historical record for a single container liner company in May with a 21.5% share of global capacity. According to Alphaliner data, as of June 9, MSC's fleet had expanded to 7.329 million TEU, with its share rising to 21.6%.

The previous industry benchmark was the 19.3% share achieved by Maersk in 2018, when the Danish carrier set a record through aggressive integration. MSC has now surpassed that figure by more than two percentage points, having doubled its market share since 2010.

The Swiss shipping company has grown from a strong industry runner-up to a structurally dominant market leader, underpinned by a strategy that peers have not emulated: while competitors debated capital discipline, MSC has converted pandemic-era cash into hard assets at an unprecedented scale and speed since August 2020. As of November 2025, Splash statistics show it has cumulatively purchased 461 second-hand vessels. In 2025 alone, newbuilding deliveries are scheduled to include 54 ships totaling 695,185 TEU, with total capacity additions for the year reaching 831,400 TEU, representing an annual fleet growth rate of 11.7%, compared to a combined growth rate of just 7.3% for the top 12 carriers.

Fleet accumulation is a means, not an end. When MSC and Maersk announced the dissolution of the 2M alliance in January 2023 (with the exit date set for February 2025), MSC used the intervening two years to prepare for post-alliance operations. Its independent east-west network was unveiled in September 2024 and launched in February of the following year, offering 34 loops across five trade routes, including both Suez and Cape of Good Hope services. A slot exchange agreement with the Premier Alliance on Asia-Europe trade provides it with collaborative scope without reliance on others. MSC itself assesses that it "has the fleet size and strength required to operate as a non-alliance carrier."

The vertical dimension of MSC's expansion is equally deliberate. In 2019, it increased its stake in terminal operator TiL to 60%; in 2021, it acquired Brazil's Log-In Logistica; in 2022, it completed the €5.7 billion acquisition of Bolloré Africa Logistics (later renamed AGL); and in 2024, it obtained a minority stake in Hamburg's HHLA. The combined effect is that MSC's influence extends from terminals to inland logistics networks in Europe, Latin America, and Africa, strengthening its control over cargo flows at both ends of the supply chain.

Competitors have adopted markedly different strategies. Maersk has deepened its integrated logistics model and established the Gemini Cooperation with Hapag-Lloyd, prioritizing reliability over capacity growth.

Industry concentration is not limited to MSC. In January 2021, the top ten container carriers collectively held 84.8% of global capacity, a historical high. According to Alphaliner data, over the five months from last December to this April, these carriers took delivery of nearly 500,000 TEU of newbuilding tonnage, bringing their combined share to 84.7% of the total market by the end of May, just 0.1 percentage points below the historical record.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com