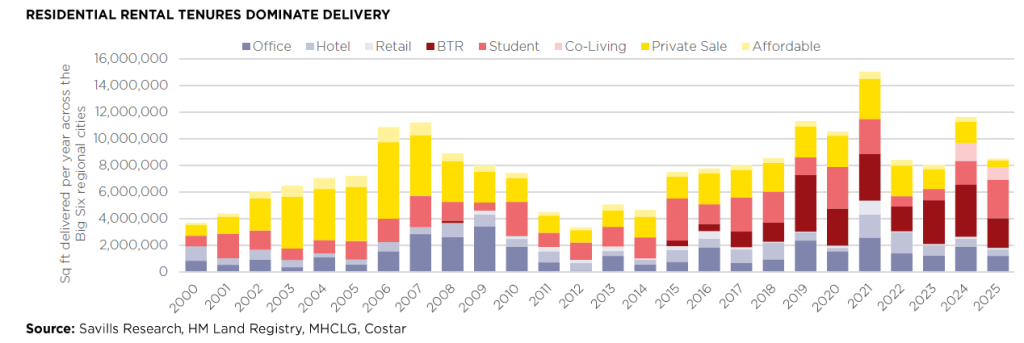

en.Wedoany.com Reported - A recent report released by Savills indicates that the development model in the city centers of the UK's six major regional cities is shifting from being dominated by private for-sale residential properties before the global financial crisis to more integrated mixed-use development. Build to Rent (BTR) has surpassed private sales to become the primary driver of residential delivery, while new asset classes such as Purpose-Built Student Accommodation (PBSA) and co-living are also expanding rapidly.

The study, titled "UK Cities: a mixed-use perspective," shows that over the past five years, annual rent growth in the six major cities—Birmingham, Bristol, Edinburgh, Glasgow, Leeds, and Manchester—has averaged between 4% and 7.5%, reflecting strong demand fundamentals. The increasing involvement of institutional capital supports large-scale, placemaking-led urban regeneration. However, sustained construction cost increases and growing affordability pressures require a pragmatic approach from developers and local planning authorities to maintain development viability.

The report emphasizes that the office market is undergoing a major structural transformation. In the post-pandemic era, hybrid working models have led to rising vacancy rates for older, inefficient buildings, but tenant demand is increasingly concentrated on modern, highly sustainable office spaces located in central areas with good transport links. Over 60% of office take-up in 2026 is expected to be for Grade A and prime quality. Meanwhile, the office development pipeline is exceptionally thin, with only Manchester and Leeds currently having projects under construction planned for completion after 2026. Over the past five years, prime office rents have risen by an average of 30%, and if this trend continues, they may soon approach the redevelopment viability threshold of £60 per square foot.

The retail sector is also evolving, shifting from traditional formats to experience, leisure, and F&B-focused mixed-use environments. The activation of ground-floor commercial spaces, including shops, bars, restaurants, and cafes, is increasingly becoming a key element connecting residential, office, and hotel uses, helping to attract target tenants and residents and maximize value across the project.

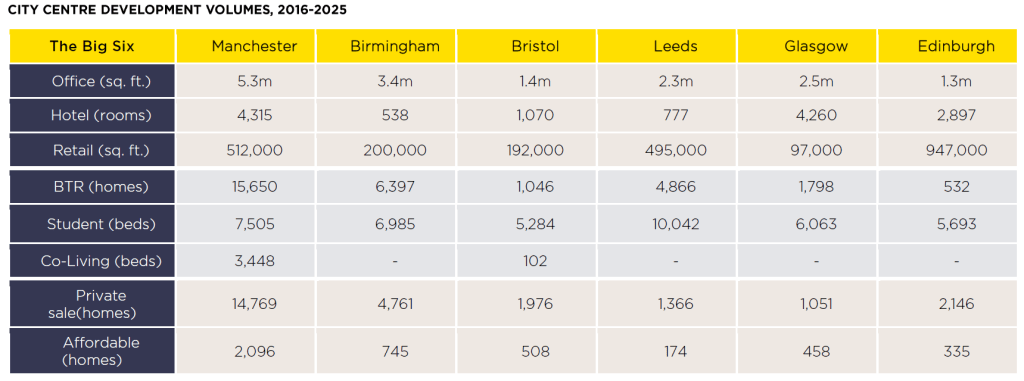

The study also showcases the scale and diversity of delivery in major cities between 2016 and 2025. Manchester delivered 5.3 million square feet of office space, 15,650 BTR homes, and 3,448 co-living beds; Birmingham delivered 3.4 million square feet of office space, 6,397 BTR homes, and 6,985 student beds; Leeds delivered 10,042 student beds; and Edinburgh delivered 947,000 square feet of retail space.

Emily Williams, Director of Residential Research at Savills, stated that residential development is expected to remain the core of city center regeneration, particularly through rental-led models, but rent growth may slow due to affordability caps. High construction costs, borrowing costs, and regulatory pressures are expected to continue constraining new supply, widening the gap between demand and delivery.

Jonathan Lambert, Co-Head of the Mixed-Use Sector Group at Savills, added that market polarization is a defining theme, with larger, more established cities better positioned to sustain development, while smaller or more constrained markets may struggle in a high-cost, high-risk environment. Local authorities need to take a pragmatic approach to viability issues, and public-private partnerships along with long-term patient institutional capital may be key to unlocking future opportunities.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com