en.Wedoany.com Reported - Vox Royalty Corp. (hereinafter referred to as Vox) achieved record results in the first quarter of 2026, with royalty and precious metal net revenue reaching $16.0 million, a significant increase from $2.7 million in the same period of 2025. Net income was $24.5 million, or $0.36 per share, including a non-cash gain of $16.5 million related to the revaluation of its global gold portfolio. The company generated operating cash flow of $15.2 million and adjusted EBITDA of $12.7 million ($0.18 per share), both quarterly records. Management raised its full-year 2026 revenue guidance from the previous range of $28-32 million to $32-37 million and issued its first long-term guidance for 2030, projecting revenue of approximately $66 million, a target based solely on existing assets and explicitly excluding the impact of the Red Hill litigation outcome.

The company operates in the precious metals royalty and streaming sector, employing an asset-light business model that involves acquiring fixed percentage or net revenue interests in third-party mining projects without assuming direct operational, exploration, or capital expenditure risks. This sector has historically commanded higher valuations than operating miners, benefiting from high marginal profits, limited cost inflation risk, and option value associated with mine life extensions and exploration success. Gold prices have risen steadily over the past 18 months, breaking through $3,000 per ounce in March 2025 and exceeding $5,000 per ounce by January 2026. With 92% of Vox's first-quarter 2026 revenue derived from gold-linked assets, this market backdrop provides a tailwind for the company through direct price exposure via offtake stream structures and indirect incentives for underlying operators to expand capacity. The company's market capitalization as of June 1, 2026, was approximately $389 million, placing it among the smaller publicly listed royalty companies—a core tension explored in this report: the disconnect between a track record of organic growth and balance sheet discipline and a valuation management believes does not yet reflect this.

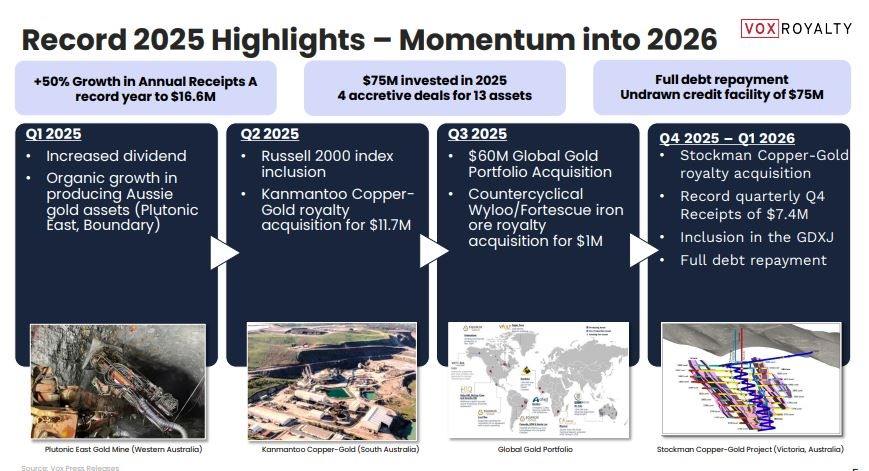

In the first quarter of 2026, Vox delivered 77,293 ounces of gold through its offtake stream structure, achieving an average net revenue margin of $179.41 per precious metal ounce. This mechanism allows the company to select purchase prices within multiple quotation windows and resell the metal at individually chosen price points, providing leveraged exposure to rising gold prices without assuming direct commodity price risk. The balance sheet remains unlevered: as of March 31, 2026, the company held $15.9 million in cash, had no outstanding debt, repaid $6.7 million in loan balances during the quarter, and maintained a fully undrawn $75 million revolving credit facility with the Bank of Montreal, providing total available capital of approximately $90 million.

In its investment materials, management highlighted the valuation gap between Vox's implied value per Gold Equivalent Ounce (GEO) and that of larger peers. The company disclosed that its royalty portfolio contains over 1 million GEOs, with an average royalty rate of approximately 1%, of which roughly 240,000 GEOs come from producing assets. Based on this, the implied market valuation is approximately $300 per GEO, compared to approximately $1,200 per GEO for Triple Flag Precious Metals and approximately $1,800 per GEO for Franco-Nevada. The company cites a 28% return on invested capital since inception as evidence of underwriting discipline comparable to or better than larger peers. However, these comparisons have some notable limitations: Franco-Nevada and Triple Flag are significantly larger, more diversified, have longer operating histories, and carry lower portfolio concentration risk, factors that typically command independent valuation premiums. The GEO comparison also does not adjust for differences in asset quality, jurisdictional risk, or the proportion of resource-stage ounces versus reserve-stage ounces.

Three assets are central to near-term catalyst discussions. Bonikro, an uncapped 50% gold stream in Côte d'Ivoire, saw its disclosed mine life extended from 4 years (to 2029) to 12 years (to 2036) following Allied Gold's updated production plan on June 10, 2026, with average annual production guidance exceeding 120,000 ounces, implying annual deliveries to Vox of approximately 60,000 ounces. Los Filos, a 50% gold stream nominally acquired for $1, is currently suspended pending a community agreement with Equinox Gold, representing an embedded option management estimates to be worth between $30 million and $50 million if production resumes. Red Hill, a 4.0% uncapped gross revenue royalty in Western Australia covering resources recently upgraded by approximately 58% to roughly 1.9 million ounces, benefits from a A$1.5 billion expansion of the underlying Fimiston processing plant. However, Northern Star Resources is contesting the transfer of the Red Hill royalty to Vox, a claim the company is defending as a second defendant in litigation, a risk explicitly excluded from formal guidance.

Vox has multiple fully cost-recovered royalty acquisitions in its capital allocation track record, including Kookynie at approximately 14x total cost, Graphmada at approximately 11x, and Segilola at approximately 5x. These figures support the company's strategy of identifying legacy assets through its proprietary database of 8,500 royalties. However, the same disclosures show that among broader acquisitions made between 2019 and 2024, total costs of $50 million had generated $45 million in total revenue as of 2025, yielding an overall portfolio ratio slightly below 1x invested capital. This does not necessarily indicate underperformance, as many positions remain in the early stages of their cash flow curves, and the company's 28% ROIC figure may employ a different calculation methodology or time period.

Vox enters the second half of 2026 with a significantly strengthened balance sheet, record quarterly operating metrics, and its first-ever long-term growth targets. If achieved, these targets would nearly double current revenue by 2030 without requiring further acquisitions. The core revaluation thesis rests on a valuation discount per GEO compared to larger peers, a discount directionally supported by data but constrained by differences in scale, diversification, and asset quality. Near-term shareholder value may depend more on the resolution of identifiable binary catalysts, including the Red Hill litigation outcome, the Los Filos community agreement, and the execution of mine life extensions such as Bonikro. Investors must weigh these catalysts against the company's structural reliance on third-party operator disclosures, concentration in the Australian jurisdiction (67% by asset count), and commodity price headwinds.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com