en.Wedoany.com Reported - The lithium market is undergoing a profound transformation, altering the development logic for mining projects. Vitor Bueckmann, an analyst at industry advisory firm Octave, outlined in a report several key trends that will shape industry competitiveness in the coming years, including digitalization, sustainability, infrastructure bottlenecks, and the application of new technologies.

Global demand for lithium continues to surge, driving a transformation that extends beyond mere production growth. With the acceleration of the energy transition and the consolidation of the electric vehicle market, the industry urgently needs to develop more efficient, sustainable, and technologically integrated operational systems to cope with an increasingly demanding market environment.

In his analysis, Bueckmann pointed out that the future of lithium mining depends on the ability to integrate technological innovation, operational efficiency, and environmental standards within a single strategic framework. Digitalization, process automation, and intelligent data integration have become indispensable means for maintaining the competitiveness of new projects.

Infrastructure is one of the key variables affecting industry growth. Beyond resource endowment, the feasibility of many projects will depend on whether power grids, roads, and logistics corridors can keep pace with expansion. In some scenarios, the strategic importance of such investments can rival the quality of the mineral deposit itself.

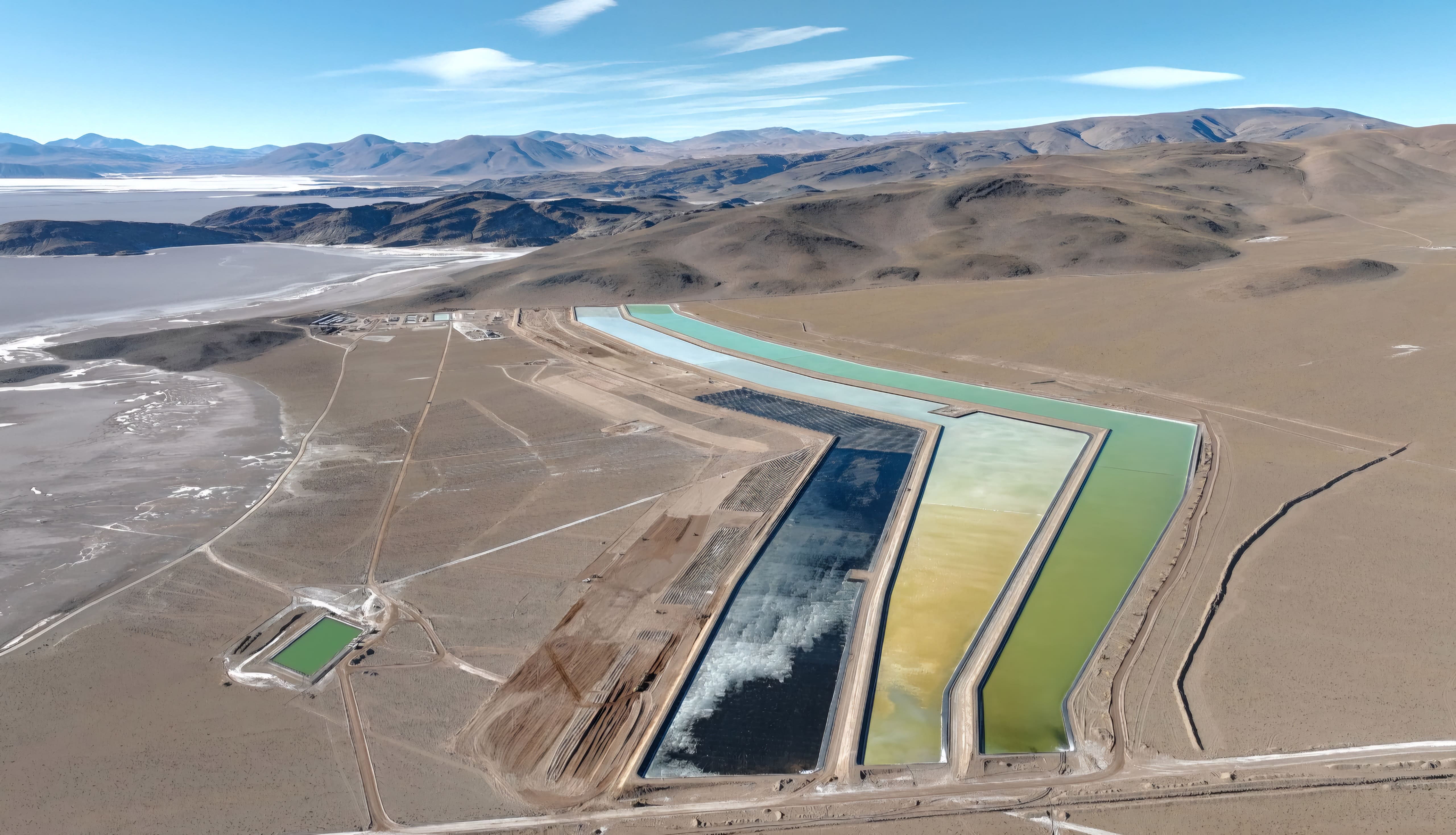

Chile in Latin America is a typical case. The Port of Antofagasta (Puerto de Antofagasta), leveraging its geological and logistical advantages, handles the majority of the country's lithium exports, but this also makes it a potential bottleneck for future development. Additionally, remote salt flats require substantial investment in power transmission and road construction as prerequisites for converting geological reserves into commercial operations.

The global market also reflects the scale of this challenge. According to data collected by Octave, approximately 200 new lithium mines will need to be built worldwide by 2040 to meet projected demand, corresponding to an estimated investment scale of between $400 billion and $600 billion (Brasil Mineral, 2025). This outlook presents both project opportunities and the imperative for the industry to accelerate the accumulation of technical, financial, and operational capabilities.

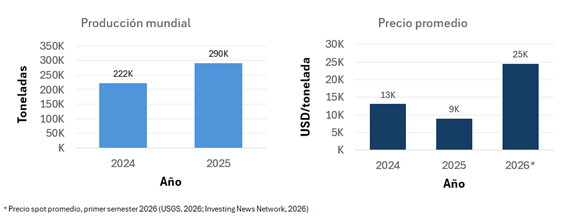

Recent market trends clearly reflect these dynamics: after a significant price decline in late 2025, lithium prices rebounded strongly in 2026, driven by robust demand from batteries and energy storage. Over the same period, global lithium production grew by more than 30%, indicating that the industry is not stagnating but rather in an expansion phase (USGS, 2026).

In this context, strategic cooperation between companies has become a key lever for advancing new projects. Bueckmann believes that the need for large-scale investment, the urgency of technology sharing, and the pursuit of economies of scale are driving the industry towards a high degree of consolidation through agreements among major international players.

The transformation also extends across the entire value chain. The industry is evolving from simple mineral extraction towards a higher value-added model encompassing processing, recycling, and vertical integration. The circular economy is gradually establishing itself as a strategic component, with existing recycling plants capable of recovering over 95% of lithium from spent batteries, and projections indicating that recycled sources could meet approximately 25% of global lithium demand by 2040 (Li-Cycle; Redwood Materials).

Sustainability has transcended regulatory compliance to become a competitive factor. Utilizing renewable energy in regions with high solar radiation, such as the Atacama Desert or the Puna Plateau, can reduce operational carbon footprints and improve a company's positioning in markets with increasingly stringent investor and environmental requirements.

Digitalization is also reshaping the industry's demand for talent. The ability to integrate data from multiple sources, apply predictive analytics tools, incorporate ESG indicators into operational management, and work in automated environments are becoming increasingly valued skills for mining companies.

Argentina is playing an increasingly important role in the global lithium landscape. With projects at various stages of development in the provinces of Salta, Jujuy, and Catamarca, the country is consolidating its position as a major supplier of strategic minerals and seeking to capitalize on the demand growth driven by the energy transition. The investment wave spurred by the Large Investment Incentive Regime (RIGI) is accelerating the development of new projects and the expansion of existing capacity. As of mid-2026, the regime had approved 18 projects with a total investment of $22.541 billion, covering multiple strategic sectors (La Nación, 2026).

In recent months, several lithium projects in Argentina have received investment approvals, involving capacity expansions, progress in RIGI processes, and the start of commercial operations. Specific examples include: Rio Tinto's Rincón project in Salta province, with a total investment of $2.5 billion plus $1.175 billion in financing, which began exports in March 2026; the Cauchari-Olaroz Phase II project in Jujuy province, a joint venture between Lithium Argentina and Ganfeng Lithium, with an undisclosed investment amount, which was in the RIGI approval stage in May 2026; Galan Lithium's Hombre Muerto Oeste project in Catamarca province, with an investment of $217 million, where Phase I construction is complete; and Posco's Sal de Oro Phase II project, spanning the provinces of Salta and Catamarca, with an investment of $547 million, which received RIGI approval in June 2026. These cases reflect Argentina's efforts to convert its project pipeline into actual export operations.

However, the expansion also carries warning signs: lithium's share of Argentina's exploration budget fell from 22% in 2021 to 11.3% in 2025, while during the same period, relative investment in lithium in Canada and Australia nearly tripled and increased, respectively (Secretaría de Minería de Argentina / S&P Capital IQ, 2026). This does not signify a global cooling of lithium exploration interest, but rather that capital is flowing towards jurisdictions with more predictable regulatory environments. This implies that regulatory stability and infrastructure will be as decisive as geological conditions in determining whether Argentina can maintain its industry leadership over the next decade.

The expansion also brings accompanying challenges, namely the need to support growth with infrastructure, logistics, and technology to transform resource potential into long-term competitiveness and sustainable operations. To this end, the full integration of the Capricorn Bioceanic Corridor (Corredor Bioceánico de Capricornio) is crucial in the short and medium term. This corridor will connect Argentina, Brazil, Chile, and Paraguay via a road and port network, providing direct access to the Pacific Ocean, which would benefit cargo transportation from Argentina's northwestern provinces (Ámbito, 2026).

From a strategic perspective, Bueckmann recommends that companies shift towards models based on integrated asset management, strengthen ESG strategies, form alliances to diversify risk, promote geographical diversification of operations, and treat recycling as a supplementary supply channel. This combination of measures can help companies maintain resilience in a market with higher technical, environmental, and financial demands.

The development of the lithium industry is no longer solely determined by geological potential. The ability to integrate technology, infrastructure, sustainability, and intelligent asset management will be the core variable determining which projects lead the next phase of growth in this industry, which sits at the pivotal point of the global energy transition.