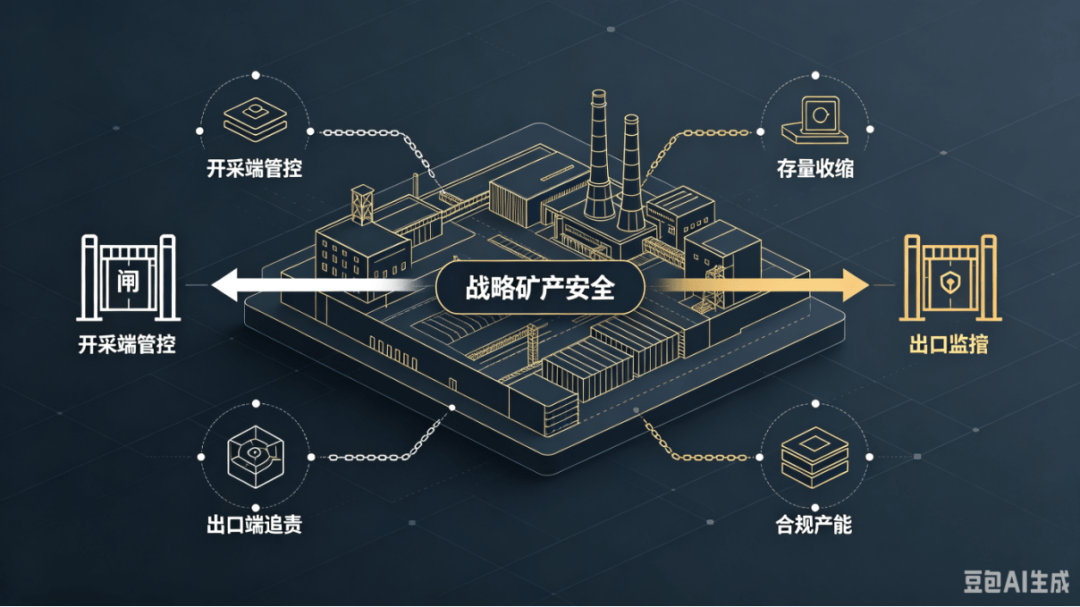

en.Wedoany.com Reported - China's Ministry of Commerce recently officially launched a reporting and supervision mechanism for strategic mineral export controls, aiming to crack down on smuggling and circumvention of export control violations across the entire supply chain. Meanwhile, two Japanese nationals were legally detained by Chinese authorities for attempting to smuggle rare earth magnets out of the country by concealing them inside ordinary motors. The mining industry views these two incidents as clear signals of China's tightening control over strategic mineral resources, driven not by short-term trade countermeasures or capital market speculation, but by a long-term institutional framework covering the entire chain from mining to export.

This tightening is reflected in both mining and export sectors. On the mining side, the new version of the "Implementation Regulations of the Mineral Resources Law" has included 36 types of critical minerals in the strategic catalog. New mining rights are essentially suspended, annual mining output quotas are rigidly enforced, and approval authority for mining rights has been fully centralized. Continuously rising environmental, safety, and energy consumption standards have accelerated the exit of small and inefficient mines, solidifying the existing industry structure. On the export side, the newly launched reporting and supervision mechanism covers ten types of violations, including unlicensed exports, splitting goods, and transshipment via third countries, with full-chain accountability involving freight forwarders, customs brokers, and technology transfer. This means that the operational space previously reliant on gray channels such as "repackaging and rerouting through other ports" has been significantly compressed.

The core of this control is not a complete supply cut-off, but to safeguard the bottom line of industrial security. Strategic minerals such as rare earths, tungsten, and molybdenum are core raw materials for military, semiconductor, and high-end equipment manufacturing, directly impacting the security of the industrial chain. Japanese companies deemed risky are included in the control list, while compliant companies can be removed from controls after passing inspections. The aim is to block gray channels of acquisition and prioritize the supply of raw materials for China's domestic high-end industries.

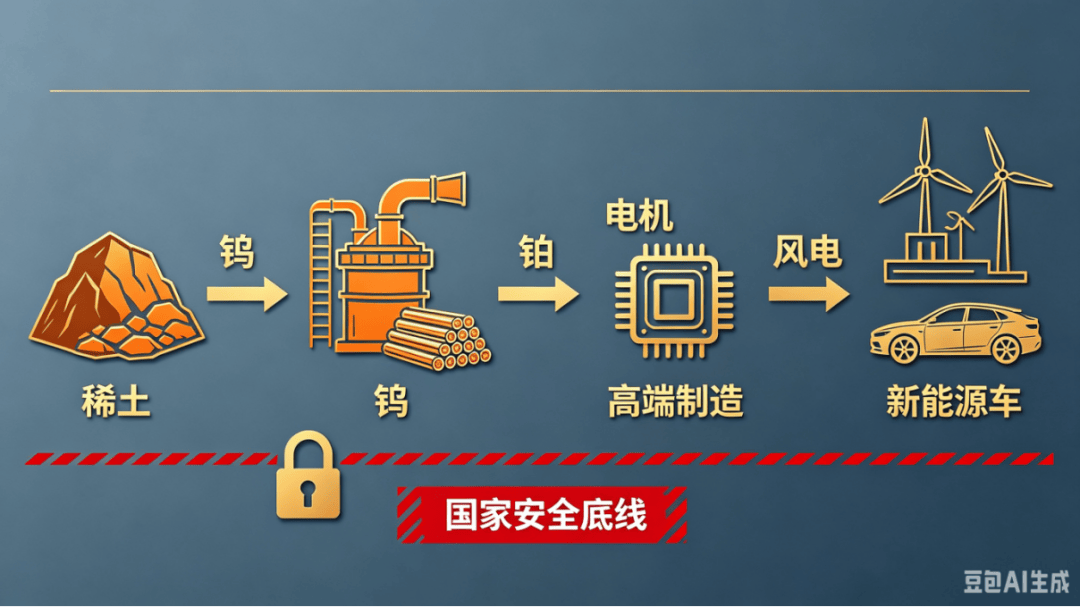

Looking at specific minerals, the trend of supply-demand mismatch is already evident. For rare earths, rigid mining quotas combined with blocked smuggling channels will continue to increase the tightness of medium and heavy rare earth supply. Downstream permanent magnet materials are deeply tied to sectors like new energy vehicles, humanoid robots, and wind power, providing stable demand support. Tungsten is a critical raw material for cemented carbide and semiconductor tungsten hexafluoride, with high dependence from overseas, especially Japanese and South Korean manufacturers. After the gray channel of exporting high-purity tungsten powder via Southeast Asia was blocked, compliant supply will remain tight. For molybdenum, beyond traditional steel applications, technological iterations of "replacing tungsten with molybdenum" in AI computing and memory chips are releasing new demand increments. With molybdenum under routine control, supply-side growth is limited.

For mining industry practitioners, this round of controls signifies a complete shift in the industry's development logic. Against the backdrop of essentially halted new mining rights, the scarcity of companies with compliant mines and stable mining quotas will become increasingly prominent. Enterprises with a full industrial chain layout covering "mining, smelting, and deep processing" will have stronger risk resistance and profit elasticity. At the same time, caution is needed regarding two types of targets: first, companies without their own mines that purely engage in toll processing, as the benefits of rising raw material prices are mostly absorbed by upstream players; second, companies that merely ride on the strategic resource hype without substantial compliant production capacity. Future core competitiveness will hinge on the depth of resource reserves, breakthroughs in deep processing technology, and expansion into high-end application scenarios.