en.Wedoany.com Reported - On the evening of July 8, China's Hunan Gold (002155) announced that it plans to acquire 100% equity of Hunan Gold Tianyue Mining Co., Ltd. ("Gold Tianyue") and 100% equity of Hunan Zhongnan Gold Smelting Co., Ltd. ("Zhongnan Smelting") through share issuance, with a total transaction value of 4.334 billion yuan. At the same time, it plans to raise up to 1 billion yuan in supporting funds by issuing shares to no more than 35 specific investors.

This transaction constitutes a major asset restructuring and related-party transaction, but does not constitute a backdoor listing. After the transaction is completed, the company's controlling shareholder will remain Hunan Gold Group, and the actual controller will remain the State-owned Assets Supervision and Administration Commission of Hunan Province, with no change in control.

The initial issuance price for the shares used to acquire the assets is 17.06 yuan per share, which is no less than 80% of the average trading price of the stock over the 120 trading days prior to the pricing benchmark date. Since the listed company implemented a cash dividend for 2025 on June 11, 2026, the issuance price has been adjusted to 16.76 yuan per share according to adjustment rules. Based on this calculation, the transaction plans to issue approximately 259 million shares to the counterparty, accounting for about 14.20% of the total share capital after issuance (excluding supporting funds raised).

The valuation of the target assets is a key highlight of this transaction. With March 31, 2026 as the valuation base date, the appraised value of 100% equity of Gold Tianyue is 3.502 billion yuan, representing a premium rate of 464.04% over its book value; the appraised value of 100% equity of Zhongnan Smelting is 832 million yuan, with a premium rate of 11.39%. The total transaction value for the two target assets is 4.334 billion yuan, all paid in shares with no cash consideration.

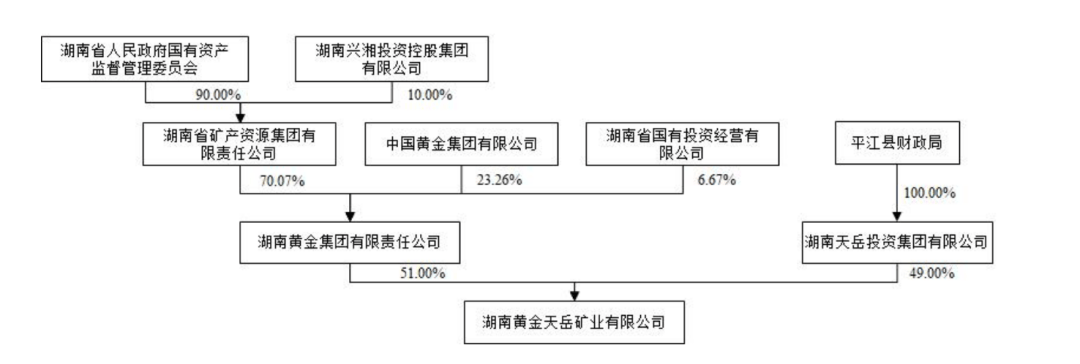

Gold Tianyue is the core target of this restructuring. The company is primarily engaged in the integration and exploration of mining rights in the Wangu mining area, as well as the mining, processing, and sale of some gold mines, with the main product being gold concentrate. The Wangu mining area currently has a large number of mining rights, previously divided between Gold Tianyue and Hunan Gold's subsidiary, Gold Dong Company, as two development entities. The interwoven distribution of mining rights has constrained large-scale mining. After the transaction is completed, Hunan Gold will achieve large-scale and intensive mining and processing of gold resources in the Wangu mining area in accordance with the requirements of "integrated exploration and integrated development." Zhongnan Smelting is primarily engaged in the specialized smelting and processing of refractory gold concentrates with high arsenic and high sulfur content. This acquisition will help Hunan Gold integrate the mining, processing, and smelting stages of gold resources and reduce related-party transactions.

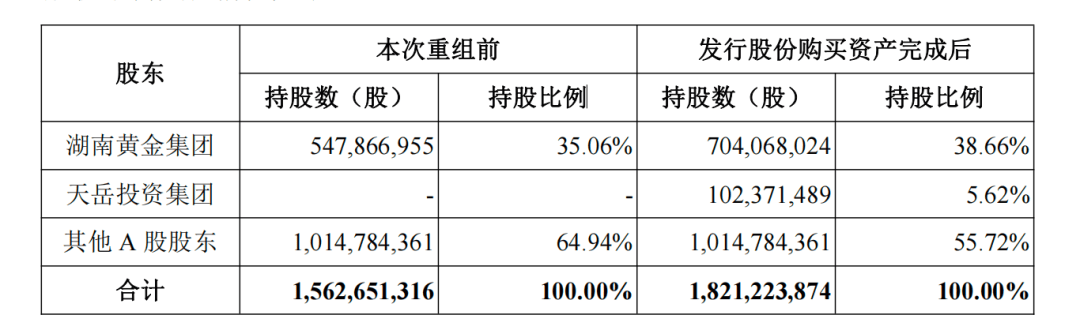

After the transaction is completed, Hunan Gold Group's shareholding ratio will increase from 35.06% to approximately 38.66%, Tianyue Investment Group will hold approximately 5.62% of shares, and the controlling shareholder and actual controller will remain unchanged.

Hunan Gold noted that most of the mining rights under Gold Tianyue are still in a state of undeveloped substance, and its performance has not yet been fully realized. Issuing shares to expand total share capital may expose the listed company to the risk of diluted immediate returns in the short term.

From a fundamental perspective, Hunan Gold is in a period of rapid performance growth. In 2025, the company achieved operating revenue of 50.181 billion yuan, a year-on-year increase of 80.26%; net profit attributable to the parent company was 1.488 billion yuan, a year-on-year increase of 75.77%, with both revenue and profit reaching historical highs, and an asset-liability ratio of only 13.47%. Entering 2026, the company achieved operating revenue of 18.831 billion yuan in the first quarter, a year-on-year increase of 43.51%; net profit attributable to the parent company was 596 million yuan, a year-on-year increase of 79.21%. The company stated that the performance growth was mainly due to the year-on-year increase in sales prices of gold and antimony products and an increase in product sales volume.

Hunan Gold has formed a "gold + antimony + tungsten" multi-metal synergistic development pattern. The gold business is the company's core pillar, and the antimony business holds a leading position in China. In 2025, the company's sales revenue from gold, antimony, and tungsten products all achieved significant growth, with the profitability of the antimony business notably improving. The company's subsidiaries, including Chenzhou Mining, Gold Dong Mining, and Xinlong Mining, constitute a stable mining and processing system.

In 2026, the gold market experienced significant volatility. At the beginning of the year, gold prices once hit a historical high of $5,405 per ounce, but subsequently fell sharply, declining by approximately 7% in the first half of the year. The tight supply-demand dynamics for rare and scattered metals such as antimony and tungsten supported an upward shift in the price center. Antimony, as an important raw material for flame retardants and photovoltaic glass clarifiers, continues to see growing demand in the new energy sector; tungsten is widely used in fields such as cemented carbide and special steel. As a leading enterprise in China's antimony industry, Hunan Gold is expected to continue benefiting from the favorable antimony price cycle.

Hunan Gold specifically noted that fluctuations in gold prices directly affect the company's profitability. If gold prices fall sharply in the future, the profitability of the target companies will be adversely affected. Additionally, most of the mining rights under Gold Tianyue are still in a state of undeveloped substance, and integration and subsequent production will require a certain period. Whether the integrated development of the Wangu mining area can proceed smoothly and whether performance commitments can be fulfilled on schedule are key variables determining the success of this restructuring. There remains uncertainty as to whether this transaction can successfully pass shareholder meetings and regulatory review.