1. Scope, Definitions and Methodology

1.1 Product Scope

A variable frequency drive controls the speed and torque of an AC motor by converting incoming AC power to DC and then synthesising a variable-frequency, variable-voltage AC output. The core low-voltage architecture normally includes an input rectifier, DC-link components, an inverter stage based on power semiconductors, gate drives, control electronics, sensors, firmware, thermal management and protection. The market spans simple V/Hz microdrives, sensorless-vector drives, closed-loop vector drives, process drives, HVAC drives, low-harmonic drives, regenerative drives and fully enclosed systems with disconnects, bypasses and line contactors.

The analysis concentrates on low-voltage drives below 1 kV because this is the range covered by most public distribution quotations and by the principal efficiency framework discussed in IEC 61800-9-2. Medium-voltage drives are project-engineered products with different semiconductor topologies, transformers, cooling systems, site testing and commercial terms; their prices cannot be inferred from low-voltage data.

1.2 Price Definitions Used in the Report

|

Price term |

What it normally includes |

What it normally excludes / risk |

|

Public web price |

One catalogued drive, standard configuration, distributor channel |

Tax, freight, project engineering, filters, enclosure, installation, commissioning and service |

|

Ex-works |

Equipment at the supplier factory |

Export packing, inland freight, customs, insurance, international freight and destination costs |

|

FOB |

Export-cleared equipment delivered on board at the named port |

Ocean freight, insurance, destination handling, duty, tax and inland delivery |

|

CIF |

Cost, insurance and freight to the named destination port |

Import duty, tax, customs brokerage, inland transport, installation and commissioning |

|

DDP |

Delivery to the named destination with most import formalities included |

Site installation, cabling, testing, process integration and operational risk unless stated |

|

Installed / turnkey |

Drive plus defined engineering, enclosure, accessories, installation and commissioning |

May still exclude civil work, upstream switchgear, motor replacement, production downtime or long-term service |

Table 1. Price-scope definitions for VFD procurement

1.3 Data Quality Rules

- PPI data are used only as a directional proxy for the U.S. industrial-control manufacturing environment. They are not presented as an exact global VFD selling-price series.

- Commodity data are annual nominal U.S. dollar benchmark prices. They show input-price pressure but cannot be converted directly into a finished-drive price without a verified bill of materials.

- Distributor quotations are dated snapshots. They may change without notice and are not representative of negotiated OEM, EPC or volume-purchase prices.

- The TCO model is an illustrative scenario, not an investment recommendation. Buyers should replace the assumptions with site duty-cycle, tariff, static-head, load and installed-cost data.

2. Price Trend: What the Public Data Actually Show

2.1 Industrial-Control Producer Prices Rose Sharply

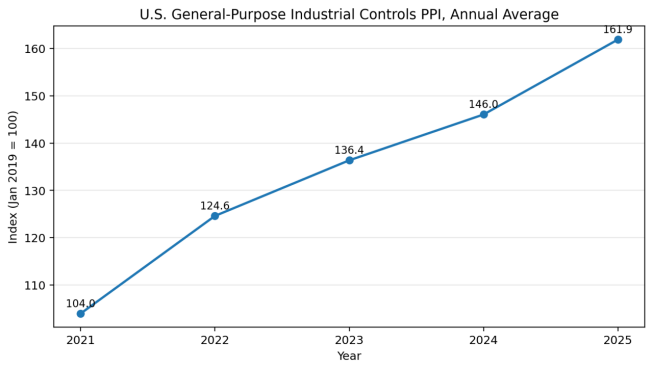

The U.S. Bureau of Labor Statistics series for general-purpose industrial controls rose markedly across 2021-2025. The annual average increased by 19.8% in 2022, 9.4% in 2023, 7.1% in 2024 and 10.8% in 2025. The cumulative increase from the 2021 annual average to 2025 was 55.7%. [1]

This series covers a broader group of industrial controls than VFDs, so it should not be interpreted as proof that every drive model increased by the same amount. It is nevertheless useful evidence that the manufacturing and channel environment remained inflationary even after acute semiconductor shortages eased. Standard drives are exposed to competition and product-platform cost reduction, while configured systems retain labour, engineering, compliance and channel content that is less responsive to commodity deflation.

Figure 1. U.S. general-purpose industrial controls producer-price trend

Source: U.S. Bureau of Labor Statistics via FRED, series PCU335314335314F. Annual averages calculated from monthly observations. This is an industrial-controls proxy, not a VFD-only index.

|

Year |

Annual average index |

Year-on-year change |

|

2021 |

104.0 |

- |

|

2022 |

124.6 |

19.8% |

|

2023 |

136.4 |

9.4% |

|

2024 |

146.0 |

7.1% |

|

2025 |

161.9 |

10.8% |

Table 2. Annual-average industrial-control PPI used as a price-direction proxy

2.2 Metals Were Mixed: Electronics and Value-Added Content Matter

VFDs contain copper in busbars, chokes, transformers and cabling; aluminium in heat sinks and enclosures; and steel in cabinets and structural parts. Yet the finished product is not a simple metal-cost pass-through. From 2021 to 2025, the IMF global benchmark price for copper increased from USD 9,317/t to USD 9,947/t, and aluminium increased from USD 2,473/t to USD 2,631/t. Iron ore declined from USD 158/t to USD 104/t.

The net effect varies by drive rating and design. Small drives have a higher share of control electronics, casing, assembly, firmware, certification and channel cost per kilowatt. Larger drives contain more power semiconductors, DC-link components, busbars, heat sinks, cooling and enclosure material. Enclosed bypass systems add contactors, protective devices, controls and labour that are not captured by the basic drive module price.

Figure 2. Selected global input commodity price trends

Source: International Monetary Fund Primary Commodity Prices via FRED. Annual nominal USD benchmark prices; indices calculated with 2021 = 100.

|

Year |

Copper (USD/t) |

Aluminium (USD/t) |

Iron ore (USD/t) |

|

2021 |

9,317 |

2,473 |

158.2 |

|

2022 |

8,829 |

2,707 |

120.7 |

|

2023 |

8,491 |

2,256 |

120.3 |

|

2024 |

9,142 |

2,421 |

111.1 |

|

2025 |

9,947 |

2,631 |

103.7 |

Table 3. Commodity data underlying Figure 2

2.3 Why Factory Prices and Delivered Prices Can Diverge

A supplier can reduce the factory price of a standard drive platform while the buyer still pays more at the project level. The most common reasons are a stronger supplier currency, higher destination freight, import duty, local certification, higher short-circuit ratings, harmonic mitigation, longer cable requirements, motor-side filters, cooling or derating, local panels, commissioning, extended warranty and spare-parts packages. Conversely, a higher-priced drive can reduce delivered lifecycle cost when it eliminates a separate filter, reduces cabinet size, supports the required communications protocol, shortens commissioning or avoids motor damage.

3. Current Public Price Benchmarks and Quotation Dispersion

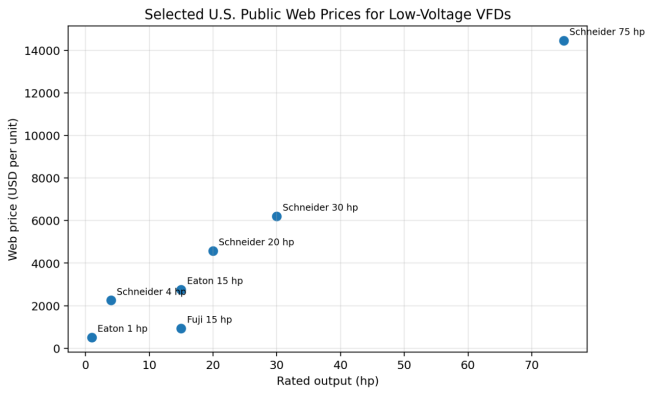

3.1 Public U.S. Web Prices: A Snapshot, Not a Global Price List

The following observations were collected from public Grainger product pages on 29 June 2026. They are one-unit web prices in the United States and should be treated as retail-channel snapshots. Taxes, freight, installation and project-specific accessories are not included. Specifications differ materially, so the table is intended to demonstrate quotation dispersion rather than rank suppliers.

|

Series |

Rating |

Voltage |

Selected scope |

Web price |

USD/hp |

|

Eaton DC1 |

1 hp |

480 V |

IP21, no bypass, general-purpose HVAC |

$507.62 |

$507.62 |

|

Schneider Altivar Process 600 |

4 hp |

480 V |

IP21, process/utilities, no bypass |

$2,249.14 |

$562.28 |

|

Fuji FRENIC-Mini C2 |

15 hp |

460 V |

IP20, compact, no Ethernet |

$936.92 |

$62.46 |

|

Eaton PowerXL DG1 |

15 hp |

480 V |

IP21, high-performance, Ethernet |

$2,751.07 |

$183.40 |

|

Schneider Altivar Process 600 |

20 hp |

480 V |

IP21, process/utilities, no bypass |

$4,573.98 |

$228.70 |

|

Schneider Altivar Process 600 |

30 hp |

480 V |

IP21, process drive, line contactor |

$6,198.17 |

$206.61 |

|

Schneider Altivar 900 |

75 hp |

480 V |

IP21, high-performance process drive |

$14,455.69 |

$192.74 |

Table 4. Selected public U.S. low-voltage VFD web prices, accessed 29 June 2026

Source: Grainger public product pages, item and manufacturer model numbers listed in the source notes. Prices are snapshots and can change without notice.

Figure 3. Public web-price dispersion across selected drive ratings

Note: Products differ in control capability, enclosure, process features, communications, contactor content and brand positioning. The chart must not be used as a same-specification comparison.

3.2 What the Quotes Reveal

First, price per horsepower generally falls as rating increases, but the pattern is interrupted by configuration and feature differences. The 4 hp Schneider process drive carried a much higher USD/hp value than the 15 hp compact Fuji unit. Second, two 15 hp products on the same platform differed by almost three times: the compact Fuji unit was USD 936.92, while the Eaton DG1 high-performance unit with Ethernet was USD 2,751.07. Third, the 30 hp and 75 hp process drives show how power scaling, contactors, enclosure and communications can keep total price high even when USD/hp is lower than on small units.

At the entry end of the market, AutomationDirect advertised its GS20 series as starting at USD 171, with ratings extending across several voltage and horsepower ranges. That starting price is useful only as evidence of a low-cost microdrive tier; it does not define the price of a fully specified industrial system.

3.3 Main Drivers of Quotation Dispersion

|

Driver |

Why it changes price |

Buyer verification |

|

Duty and overload rating |

Constant-torque and heavy-duty ratings require higher current capability than light-duty fan/pump ratings |

Compare continuous current, overload duration and ambient-temperature derating |

|

Enclosure and environment |

IP20 chassis units are cheaper than IP54/IP55, NEMA 12 or outdoor systems |

Confirm dust, moisture, corrosive gas, altitude and temperature conditions |

|

Harmonics and power quality |

Reactors, passive filters, active-front-end or low-harmonic topologies add hardware and engineering |

Specify THDi target, source impedance, short-circuit ratio and applicable standard |

|

Bypass and isolation |

Bypass contactors, disconnects, fuses and control logic increase cabinet size and labour |

Check whether bypass is manual, automatic or redundant and whether it preserves protection |

|

Safety and controls |

STO, safe brake control, encoder feedback, PLC functions and network protocols increase functionality |

Define safety integrity, protocol licences, I/O and cybersecurity requirements |

|

Motor and cable compatibility |

Long cables, old motors, high dv/dt and bearing-current risk may require filters or insulated bearings |

Check cable length, motor insulation, grounding and switching-frequency limits |

|

Service and warranty |

Local commissioning, spare units, extended warranty and response-time commitments are value-bearing scope |

Price service-level agreements separately and verify local inventory |

Table 5. Technical factors behind VFD price dispersion

4. Product-Specific Cost Structure

Public sources do not disclose a consistent global bill-of-material cost share for VFDs. Supplier designs, power ratings, purchasing scale, vertical integration and channel models differ too much to justify a universal percentage split. The following cost map is therefore qualitative and directional.

|

Cost block |

Typical content |

Relative cost importance |

Main volatility / differentiation |

|

Power conversion stage |

Rectifier, IGBT or MOSFET modules, gate drivers, current sensors |

High |

Semiconductor cycle, current rating, switching frequency, overload design and supplier qualification |

|

DC link and magnetics |

Electrolytic or film capacitors, chokes, reactors, busbars |

Medium to high |

Copper, aluminium, capacitor lifetime, harmonic design and temperature rating |

|

Control electronics |

MCU/DSP, PCB, I/O, communications, memory, cybersecurity functions |

Medium |

Chip availability, firmware development, protocol support and obsolescence management |

|

Thermal management |

Heat sinks, fans, liquid cooling on larger units, thermal sensors |

Medium |

Aluminium, acoustic limits, ambient temperature, altitude and maintenance requirements |

|

Mechanical and enclosure |

Housing, cabinet, coatings, seals, terminals, disconnects, contactors |

Low to high |

IP/NEMA class, corrosion category, bypass design, short-circuit rating and local panel labour |

|

Testing and compliance |

EMC, safety, efficiency mapping, type tests, documentation |

Medium |

Target markets, certification portfolio, product variants and audit costs |

|

Channel, warranty and service |

Distributor margin, technical support, commissioning, spares and warranty reserve |

Medium to high in mature markets |

Local availability, response time, installed base and contractual risk |

Table 6. Directional VFD cost architecture

4.1 Cost Behaviour by Product Tier

Microdrives and standard general-purpose drives are the most exposed to scale economics, platform reuse and price competition. Their cost reduction comes from integrated power modules, common control boards, simplified I/O, compact mechanical design, automated production and global sourcing. Because these products are easy to compare on headline rating, channel competition can be intense.

Process, safety and low-harmonic drives carry more software, sensor, communications, certification and application-engineering content. Their value is tied to uptime, process stability and compliance rather than only conversion hardware. Enclosed and bypass drives add protective devices, thermal design, wiring, panel engineering and testing. Medium-voltage drives are predominantly project-engineered systems; power-cell topology, transformer, cooling, redundancy, site acceptance testing and long-term service dominate the commercial package.

4.2 Semiconductor Direction

Conventional low-voltage VFDs remain predominantly silicon-based. Silicon-carbide devices can reduce losses and enable higher switching frequencies, but 2025 IEA 4E tests warned that excessive switching frequency can make drive losses dominate, while faster voltage rise can increase motor-insulation and bearing-current stress. Long-term testing also identified reliability issues. Buyers should evaluate wide-bandgap technology as a system architecture rather than a device-efficiency claim. [10]

5. Project Economics and Total Cost of Ownership

5.1 Energy Savings Depend on the Load Curve

For centrifugal fans and pumps with low static head, the affinity laws provide the most important economic mechanism: flow varies approximately with speed, pressure with the square of speed and power with the cube of speed. The U.S. Department of Energy states that reducing speed or flow by 20% can reduce input power by approximately 50% in appropriate variable-torque applications. [5]

This relationship does not apply unchanged to every application. Constant-torque loads such as conveyors, positive-displacement pumps, extruders and many compressors have a different power-speed relationship. High static head, minimum-flow constraints, process pressure, poor motor efficiency, low operating hours or an already efficient control method can reduce savings. Conversely, large throttling losses, long annual operating hours and high electricity prices can produce short payback periods.

5.2 Illustrative Payback Sensitivity

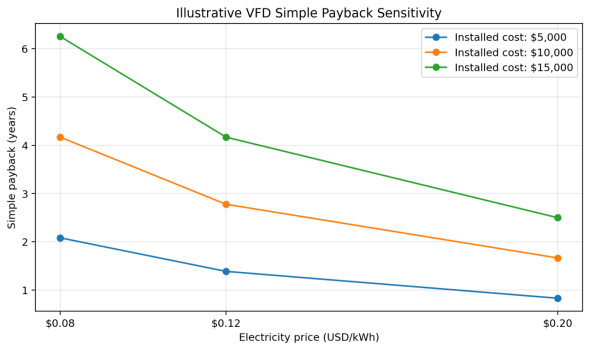

The following scenario assumes a 30 kW motor, 4,000 operating hours per year and net electricity savings of 25% after drive and motor losses. The avoided electricity is 30,000 kWh/year. These values are assumptions for sensitivity analysis and must be replaced with site measurements.

Figure 4. Illustrative simple payback under different electricity and installed-cost assumptions

Assumptions: 30 kW motor, 4,000 h/year, 25% net electricity reduction. Excludes financing, maintenance, demand charges, production benefits and residual value.

|

Installed cost |

Payback at $0.08/kWh |

Payback at $0.12/kWh |

Payback at $0.20/kWh |

|

$5,000 |

2.1 years |

1.4 years |

0.8 years |

|

$10,000 |

4.2 years |

2.8 years |

1.7 years |

|

$15,000 |

6.2 years |

4.2 years |

2.5 years |

Table 7. Payback values underlying Figure 4

5.3 TCO Items Often Omitted from the Quotation

- Engineering and studies: load profile, harmonic study, short-circuit study, motor compatibility, cable length, EMC and control architecture.

- Installation and downtime: cabinet modifications, power cabling, control wiring, shutdown window, testing and production interruption.

- Energy and power quality: drive losses, part-load efficiency, harmonic losses, power factor, transformer loading and utility demand charges.

- Reliability: fan and capacitor replacement, contamination, cooling, nuisance trips, bypass availability, firmware support and spare-unit strategy.

- Motor-system effects: dv/dt stress, common-mode voltage, bearing currents, acoustic noise, cooling at low speed and overspeed risk.

- End-of-life economics: expected service life, repairability, obsolescence, spare-parts support, residual value and migration path.

6. Global and Regional Delivered-Cost Analysis

The same drive can have materially different delivered costs across regions because voltage standards, certification, distribution structure, freight, duties, exchange rates, local labour and service obligations vary. The table below summarises the most important procurement effects rather than presenting unsupported regional average prices.

|

Region |

Typical cost position |

Key delivered-cost modifiers |

Procurement emphasis |

|

China and East Asia |

Highly competitive for standard low-voltage drives; broad OEM and component ecosystem |

Export certification, language/documentation, freight, duty, local service and spare-part lead time |

Verify product platform maturity, reference sites, certification validity and support outside the home market |

|

European Union / EEA |

Higher compliance and service content; strong process and energy-efficiency focus |

IE2 ecodesign, CE/EMC documentation, labour, distributor margin and local technical support |

Request part-load loss data, EU declaration documentation, harmonics and lifecycle service scope |

|

North America |

Retail and distribution prices can be high; strong UL/NEMA and channel-service content |

UL listing, SCCR, NEMA enclosure, local panel integration, tariffs, freight and warranty |

Compare chassis drive versus complete listed panel; verify short-circuit rating and field-service response |

|

India |

Price-sensitive market with expanding local manufacturing and assembly |

Import duty, local content, BIS/utility or project specifications, heat and dust conditions |

Check derating, local spares, service network and whether the quoted duty rating matches the load |

|

Middle East |

Demand often favours robust cooling, outdoor or process configurations |

High ambient temperature, dust, IP rating, harmonic limits, project approvals and local agent margin |

Specify ambient/altitude derating, enclosure cooling, redundancy and long-term spares |

|

Latin America |

Imported equipment and currency movement can dominate the final price |

FX volatility, customs, inland logistics, local taxes, lead time and service coverage |

Lock price-validity and currency terms; require local commissioning and spare strategy |

|

Africa |

Headline equipment price can be secondary to logistics and maintainability |

Freight, customs, voltage quality, dust/heat, limited local stock and long repair cycles |

Prioritise ruggedness, simple maintenance, local training, surge protection and critical spares |

Table 8. Regional drivers of VFD delivered cost

6.1 Europe: Efficiency Data Are Part of Market Access

The EU Ecodesign Regulation applies to in-scope motors and variable speed drives placed on the EU market. It entered into application on 1 July 2021 and requires in-scope drives to reach IE2. Manufacturers must also provide information at different load points, which supports system-level optimisation. [6]

Because IEA 4E testing found that almost all sampled converters already met IE2, a buyer should not assume that an IE2 label by itself proves superior lifecycle economics. The more useful comparison is the loss map at actual torque and speed points, together with harmonic performance, cooling, motor-system effects and application-specific controls.

6.2 North America: The Panel Can Cost More Than the Drive

North American projects frequently require UL-listed assemblies, defined short-circuit current ratings, NEMA enclosures, disconnects, bypasses and local panel-shop integration. A chassis-drive web price is therefore a poor proxy for the installed project cost. The difference between a bare drive and a listed bypass panel can include protective devices, wiring, thermal management, documentation, testing and field labour.

6.3 Emerging Markets: Service and Currency Risk Can Dominate

In markets with volatile currencies, limited spare stock or long customs cycles, the cheapest imported drive can create the highest downtime exposure. Buyers should evaluate the replacement lead time, whether firmware and parameter files are locally supported, the availability of fans and capacitors, and whether a spare drive can be kept in a standardised configuration across multiple motor ratings.

7. Competitive Logic and Technology Direction

7.1 From Unit Price to Lifecycle and Process Value

Low-price competition remains intense in microdrives, HVAC and standard machinery. However, competition in water, oil and gas, mining, metals, marine, data centres and continuous-process industries increasingly centres on uptime, process control, functional safety, harmonics, cybersecurity, predictive maintenance, digital services and long-term support. A drive supplier with a larger installed base can command a premium when the buyer values rapid replacement, parameter migration and service coverage.

7.2 Efficiency Classes Are Necessary but Not Sufficient

IEC 61800-9-2:2023 defines energy-efficiency indicators and IE/IES classes for complete drive modules and power drive systems and links efficiency evaluation to the speed/torque profile and operating points over time. This extended-product approach is more economically meaningful than a single full-load efficiency number. [7]

The 2026 IEA 4E EMSA policy brief states that motor systems account for 53% of global electricity consumption and that available technologies could reduce motor-system demand by 20-30%. This is a system-level opportunity, not a guaranteed saving from installing a VFD on every motor. [8]

7.3 Digitalisation and Service Bundles

Embedded connectivity, condition monitoring, cloud diagnostics and asset-management software are shifting part of the value from hardware to lifecycle services. These features can reduce commissioning and unplanned downtime, but they also introduce protocol, cybersecurity, software-maintenance and vendor-lock-in considerations. Buyers should specify data ownership, local operation during cloud outages, firmware support duration and secure remote-access responsibilities.

8. Procurement Recommendations

8.1 Minimum Technical and Commercial Comparison Sheet

|

Category |

Minimum items to compare |

Commercial risk if omitted |

|

Electrical rating |

Input voltage/frequency, continuous output current, duty class, overload, switching frequency, short-circuit rating |

Undersized drive, nuisance trips, reduced life or invalid warranty |

|

Application |

Load torque, speed range, static head, starts/hour, regenerative operation, process criticality |

Incorrect energy-savings estimate and unsuitable control mode |

|

Environment |

Ambient temperature, altitude, dust, humidity, corrosion, enclosure and cooling |

Derating, overheating, contamination and premature failure |

|

Motor system |

Motor type, insulation, cable length, grounding, bearings, low-speed cooling |

dv/dt damage, bearing currents, overheating and acoustic problems |

|

Power quality |

THDi target, line impedance, reactor/filter, EMC, power factor |

Utility non-compliance, transformer heating and interference |

|

Controls and safety |

I/O, encoder, fieldbus, STO/SIL, local/remote mode, cybersecurity |

Integration delay, safety non-compliance and software rework |

|

Scope and terms |

Incoterm, packing, freight, tax, installation, commissioning, training, spares |

Non-comparable bids and unbudgeted delivered cost |

|

Warranty and service |

Warranty exclusions, response time, local engineer, spare stock, repair/replace policy |

Long downtime and disputed responsibility |

|

Lifecycle data |

Part-load losses, fan/capacitor life, maintenance, obsolescence and migration path |

Higher TCO despite a low initial quotation |

Table 9. VFD procurement comparison checklist

8.2 Recommended Bid-Normalisation Process

- Freeze the load and duty basis before requesting prices: motor current, torque curve, speed range, ambient conditions, cable length and process criticality.

- Separate the quotation into base drive, mandatory accessories, enclosure/panel, engineering, installation, commissioning, training, spares, warranty and service.

- Normalise all bids to the same Incoterm, currency date, tax basis, delivery destination and warranty period.

- Calculate delivered installed cost, then add energy, maintenance, downtime and replacement assumptions over the selected analysis period.

- Run a technical deviation review before commercial ranking. A cheaper bid with exclusions should not be treated as equivalent.

- Require reference projects in comparable duty, environment, voltage and process conditions, not only the same nominal horsepower.

- For critical facilities, assess supplier financial strength, firmware support, cyber policy, repair lead time and local spare inventory.

8.3 Red Flags

- Price quoted only by horsepower without continuous current and overload duty.

- No statement on ambient-temperature or altitude derating.

- No harmonic, EMC or motor-cable compatibility boundary.

- An IP rating applied to the keypad or front face rather than the complete installed assembly.

- Warranty that excludes the actual operating environment or requires unavailable local service.

- Energy-savings claim without a measured duty cycle and baseline control method.

- No migration plan for discontinued firmware, keypad or communication option.

9. Price Outlook for 2026-2028

9.1 Base Case

The most likely outcome is not a single global price direction. Standard low-voltage drives should remain under strong competitive pressure as suppliers reuse platforms, integrate electronics and expand Asian manufacturing. This should limit factory-price growth for commodity products. However, the broad industrial-control PPI and current metal prices indicate that manufacturers still face elevated labour, electronics, compliance and channel costs. Nominal prices in mature distribution markets are therefore more likely to remain firm than to return to pre-2021 levels.

Process-grade, low-harmonic, regenerative, safety-certified and enclosed systems are likely to retain better pricing power because their value includes engineering, software, certification and service. Buyers may see lower base-drive prices but higher total packages when projects add harmonic limits, functional safety, cybersecurity, outdoor enclosures, bypass, redundancy and extended support.

|

Scenario |

Key assumptions |

Expected price effect |

Procurement response |

|

Base case |

Moderate metal prices, normal semiconductor supply, stable freight, continued competition |

Commodity drive prices broadly stable to modestly higher in nominal terms; configured systems firmer |

Use multi-year framework pricing but preserve specification and lifecycle comparison |

|

Cost-down case |

Weaker industrial demand, lower electronics and freight cost, aggressive Asian capacity expansion |

Lower factory prices for standard drives; less benefit on local panels and service |

Separate drive module from local integration to capture savings transparently |

|

Cost-up case |

Copper/aluminium spike, trade restrictions, currency depreciation, logistics disruption |

Delivered prices rise faster than factory prices; long lead times and quote-validity risk |

Lock currency/Incoterm, secure critical spares and evaluate local assembly |

|

Technology premium case |

Faster adoption of active front ends, SiC, digital services and safety functions |

Higher initial price with potential energy, size or process benefits |

Require measured system benefit and motor-compatibility validation before paying a premium |

Table 10. VFD price outlook scenarios for 2026-2028

9.2 Most Important Watch Indicators

- BLS producer-price data for general-purpose industrial controls and electrical equipment.

- Copper and aluminium benchmark prices, particularly when combined with currency movement.

- Power semiconductor lead times and supplier product-change notifications.

- Ocean freight, customs rules and trade-remedy measures affecting static converters and components.

- EU ecodesign review and updates to IEC 61800-9-2 and related motor-system standards.

- Public distributor pricing and lead-time changes for matched model families rather than isolated products.

- Supplier service-network changes, warranty terms and availability of fans, capacitors and control boards.

Conclusion

The VFD market cannot be described by a single global price curve. The strongest public evidence shows that the broader industrial-control manufacturing environment became substantially more expensive between 2021 and 2025, while metal inputs moved in different directions. At the same time, current public quotations show that standard compact drives remain highly price-competitive and that configuration can create several-fold price differences at the same horsepower.

For buyers, the decisive economic question is not whether the drive is cheap, but whether the complete motor system achieves the required duty, power quality, reliability and energy performance at the lowest delivered lifecycle cost. The largest savings are available in well-selected variable-torque applications with long operating hours and inefficient baseline control. The largest procurement failures occur when horsepower is used as the only comparison basis and the buyer ignores current rating, overload, derating, harmonics, motor insulation, enclosure, service and commissioning scope.

Through 2028, competition should continue to compress prices for standard low-voltage units, but configured, low-harmonic, regenerative, safety and process systems will remain value-priced. The winning suppliers will be those that combine competitive hardware with verifiable part-load data, application engineering, local service, spare-parts availability and a credible lifecycle support path.