1. Executive Summary

The global steam turbine market occupies a paradoxical position in the energy transition narrative: widely viewed as a legacy technology tied to fossil fuel-based thermal power, yet simultaneously indispensable to grid stability, industrial process heat, nuclear baseload generation, and the emerging hydrogen economy. Understanding this duality is essential to evaluating the market's trajectory.

Cross-referencing data from Grand View Research, Mordor Intelligence, Arizton, and DataHorizzon Research, the global market for

steam turbines was valued between USD 18.2 billion and USD 19.5 billion in 2024, and is projected to reach between USD 22.5 billion and USD 24.8 billion by 2032-2033, translating to a compound annual growth rate of 2.5% to 3.5% over the forecast horizon. The variance between estimates reflects different statistical scopes—some research houses include aftermarket services and balance-of-plant equipment in their coverage, while others confine the definition to OEM equipment revenue.

Asia Pacific dominates with approximately 47.6% of global revenue, driven by continued coal-fired capacity expansion in India and Southeast Asia, supercritical and ultra-supercritical retrofits, and a large nuclear new-build pipeline. The Middle East & Africa region, while accounting for just 12% of 2025 revenue, is the fastest-growing market with a projected 5.3% CAGR to 2031, fueled by Saudi Arabia's gas-fired IPP program and the UAE's Barakah nuclear expansion.

■ Key Data at a Glance

|

Metric |

Value / Range |

Source(s) |

|

Market Size (2024E) |

USD 18.2 - 19.5 billion |

GVR, Arizton, DataHorizzon, Mordor Intelligence |

|

2032E Projected Size |

USD 22.5 - 24.8 billion |

Multiple; median ~USD 23 billion |

|

Forecast CAGR |

2.5% - 3.5% |

Range from four research houses |

|

Largest Region (2025) |

Asia Pacific (~47.6% share) |

Mordor Intelligence, Fundamental BI |

|

Fastest-Growing Region |

Middle East & Africa (5.3% CAGR) |

Mordor Intelligence |

|

Dominant Capacity Segment |

300-600 MW (~59.8% share) |

Mordor Intelligence / GVR |

|

Largest Fuel Application |

Coal (~58.5% of turbine revenue) |

Mordor Intelligence |

|

Top OEM by Revenue |

Siemens Energy (est. ~16% share) |

GVR, Mordor Intelligence, GMI |

|

Aftermarket Market Size (2025) |

USD 12.5 billion |

Arizton |

|

Global Coal Fleet (2024) |

~2,130 GW operating capacity |

Global Energy Monitor |

|

Nuclear Units Under Construction |

~60 reactors / ~60.5 GW |

IAEA PRIS, WNA (early 2024) |

2. Market Sizing & Growth Trajectory

Quantifying the steam turbine market requires careful attention to methodological differences among research providers. The table below presents a cross-section of the most frequently cited estimates, illustrating the range that results from varying coverage definitions.

TABLE 1: Global Steam Turbine Market Size — Multi-Source Comparison

|

Research House |

Base Year |

Base Value |

Target Year |

Target Value |

CAGR |

Scope Notes |

|

Grand View Research |

2022 |

USD 16.27B |

2030 |

USD 19.64B |

2.5% |

OEM equipment; capacity + end-use segments |

|

Mordor Intelligence |

2026 |

USD 19.33B |

2031 |

USD 22.48B |

3.07% |

Includes services; fuel + technology + region |

|

Arizton |

2024 |

USD 19.50B |

2030 |

USD 23.48B |

3.15% |

Equipment + aftermarket bundled |

|

DataHorizzon Research |

2024 |

USD 18.20B |

2033 |

USD 24.80B |

3.5% |

Broad scope incl. industrial turbines |

|

The Business Research Co. |

2024 |

USD 19.51B |

2028 |

USD 22.70B |

3.9% |

Includes turbine-generator sets |

|

Global Market Insights |

2025 |

USD 26.20B |

2035 |

— |

— |

Widest scope; likely incl. full BOP equipment |

Source: Respective research house publications (accessed July 2026). Scope differences account for valuation spread.

The market's growth trajectory, though modest by the standards of high-growth technology sectors, reflects genuine structural expansion rather than cyclical fluctuation. Two dynamics deserve emphasis. First, the 2021-2023 period witnessed a post-pandemic rebound in thermal power plant commissioning, with global coal capacity additions of approximately 70 GW in 2023 alone, according to Global Energy Monitor. Second, the market's growth rate is being simultaneously lifted by modernization and aftermarket intensity and weighed down by the ongoing retirement of coal-fired plants in Europe and North America. The net effect is a market that grows but at a decelerating pace—the 3.0-3.5% CAGR observed in the near term is expected to moderate toward 2.0-2.5% beyond 2030 as the global coal fleet enters structural decline.

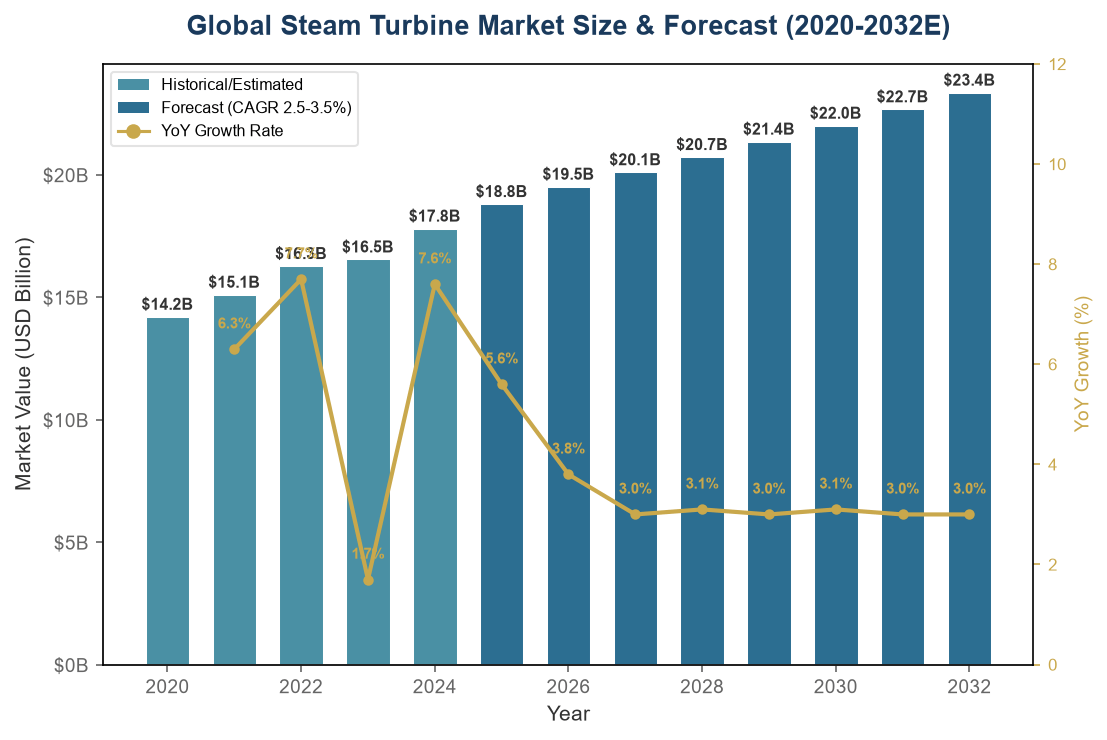

Figure 1: Global Steam Turbine Market Size & Forecast (2020-2032E). Sources: Grand View Research, Mordor Intelligence, Arizton, DataHorizzon Research. Note: 2020-2024 figures are historical/estimated; 2025E-2032E are consensus forecasts.

Figure 1 illustrates the compound effect of moderate but persistent annual growth: over the 2020-2032 window, the market expands by roughly 65%, from an estimated USD 14.2 billion to USD 23.4 billion. The year-over-year growth rate peaks in 2022-2023 as the global energy crisis spurred accelerated fossil fuel investment in Europe and Asia, before settling into the 3% range that most analysts view as the market's "new normal" growth equilibrium.

3. Global Power Generation Capacity: The Demand-Side Narrative

Steam turbines are, at their core, thermal power conversion machines. Their demand is therefore inseparable from the global trajectory of

thermal power generation technology, encompassing coal, natural gas (combined cycle), nuclear, biomass, waste-to-energy, and concentrated solar power. Understanding the installed base and the new-build pipeline across each fuel type is essential to assessing the turbine market's forward demand profile.

3.1 Coal: The Declining Giant That Still Dominates

As of year-end 2024, global operating coal-fired capacity stood at approximately 2,130 GW, according to Global Energy Monitor. Net capacity increased by just 18.8 GW in 2024—the smallest annual addition in two decades—yet the pipeline of plants under construction or in pre-construction stages remains substantial, concentrated overwhelmingly in India, Indonesia, Vietnam, and Bangladesh. Mordor Intelligence estimates that coal-fired applications still accounted for 58.5% of steam turbine industry revenue in 2025. This share is expected to decline gradually but remain above 50% through 2030, driven by ongoing construction completions and ultra-supercritical retrofits in Asia.

The critical nuance: new coal plant orders are increasingly concentrated in just a handful of countries. Outside these geographies, the coal turbine market is transitioning entirely to a replacement-and-services model—a shift with significant implications for OEM revenue mix and aftermarket intensity.

3.2 Natural Gas: The Bridge Fuel with Staying Power

Combined-cycle gas turbine (CCGT) plants—in which a steam turbine operates in tandem with one or more gas turbines—represent the largest growth opportunity for steam turbines in developed markets. The U.S. Energy Information Administration projects approximately 20 GW of new CCGT capacity additions through 2027 in the United States alone. In the Middle East, Saudi Arabia's 30 GW gas-fired independent power producer (IPP) program represents one of the largest single-market opportunities for steam turbine OEMs globally. In Europe, the drive toward hydrogen-ready gas plants is creating a new category of "transition-ready" steam turbines designed to accommodate future fuel switching with minimal retrofit cost.

3.3 Nuclear: Long-Cycle, High-Value Orders

The nuclear steam turbine market operates on fundamentally different rhythms than fossil-fuel segments. With approximately 60 reactors (60.5 GW) under construction across 16 countries as of early 2024—per IAEA PRIS and World Nuclear Association data—each reactor represents a single, high-value turbine order with a typical lead time of 3-5 years from contract award to commissioning. The geographic distribution of these orders is heavily skewed: China accounts for 26 of the 60 units under construction, with the remainder spread across India, Russia, South Korea, the UAE, Turkey, Egypt, Bangladesh, and several European nations.

For turbine OEMs, the

nuclear power plant equipment segment is characterized by very large individual contract values but extremely lumpy order intake. A single 1,400 MW nuclear turbine order can be worth USD 200-400 million excluding installation—equivalent to the revenue from dozens of smaller industrial CHP turbines. Toshiba Energy Systems & Solutions and Arabelle Solutions (formerly part of GE) are the dominant suppliers in this segment, with Mitsubishi Heavy Industries and Doosan Enerbility occupying strong regional positions.

3.4 Biomass, Waste-to-Energy, and CSP: The High-Growth Niches

Biomass and waste-to-energy steam turbines are growing at approximately 5.1% CAGR—the fastest among all fuel applications—albeit from a small base of roughly 5.5% of total turbine revenue. Northern Europe is the epicenter of this growth, where biomass-fired CHP plants achieve fuel utilization rates exceeding 85% and generate renewable energy certificates that add a meaningful revenue layer. In Brazil, sugarcane bagasse-fired cogeneration plants—often equipped with extraction-condensing steam turbines in the 50-150 MW range—benefit from feed-in tariffs of USD 70-80/MWh. Concentrated solar power (CSP), though still a niche at approximately 2% of turbine revenue, represents a strategically important growth vector, particularly in the Middle East and North Africa, where the combination of high direct normal irradiance and molten salt storage enables dispatchable renewable power.

4. Regional Market Dynamics

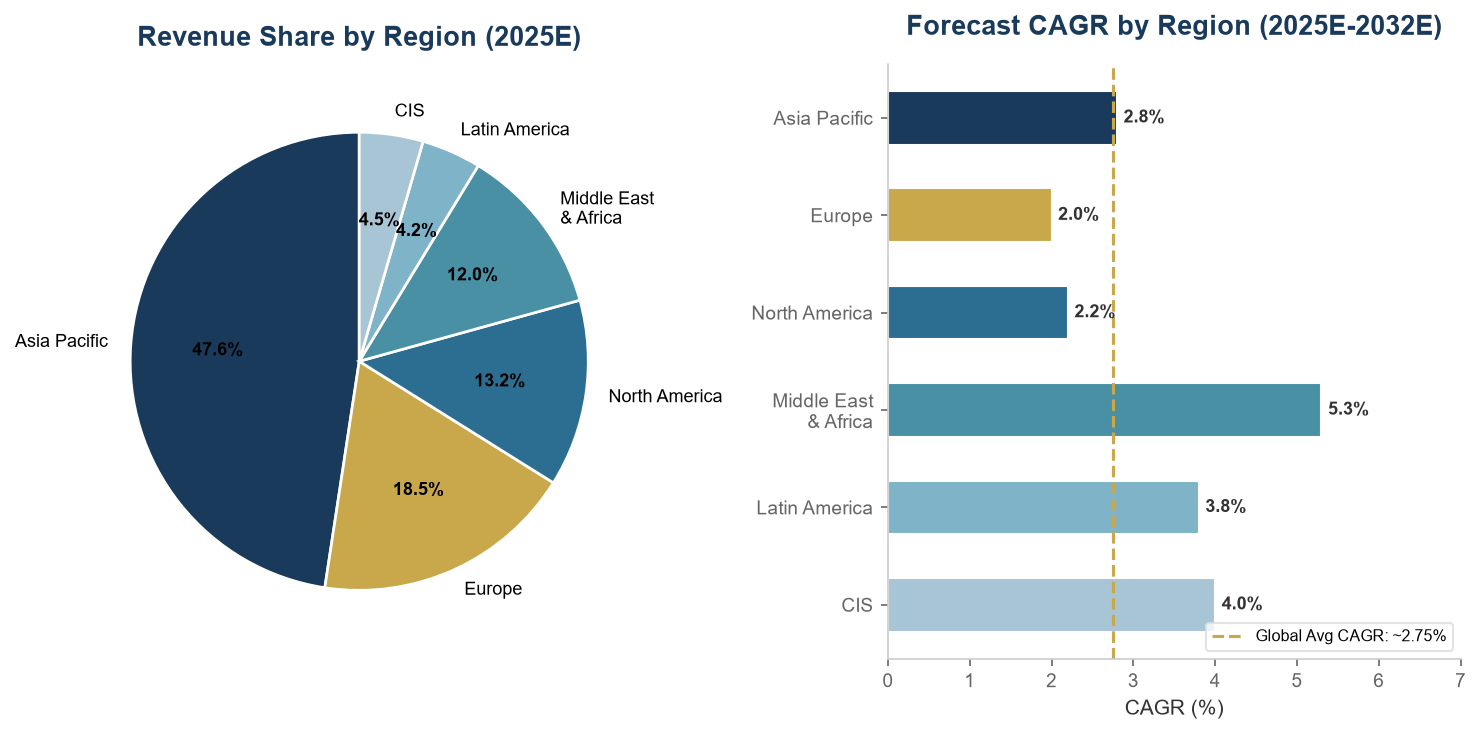

Figure 2: Steam Turbine Revenue Share by Region (2025E) and Forecast CAGR (2025E-2032E). Sources: Mordor Intelligence, Grand View Research, Fundamental Business Insights.

TABLE 2: Regional Steam Turbine Market — Comparative Profile

|

Region |

2025E Share |

CAGR (E) |

Primary Demand Drivers |

Dominant Turbine Types |

|

Asia Pacific |

~47.6% |

~2.8% |

Coal new-builds + retrofits; nuclear; industrial CHP |

300-600 MW USC, nuclear, industrial CHP |

|

Europe |

~18.5% |

~2.0% |

Biomass CHP, H₂-ready CCGT, industrial process steam |

<300 MW CHP, combined-cycle ST |

|

North America |

~13.2% |

~2.2% |

CCGT additions, coal-to-gas switching, industrial CHP |

Combined-cycle ST, CHP <150 MW |

|

Middle East & Africa |

~12.0% |

~5.3% |

Gas IPP, nuclear new-builds, desalination CHP |

300-600 MW CCGT ST, nuclear |

|

Latin America |

~4.2% |

~3.8% |

Biomass CHP, gas IPP, mining power |

<300 MW CHP, industrial |

|

CIS |

~4.5% |

~4.0% |

Nuclear, district heating, gas-fired CHP |

Nuclear turbine, Cogeneration ST |

Source: Mordor Intelligence, Grand View Research, DataHorizzon Research, Fundamental Business Insights (2025-2026). Note: Regional shares are indicative and vary by source.

4.1 Asia Pacific: Scale and Structural Momentum

The region's dominance—approaching half of global turbine revenue—is underpinned by a fundamental reality: Asia Pacific is where the world's thermal power capacity is being built, upgraded, and replaced. India's thermal power capacity target of approximately 280 GW by 2032 (from roughly 218 GW in 2024) requires turbine orders at a pace not seen since China's 2005-2015 buildout cycle. In Southeast Asia, an estimated 15 GW of new CHP capacity is projected to come online between 2025 and 2028, driven by post-inflation industrial capital expenditure cycles in Indonesia, Vietnam, and the Philippines. Japan and South Korea, while mature markets, are generating demand through plant modernization programs and an emerging hydrogen co-firing retrofit market.

4.2 Middle East & Africa: The Growth Outlier

The 5.3% CAGR projected for the Middle East & Africa is unmatched by any other region and reflects a confluence of structural factors: Saudi Arabia's plan to replace liquid fuel-fired power generation with gas, adding approximately 30 GW of CCGT capacity by 2030; the UAE's Barakah nuclear plant reaching full four-unit operation; and Egypt's El Dabaa nuclear project (4.8 GW, four VVER-1200 units) representing one of the largest single nuclear turbine contracts outside Asia. The region's market share is projected to expand from 12% in 2025 to approximately 15% by 2031.

4.3 Europe & North America: Managed Decline, Service Intensity

In Europe and North America, the steam turbine market is defined less by new capacity additions and more by the intensifying demands of an aging installed base. The average age of the European coal fleet exceeds 35 years; in the United States, it exceeds 40 years. While coal retirements are accelerating—the U.S. retired approximately 5 GW in 2024 and Europe approximately 8 GW—the remaining fleet requires sustained investment in turbine upgrades, boiler retrofits, and emissions control retrofits to meet tightening environmental regulations. This dynamic shifts the revenue model from new equipment sales toward high-margin aftermarket services, a theme explored in detail in Section 7.

5. Technology & Capacity Segmentation

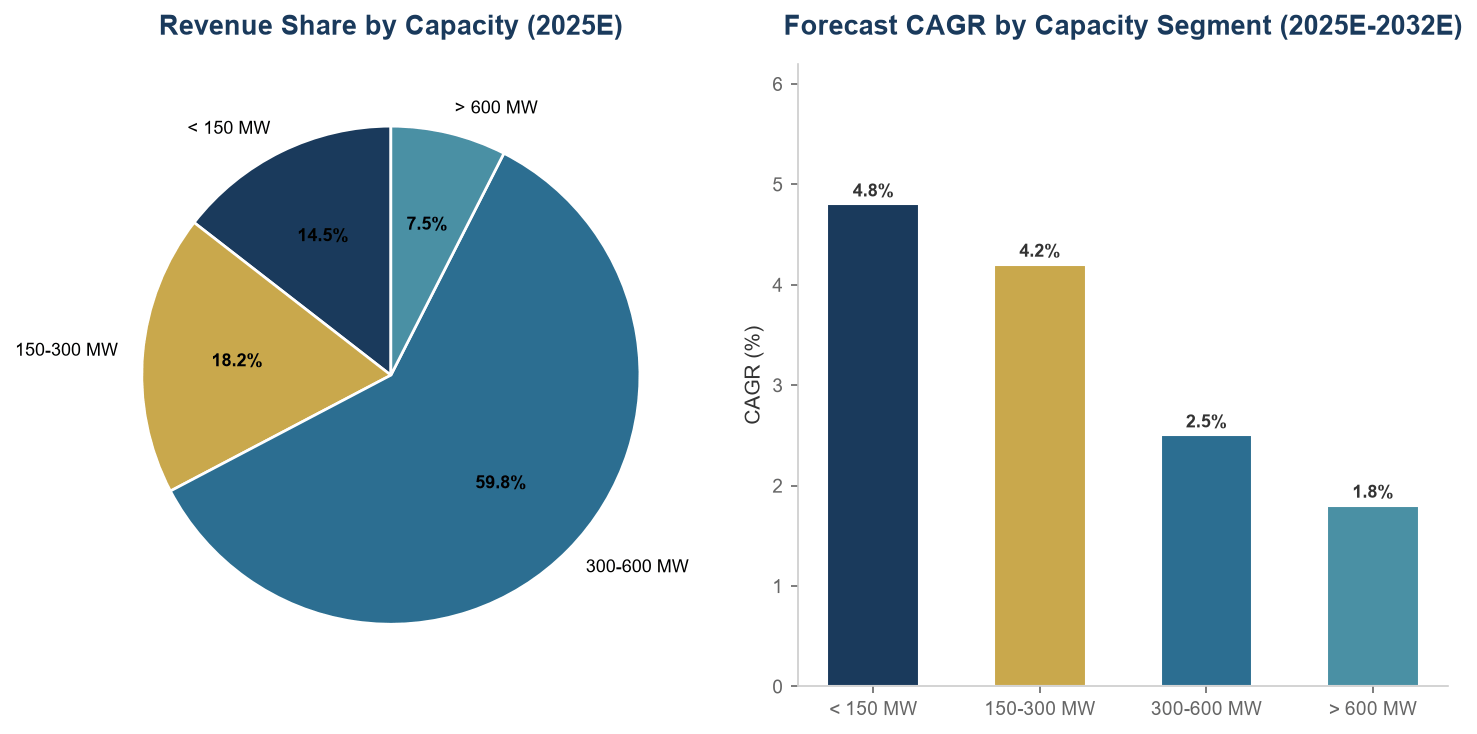

Figure 3: Steam Turbine Revenue Share by Capacity Segment (2025E) and Forecast CAGR. Sources: Grand View Research, Mordor Intelligence.

The 300-600 MW segment dominates with approximately 59.8% of industry revenue, reflecting its central role in utility-scale combined-cycle plants and supercritical/ultra-supercritical coal units. This capacity range aligns with standard grid interconnection requirements, transformer ratings, and the economic "sweet spot" for thermal power plants in most developing economies.

The sub-300 MW segment, however, is the growth leader at approximately 4.8% CAGR, driven by the expansion of industrial cogeneration, biomass CHP, and decentralized power generation in regions with unreliable grid supply. Turbines in the 150-250 MW extraction-condensing configuration are particularly in demand from petrochemical complexes, where they simultaneously supply process steam and export power to the grid.

Grand View Research identifies the 151-300 MW band as the "most lucrative" capacity segment—a function of its versatility across both utility-scale and industrial applications. The segment benefits from being large enough to achieve competitive heat rates (typically 8,500-9,500 BTU/kWh in steam-cycle config) while small enough to be rapidly deployable, with typical lead times of 18-24 months versus 30-36 months for units above 600 MW.

TABLE 3: Capacity Segment — Key Characteristics

|

Capacity Band |

2025E Rev. Share |

CAGR (E) |

Primary Applications |

Lead Time |

|

<150 MW |

~14.5% |

4.8% |

Industrial CHP, biomass, waste-to-energy, mining |

12-18 months |

|

150-300 MW |

~18.2% |

4.2% |

Petrochemical CHP, CCGT bottoming cycle, CSP |

18-24 months |

|

300-600 MW |

~59.8% |

2.5% |

Utility CCGT, supercritical coal, nuclear |

24-30 months |

|

>600 MW |

~7.5% |

1.8% |

Ultra-supercritical coal, large nuclear |

30-36+ months |

Source: Grand View Research (2023), Mordor Intelligence (2025). Lead times are indicative OEM averages.

5.1 Fuel Application Analysis

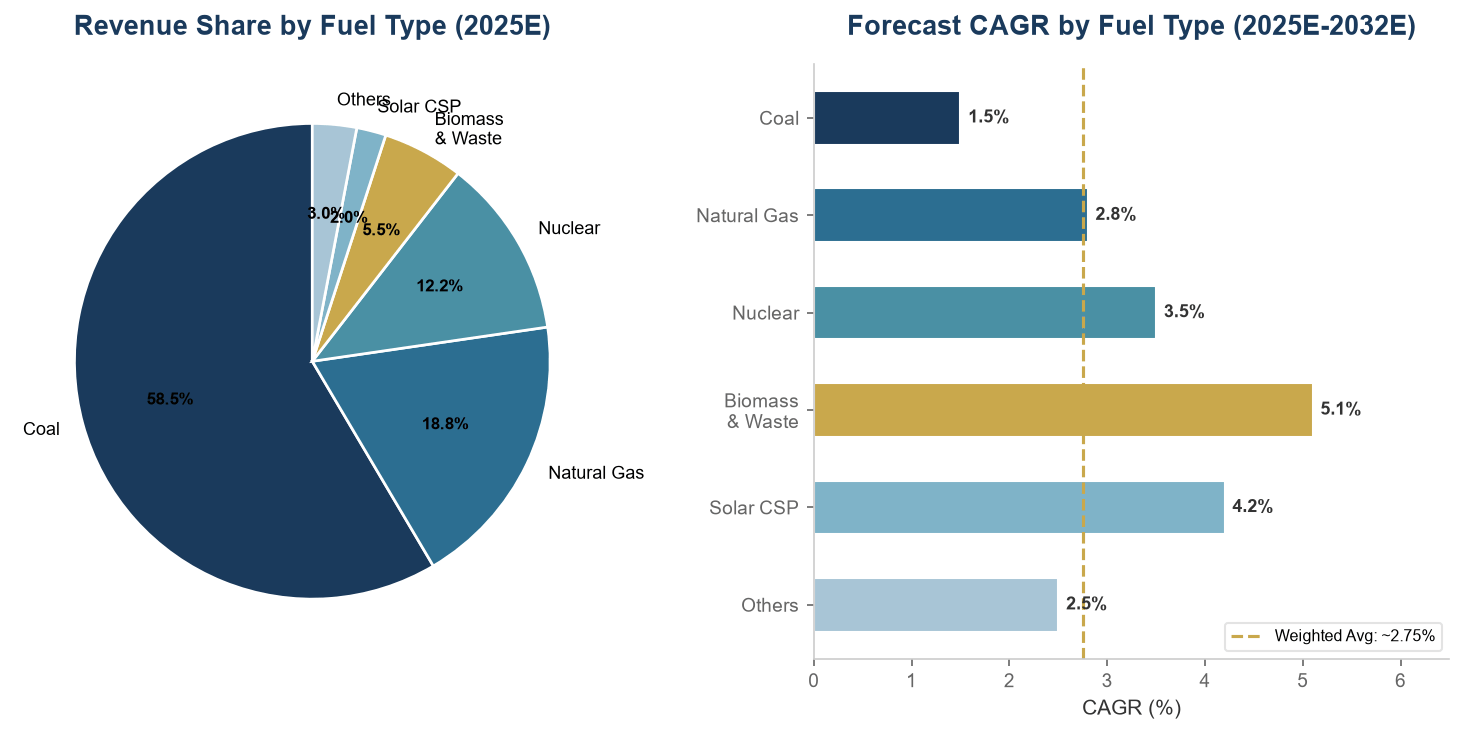

Figure 4: Steam Turbine Revenue Share by Fuel Type (2025E) and Forecast CAGR. Sources: Mordor Intelligence, Grand View Research.

The fuel application data reveals a market in transition. Coal retains its dominant share of turbine revenue at 58.5%, but this figure masks significant regional divergence: in India and Southeast Asia, coal drives new orders; in Europe and North America, it drives replacement parts and upgrade services. Natural gas-fired CCGT applications account for approximately 18.8% of revenue and are growing at 2.8%—reflecting both new plant construction in gas-rich regions and the enduring efficiency advantages of combined-cycle configurations, which can achieve net electrical efficiencies exceeding 62% (GE Vernova 9HA.02 reference).

Nuclear applications, at 12.2% of revenue, exhibit the highest per-unit value but the most erratic order intake pattern. A single year can see anywhere from two to eight large nuclear turbine contracts globally—a dispersion that creates planning challenges for the specialized manufacturing facilities required for nuclear-grade turbines. The biomass/waste-to-energy category, while starting from a modest 5.5% share, is growing at 5.1% CAGR and represents the segment with the strongest alignment to energy transition tailwinds.

Hydrogen co-firing—where existing gas-fired steam turbines are retrofitted to combust a blend of natural gas and hydrogen (typically 30-50% H₂ by volume)—is in the pilot and demonstration phase. Mitsubishi Heavy Industries has been the most aggressive in commercializing this technology, with several full-scale demonstrations completed in Japan. While hydrogen-ready turbines are unlikely to drive material revenue before 2030, they represent a critical strategic option value for turbine OEMs positioning for a post-combustion energy landscape.

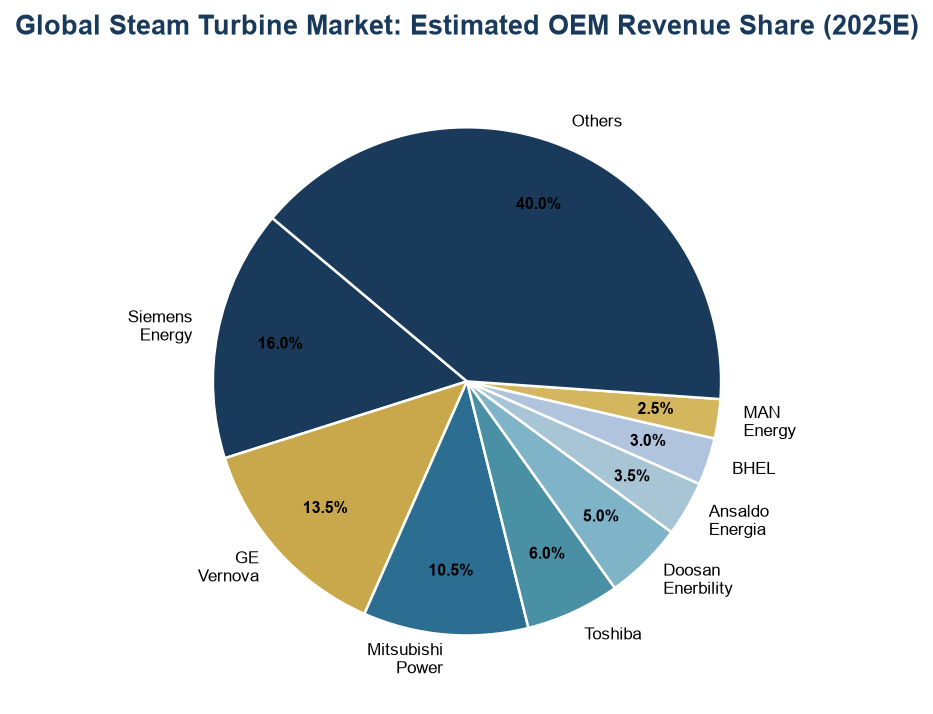

6. Competitive Landscape: The Global Heavyweights

Figure 5: Estimated Global Steam Turbine OEM Revenue Share (2025E). Sources: Grand View Research, Mordor Intelligence, Global Market Insights, company filings.

The global steam turbine market exhibits a "moderately concentrated" competitive structure. The top five OEMs—Siemens Energy, GE Vernova, Mitsubishi Heavy Industries (Mitsubishi Power), Toshiba Energy Systems & Solutions, and Doosan Enerbility—collectively control an estimated 50-55% of global installed capacity and an even larger share of the large-frame (>300 MW) segment. Below the top tier, a diverse ecosystem of regional champions and specialized niche players competes in specific capacity bands, geographies, and end-use applications.

6.1 Tier-One OEM Profiles

▎ Siemens Energy AG (Germany)

With an estimated 16% global revenue share, Siemens Energy is the market's largest participant by a narrow margin. The company's competitive advantage rests on three pillars: a dominant position in the European and Middle Eastern utility markets; a remote monitoring and diagnostics platform covering over 600 turbines globally, which the company reports has reduced unplanned outages by approximately 20%; and deep vertical integration across the thermal power value chain, from gas turbines through steam turbines to generators and control systems. The SST-600, SST-800, and SST-900 series cover the full capacity range from 10 MW industrial units to 250 MW utility-class machines.

▎ GE Vernova (USA)

GE Vernova holds approximately 13.5% of global revenue, with particular strength in the North American CCGT market, where its HA-class combined-cycle configuration—pairing the 9HA.02 gas turbine with a bottoming-cycle steam turbine—has set efficiency benchmarks exceeding 62% net LHV. The company's use of additive manufacturing for steam turbine nozzles has reduced production lead times by approximately 40%, a competitive edge in a market where delivery speed increasingly determines contract awards.

▎ Mitsubishi Heavy Industries / Mitsubishi Power (Japan)

MHI commands an estimated 10.5% share, with a technology portfolio distinguished by its leadership in hydrogen combustion—a strategic asset as hydrogen-ready gas turbines begin to enter commercial service. The company has also maintained a strong position in the Southeast Asian and Japanese nuclear steam turbine markets. MHI's J-series gas turbine, when paired with its steam turbine in combined-cycle configuration, achieves reliability rates exceeding 99.5%.

▎ Toshiba Energy Systems & Solutions (Japan)

Toshiba holds approximately 6% of global revenue, with a distinctive competitive position in geothermal steam turbines—a niche where the company has deployed over 60 units totaling approximately 3,800 MW globally. Toshiba's nuclear steam turbine business, operated through its Toshiba JSW joint venture in India, secured a landmark order in January 2026 for two 800 MW turbine-generator sets for the Salboni thermal power project in West Bengal, India. The company has also deployed its EtaPRO AI-based monitoring system across 165 power plants.

▎ Doosan Enerbility (South Korea)

With an estimated 5% global share, Doosan is the dominant supplier to the Korean market and has been expanding its footprint in the Middle East and South Asia. The company is the steam turbine supplier for the UAE's Barakah nuclear plant—the first operational nuclear power station in the Arab world—and is actively pursuing additional nuclear turbine contracts in Egypt and Saudi Arabia.

6.2 Regional Champions and Niche Specialists

Bharat Heavy Electricals Limited (BHEL) dominates the Indian market with an installed base exceeding 180 GW of power generation equipment, of which steam turbines represent a substantial portion. Ansaldo Energia (Italy) maintains a strong position in the Mediterranean and North African markets, with particular expertise in hydrogen-ready gas turbine configurations. Elliott Group and MAN Energy Solutions focus on the mechanical drive and industrial process steam segments below 100 MW. In the sub-30 MW CHP segment, India's Triveni Turbines has emerged as a global leader, exporting to over 70 countries. Brazil's WEG S.A. has carved a niche in biomass-fired industrial cogeneration turbines.

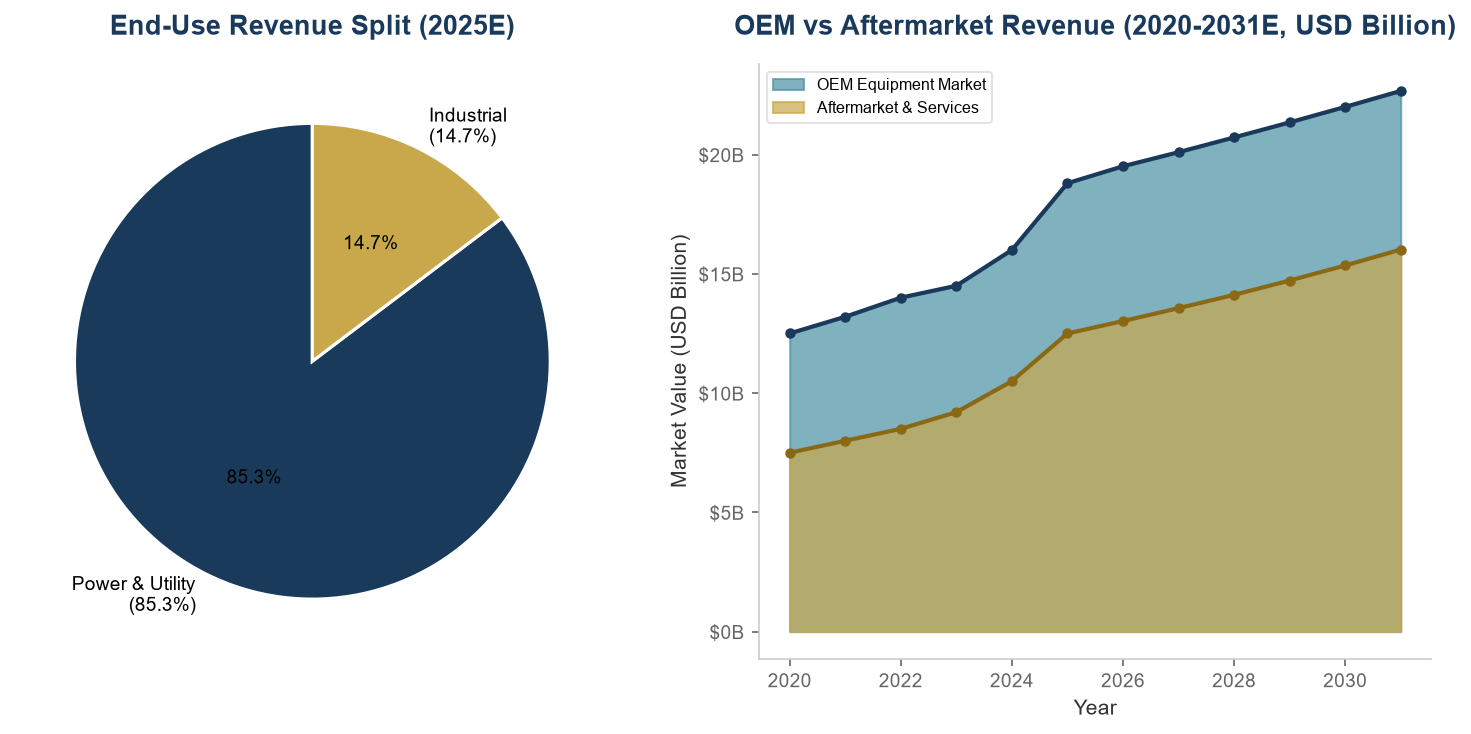

7. Aftermarket & Services: The Hidden Growth Engine

Figure 6: OEM Equipment vs Aftermarket Revenue (2020-2031E, USD Billion). Sources: Arizton, Grand View Research, Mordor Intelligence, TBRC.

Arizton valued the global steam turbine aftermarket at USD 12.5 billion in 2025, with a projected CAGR of 4.22% to reach USD 16.02 billion by 2031—a growth rate notably higher than the 2.5-3.5% projected for the OEM equipment market. This divergence tells a critical story about where value is migrating in the turbine industry.

The aftermarket's superior growth is driven by three structural forces. First, the global installed base of steam turbines—estimated at approximately 1,600-1,800 GW of operating thermal capacity—is aging. Globally, the weighted average age of the coal fleet exceeds 30 years, and combined-cycle plants commissioned during the 2000-2010 buildout wave are entering their first major overhaul cycle (typically at the 15-20 year mark). Each major overhaul of a large-frame steam turbine generates USD 5-15 million in parts, labor, and engineering services revenue.

Second, the tightening of environmental regulations in Europe and North America is driving a wave of emissions-compliance retrofits. The EU's Industrial Emissions Directive (IED) and the U.S. EPA's Mercury and Air Toxics Standards (MATS) require plant operators to invest in turbine upgrades and emissions control retrofits as a condition of continued operation. These mandates effectively convert regulatory compliance costs into turbine aftermarket revenue.

Third, digitalization is transforming the aftermarket from a reactive repair business into a predictive maintenance service. Siemens Energy's remote monitoring platform, covering 600+ turbines, and Toshiba's EtaPRO AI system, deployed across 165 plants, are emblematic of this shift. These platforms use real-time operational data to predict component wear, optimize maintenance schedules, and reduce unplanned outages—creating recurring, high-margin software-enabled service revenue for OEMs while reducing lifecycle costs for plant operators.

8. Technology Trends & Innovation Frontiers

The steam turbine, a technology whose fundamental thermodynamic principles have been understood since the late 19th century, is nonetheless experiencing a period of meaningful innovation. These advances are not about reinventing the Rankine cycle but about optimizing every element of the turbine system—from materials science to digital controls—for a rapidly changing power system.

▎ Ultra-Supercritical & Advanced Ultra-Supercritical (A-USC)

Operating at steam temperatures exceeding 600°C and pressures above 250 bar, USC and A-USC steam turbines achieve net efficiencies of 44-47% (HHV) in coal-fired applications, compared to 35-38% for conventional subcritical plants. This efficiency gain translates to an approximately 18% reduction in CO₂ emissions per MWh. While the technology has been widely deployed in Japan, South Korea, and Germany, the near-term growth market is India, which has committed to USC as the minimum standard for all new coal plants. The materials science challenges of A-USC—requiring nickel-based alloys for the highest-temperature stages—create substantial barriers to entry and concentrate the market among the top-tier OEMs with advanced metallurgy capabilities.

▎ Hydrogen Co-Firing and Ammonia Combustion

Mitsubishi Heavy Industries has conducted full-scale demonstrations of hydrogen co-firing in gas turbines at the Takasago Hydrogen Park in Japan, achieving stable combustion with a 30% hydrogen blend. Siemens Energy has announced plans for 100% hydrogen-capable gas turbines by 2030. For steam turbines, the impact is indirect but significant: hydrogen-ready gas turbines in combined-cycle configuration require steam turbines that can accommodate the altered exhaust gas characteristics (higher moisture content, different temperature profiles) of hydrogen combustion. The retrofit market for steam turbine moisture separation and materials upgrades represents a new revenue stream with a projected addressable market of USD 1.5-2.0 billion by 2035.

▎ Digital Twins and AI-Driven Predictive Maintenance

The deployment of physics-based digital twins—virtual replicas of physical turbines that simulate thermal, mechanical, and metallurgical behavior in real time—is transforming turbine operations and maintenance. GE Vernova's Digital Power Plant suite and Siemens Energy's Omnivise platform use digital twins to predict component fatigue, optimize steam path temperatures, and schedule maintenance interventions with minimal operational disruption. The operational impact is quantifiable: plants using these systems report 15-20% reductions in forced outage rates and 5-8% improvements in heat rate consistency. For OEMs, digital services generate recurring revenue at software-industry margins (typically 40-60% gross margin) within a hardware-centric business.

▎ Additive Manufacturing for Turbine Components

GE Vernova's use of additive manufacturing (3D printing) for steam turbine nozzles and stationary components has reduced production lead times by approximately 40% and material waste by up to 70% compared to traditional casting and machining. Siemens Energy has invested in additive manufacturing facilities dedicated to turbine component production in Finspång, Sweden, and Berlin, Germany. While additive manufacturing is currently limited to non-rotating components due to certification requirements for rotating parts, its expanding application is steadily compressing manufacturing cycles and enabling design geometries—such as conformal cooling channels in nozzle guide vanes—that are impossible to achieve through conventional manufacturing.

▎ Supercritical CO₂ (sCO₂) Power Cycles

A longer-term technology with the potential to disrupt conventional steam cycles is the supercritical CO₂ Brayton cycle, which uses sCO₂ as the working fluid instead of steam. sCO₂ turbines are significantly more compact than steam turbines of equivalent power output—a 300 MW sCO₂ turbine occupies roughly one-tenth the volume of a comparable steam turbine—and can achieve higher thermal efficiencies at lower operating temperatures. While the technology remains pre-commercial, pilot projects at the 10-50 MW scale are underway in the United States (STEP Demo facility in Texas), South Korea, and Europe. Commercialization at utility scale is unlikely before 2035, but sCO₂ represents the most significant potential disruption to conventional steam turbine technology since the introduction of the combined cycle.

▎ Modular and Containerized Turbine Systems

For the sub-100 MW segment, a trend toward modular, factory-assembled turbine-generator packages is reducing on-site installation time by 30-50% compared to traditional stick-built approaches. These systems, which arrive at site on skids or in containers with pre-commissioned auxiliaries, are particularly attractive for mining operations, island grids, and emergency backup power applications where speed of deployment is the primary selection criterion.

9. Growth Drivers & Structural Headwinds

9.1 Growth Drivers

▸ Industrial electrification in emerging economies

The International Energy Agency's Global Energy Review 2025 reported that global electricity demand grew at a faster-than-average pace in 2024. Much of this growth is concentrated in India and Southeast Asia, where grid infrastructure remains coal-dependent and industrial CHP provides a hedge against unreliable utility supply. This dynamic sustains demand for both utility-scale and industrial steam turbines.

▸ Nuclear renaissance in the Middle East and South Asia

The IAEA reports 60 reactors under construction globally, up from 52 in 2019. Each reactor requires a dedicated steam turbine-generator set, creating a visible order pipeline that extends through 2035. The nuclear turbine market is particularly attractive due to its extremely high barriers to entry: only four OEMs globally are qualified to supply nuclear-grade steam turbines.

▸ Coal fleet modernization in Asia

India's commitment to ultra-supercritical technology as the minimum standard for new coal plants, combined with China's ongoing program of replacing subcritical units with USC equivalents, creates a sustained demand stream for high-efficiency steam turbines in the 300-660 MW range. Global Energy Monitor data indicates that over 200 GW of coal capacity in Asia is subcritical and due for replacement before 2040.

▸ Data center and AI-driven power demand

The rapid expansion of data center capacity—particularly for AI training and inference workloads—is creating unexpected demand for firm, dispatchable power. A notable example is Fermi America's July 2025 order for over 600 MW of equipment, including six SGT-800 gas turbines and one SST-600 steam turbine, specifically to power data center loads. This emerging demand category did not exist at meaningful scale five years ago and represents a genuinely new growth vector for the turbine industry.

9.2 Structural Headwinds

▸ Declining LCOE of solar-plus-storage

Utility-scale solar PV paired with four-hour battery storage has reached levelized costs of USD 35-50/MWh in high-irradiance regions, undercutting the operating cost of existing coal plants and approaching the fuel-only cost of combined-cycle gas plants. This represents a structural—not cyclical—threat to the thermal power generation model that underpins steam turbine demand. Mordor Intelligence estimates this factor exerts a -0.9% drag on turbine market CAGR.

▸ ESG-driven capital flight from fossil generation

The progressive withdrawal of multilateral development banks, export credit agencies, and commercial lenders from coal-fired power project finance has constrained the new-build pipeline in countries that lack domestic financing capacity. This "financing bottleneck" is particularly acute in sub-Saharan Africa and parts of South Asia, where otherwise viable projects are unable to reach financial close.

▸ Water stress and cooling constraints

Steam turbines are fundamentally dependent on cooling water availability. In water-stressed regions—including the U.S. Southwest, North China Plain, the Middle East, and Southern Africa—regulatory restrictions on once-through cooling and evaporative cooling towers are adding capital costs and operational constraints to thermal power plants, reducing their competitiveness against water-independent renewable generation.

▸ Extended EPC execution timelines

Large thermal power projects in India, Indonesia, and Brazil have experienced average schedule overruns of 12-18 months, driven by land acquisition delays, supply chain disruptions, and permitting bottlenecks. These delays compress the effective CAGR of turbine demand by pushing order-to-revenue conversion into later years.

10. Strategic Outlook & Key Takeaways

The steam turbine market in 2026 presents a complex investment thesis—one that defies simple "growth" or "decline" narratives. Several observations merit emphasis for industry participants, investors, and policymakers:

1. The market is larger and more durable than energy transition narratives suggest.

At USD 18-20 billion, the steam turbine OEM market is comparable in size to the global wind turbine market (ex-China) and substantially larger than the CSP or marine energy markets combined. The aftermarket adds another USD 12.5 billion. This is not a sunset industry; it is a mature, cash-generative industry undergoing geographic and technological rebalancing.

2. Regional divergence is the defining characteristic of this market.

Investors and strategists should resist the temptation to extrapolate European and North American coal retirement trends to the global market. In India, Southeast Asia, the Middle East, and parts of Africa, thermal power capacity is expanding, not contracting. A regional lens is essential for accurate forecasting.

3. The aftermarket is where value is concentrating.

With the aftermarket growing at 4.22% CAGR versus 2.5-3.5% for OEM equipment, the services and digitalization segments are attracting disproportionate R&D investment and generating the highest margins in the turbine value chain. OEMs that fail to build credible digital service offerings will find themselves competing on price alone—an unwinnable position in a capital-intensive industry.

4. Hydrogen readiness is a strategic option, not a near-term revenue driver.

OEMs are correct to invest in hydrogen co-firing and 100% hydrogen combustion technology, but investors should calibrate expectations: hydrogen-fired turbines will not contribute materially to turbine OEM revenue before 2032-2035. The near-term value of hydrogen capability is as a risk mitigation tool—enabling gas-fired power plant investments to proceed with a credible decarbonization pathway.

5. Geopolitical fragmentation is reshaping supply chains.

The global turbine supply chain is bifurcating along geopolitical lines, with Western OEMs (Siemens Energy, GE Vernova, Ansaldo Energia) increasingly concentrated in NATO-aligned markets and Asian OEMs (MHI, Toshiba, Doosan, BHEL) dominating non-aligned and Asian markets. This fragmentation reduces head-to-head competition in individual markets but increases systemic risk for OEMs with concentrated geographic exposure.

6. The data center demand vector is real and underappreciated.

The emergence of hyperscale data centers as a demand category for firm, dispatchable power is creating a new customer class for steam turbines—one that values speed of deployment and reliability above fuel cost optimization. Early-mover OEMs in this space have an opportunity to establish multi-decade service relationships with the world's largest and most capital-rich technology companies.

【 Closing Perspective 】

The steam turbine is perhaps the ultimate "boring but essential" industrial technology. It does not capture headlines like solar panels or electric vehicles. It does not inspire TED Talks. Yet it remains the workhorse of global electricity generation, converting thermal energy into rotational motion at a scale—and with a reliability—that no other technology has matched. The market's outlook is not one of explosive growth, but of managed transformation: declining in some geographies, expanding in others; shifting from equipment sales to services; and quietly incorporating digital, additive, and hydrogen technologies that will define its relevance in the decades ahead. For those who understand its rhythms, the steam turbine market offers something increasingly rare in the energy sector: durable, predictable value creation with a clearly visible decade-long demand trajectory.

Disclaimer: This report draws on publicly available data from Grand View Research, Mordor Intelligence, Arizton, DataHorizzon Research, Global Market Insights, The Business Research Company, the International Energy Agency (IEA), Global Energy Monitor, the World Nuclear Association, the IAEA PRIS database, and publicly filed company disclosures. Market size estimates, growth rates, and market share figures are derived from these sources, whose methodologies and statistical scopes differ. Readers should consult original source publications for detailed methodology descriptions. This report represents independent analysis and does not constitute investment advice.