1. Introduction: Why Voltage Transformers Matter in the New Grid Cycle

Voltage transformers are small compared with power transformers, GIS bays or HV switchgear in project value, but they are essential components in nearly every substation, switchgear panel, feeder protection system, revenue metering point and grid synchronisation scheme. Their opportunity is therefore not best measured by a standalone commercial market-size number. It is better understood through the volume of substations, transmission corridors, renewable interconnections, industrial electrification projects and digital grid upgrades that require reliable voltage measurement and isolation.

The next market cycle is being shaped by a mismatch between generation build-out and grid capacity. The IEA reports that more than 2,500 GW of renewable, storage and large-load projects are currently stalled in grid connection queues worldwide, while annual grid investment must rise by roughly 50% by 2030 from today's USD 400 billion level. For voltage transformer suppliers, this means demand will be distributed across new transmission substations, MV distribution automation, renewable collector substations, data-center interconnection, industrial power quality systems, and retrofit programs for ageing grids.

2. Core Conclusions

- The strongest opportunity is not generic component export, but approved-vendor participation in grid, substation and switchgear projects where voltage transformers are bundled with protection relays, metering panels, GIS/switchgear packages or EPC delivery.

- India is the highest-priority emerging market because its transmission plan combines renewable integration, high-voltage substation growth and large transformation capacity additions. Suppliers must, however, manage utility qualification, domestic competition and tender documentation requirements.

- Europe and North America offer high-value opportunities for digital substations, replacement programs, grid resilience and high-accuracy metering, but entry barriers are higher due to certification, product liability, cybersecurity and utility qualification cycles.

- The Middle East provides attractive project-driven demand in utility substations, solar and grid interconnection projects. The best route is usually EPC partnership, approved local agents and selective localisation rather than pure spot export.

- Southeast Asia, Latin America and Africa are more fragmented but should not be ignored. They favour rugged MV products, spares, retrofit kits, training and compact substation packages rather than only high-end digital LPIT systems.

- Product competitiveness is shifting from price and insulation design toward type-test credibility, accuracy stability, partial-discharge performance, seismic and climatic qualification, digital output compatibility and after-sales response.

- For the next three years, a practical supplier strategy is to combine MV switchgear-OEM channels, utility prequalification, EPC consortium partnerships and a gradually built service/calibration network in selected target regions.

3. Methodology and Data Boundaries

There is no single authoritative public dataset that consistently reports global sales of voltage transformers by voltage level, insulation type, utility application and country. Many commercial market-size figures also mix current transformers, voltage transformers, electronic instrument transformers and sensors. This report therefore does not rely on unverified market-size claims. Instead, it uses four verifiable demand proxies:

- Grid and transmission investment requirements from the IEA and public infrastructure programs.

- National or regional grid expansion plans, including EU, Indian, US and ASEAN policy signals.

- Application-level demand from substations, switchgear, renewable interconnections, protection and metering upgrades.

- Standards and certification requirements that shape procurement eligibility and product positioning.

Opportunity scores in this report are strategic ratings based on demand visibility, project pipeline quality, entry barriers, payment risk, local competition, certification burden and supplier-fit potential. They are not presented as precise market-share statistics.

4. Global Market Background: Grid Build-Out Creates the Demand Base

Voltage transformers follow grid investment. Three global demand drivers are especially important:

- Grid connection bottlenecks: IEA Electricity 2026 states that more than 2,500 GW of renewable, storage and large-load projects are waiting in grid queues worldwide. Every interconnection project that progresses into substation work requires voltage measurement, protection and metering interfaces.

- Rising grid investment: the same IEA analysis indicates that annual grid investment needs to increase by about 50% from the current USD 400 billion level by 2030. Older IEA grid work also noted that global grid investment would need to rise to over USD 600 billion per year by 2030 under national climate targets.

- Transmission supply-chain pressure: IEA analysis of transmission investment reports that global power transmission investment reached about USD 140 billion in 2023 and would need to exceed USD 200 billion annually by the mid-2030s under current policy settings, and USD 250-300 billion under full-transition scenarios.

For instrument transformer suppliers, the important conclusion is that demand growth will not be evenly distributed. New-build HV substations, grid uprating, distribution automation and digital substation programs create different product requirements. Suppliers must segment by application rather than treating voltage transformers as one generic SKU.

5. Regional Market Opportunity Analysis

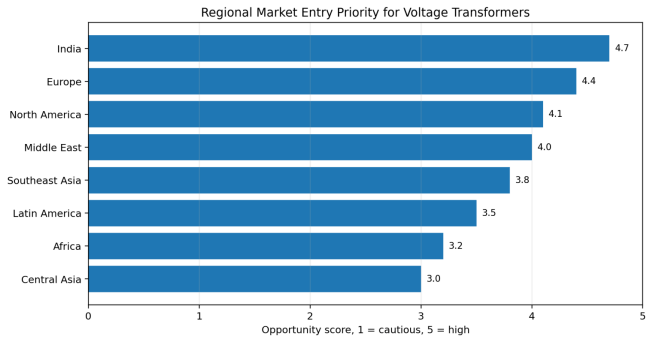

Figure 1. Regional opportunity score based on demand visibility, policy support, entry barriers and supplier-fit potential.

|

Region |

Demand logic |

Suitable offerings |

Entry mode |

Key barriers |

Opportunity |

|

India |

Large transmission plan, renewable integration, substations above 220 kV, switchgear growth and industrial electrification. |

MV indoor VTs, outdoor HV VTs/CVTs, GIS modules, test services, EPC packages. |

Utility prequalification, OEM supply to switchgear makers, EPC partnership, local service. |

Tender qualification, domestic competition, type-test proof, price pressure. |

High |

|

Europe |

Aging distribution grids, cross-border capacity, renewable integration, digitalisation and grid resilience. |

High-accuracy VTs, LPVT, digital substation sensors, retrofit and calibration services. |

Approved distributor, system integrator, panel OEM, selective local stock/service. |

CE/IEC compliance, utility approval, product liability, cybersecurity expectations. |

High |

|

North America |

Grid resilience, data centers, interconnection queues, T&D modernization and replacement of aged assets. |

IEEE/ANSI-compliant VTs, station-class CVTs, MV switchgear VTs, calibration and spares. |

UL/CSA-aligned product routes, local representative, utility qualification, EPC alliances. |

IEEE C57.13 requirements, NRTL testing, Buy America and utility vendor cycles. |

High-Medium |

|

Middle East |

Solar, grid interconnections, new substations, industrial cities and desalination/petrochemical loads. |

Outdoor HV/CVTs, GIS VTs, MV panels, harsh-climate designs, EPC packages. |

EPC partnership, local agent, utility-approved vendor list, project-specific localisation. |

Local agent dependence, project payment terms, climate testing, local content. |

High-Medium |

|

Southeast Asia |

Renewable target upgrades, grid strengthening, industrial parks, islands and cross-border power trade. |

MV VTs, compact substation parts, spares, protection packages, training. |

Distributor + panel OEM + EPC package, with country-specific utility registration. |

Fragmented standards, customs, project delays, country-by-country qualification. |

Medium-High |

|

Latin America |

Renewable buildout, mining loads, transmission corridors and substation renewal. |

Outdoor VTs/CVTs, MV VTs for mines and utilities, retrofit packages. |

EPC partnership and mining/utility channels, selective regional warehouse. |

Currency volatility, payment risk, import procedures, local competition. |

Medium |

|

Africa |

Access expansion, regional interconnectors, donor-funded substations and grid resilience. |

Rugged MV VTs, spares, compact substation packages, training and maintenance kits. |

Development-bank/EPC projects, distributor and after-sales partner. |

Payment risk, logistics, technical losses, procurement transparency. |

Selective |

|

Central Asia |

Grid renewal, mining and industrial electrification, interconnections and aging substations. |

MV/HV VTs, spares, retrofit kits, substation packages. |

Local technical partner, EPC route, state utility qualification. |

Language, certification legacy, payment and geopolitical risk. |

Selective |

6. Selected Demand Signals from Public Policy and Infrastructure Plans

|

Signal |

Implication for voltage transformers |

Source / data point |

|

Global grid investment gap |

More substations, feeder monitoring, metering and protection points as grid investment rises. |

IEA Electricity 2026: annual grid investment must rise ~50% from USD 400 billion by 2030; >2,500 GW in queues. |

|

EU Grid Action Plan |

High-value replacement and digitalisation opportunities, especially for aged distribution grids and cross-border capacity. |

European Commission: EU electricity consumption expected to rise ~60% by 2030; 40% of distribution grids over 40 years old; EUR 584 billion investment needed. |

|

India National Electricity Plan - Transmission |

Large substation and high-voltage system pipeline creates recurring demand for VTs, CVTs and testing services. |

NEP discussion: >191,000 circuit km transmission lines, 1,270 GVA transformation capacity, INR 9.15 lakh crore investment by 2032. |

|

US GRIP program |

Opportunities in grid resilience, flexibility and transmission/distribution modernization, but qualification is demanding. |

DOE: USD 10.5 billion GRIP program for grid flexibility and resilience. |

|

ASEAN energy action plan |

Renewable expansion requires grid strengthening, MV substations and interconnection equipment. |

Reuters: ASEAN endorsed 45% renewable electricity capacity share by 2030 under the 2026-2030 plan. |

7. Product and Supply Chain Opportunities

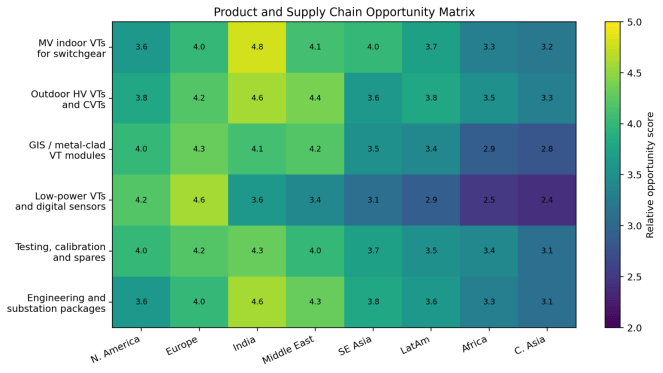

Figure 2. Opportunity scores by product segment and region. Scores are strategic ratings, not market-share statistics.

Voltage transformer suppliers should divide the opportunity into product families rather than pushing one universal catalogue. The key commercial distinction is between recurring MV switchgear demand and project-specific HV substation demand.

|

Segment |

Opportunity logic |

Best-fit customers |

Supplier capability required |

|

MV indoor voltage transformers |

High-volume demand through switchgear, industrial panels, feeder protection and metering. |

Switchgear OEMs, panel builders, utilities, industrial EPCs. |

Resin casting quality, partial-discharge control, accuracy stability, short lead times, documentation in local language. |

|

Outdoor HV voltage transformers and CVTs |

Directly linked to transmission substations, line bays, renewable interconnections and grid expansion. |

Utilities, substation EPCs, transmission owners. |

Type-test record, seismic/climatic qualification, porcelain/composite insulation options, field service. |

|

GIS-integrated voltage transformer modules |

Higher-value entry into compact substations, urban grids and high-reliability infrastructure. |

GIS OEMs, utility EPCs, metro/rail power projects. |

Mechanical integration, interface drawings, strict QA, confidentiality and OEM co-development ability. |

|

Low-power voltage transformers / digital sensors |

Growth in digital substations, distribution automation and IEC 61850 architectures. |

Digital substation integrators, protection relay vendors, advanced utilities. |

IEC 61869-6/11 understanding, merging unit compatibility, cybersecurity-aware documentation. |

|

Testing, calibration and spares |

Lower entry barrier and good route to build customer trust before full equipment supply. |

Utilities, O&M contractors, industrial plants, labs. |

Calibration traceability, quick response, replacement burden calculation, warranty management. |

|

Engineering packages |

Transforms the supplier from component seller into project participant. |

EPCs, developers, utilities and industrial customers. |

Protection coordination knowledge, specification review, tender compliance and local partner management. |

8. Project-Based Delivery Pathways

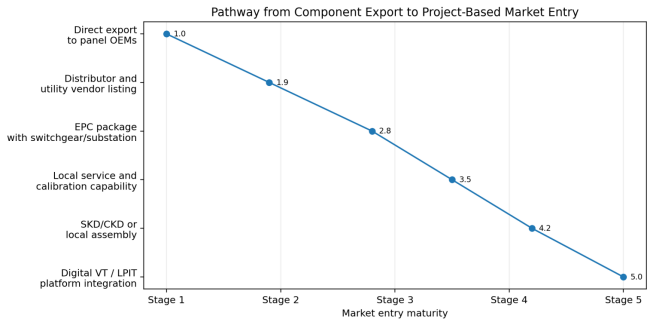

Figure 3. A staged pathway helps suppliers move from simple export to project-based international expansion.

A voltage transformer supplier usually cannot scale internationally through isolated spot orders alone. The market is governed by approved-vendor lists, protection engineering trust and long-cycle utility procurement. A staged path is therefore recommended:

- Start with MV switchgear OEMs and panel builders in target markets. This route generates reference projects, recurring demand and documentation feedback.

- Build distributor and utility-vendor qualification in one or two priority countries rather than spreading resources across too many jurisdictions.

- Offer voltage transformers as part of substation or renewable interconnection packages with EPC contractors, including documentation, testing and spare-parts planning.

- Create local service capability for inspection, replacements, burden checks and warranty response. This is often more persuasive than a small local assembly claim.

- For high-volume countries, evaluate SKD/CKD assembly or local testing capability to improve tender eligibility, delivery speed and after-sales trust.

- For mature markets, develop LPVT/digital sensor interfaces with relay and automation partners instead of competing only on conventional inductive VT price.

|

Entry model |

Best use case |

Advantages |

Weaknesses / prerequisites |

|

Direct export |

Small MV orders, replacement VTs, non-strategic industrial projects. |

Fast, low fixed cost, useful for market testing. |

Weak for utilities; limited ability to handle warranty and qualification. |

|

Local distributor |

Fragmented MV and industrial markets. |

Local language, customer access, customs and stock support. |

Margin sharing; distributor may lack technical depth. |

|

OEM supply |

Switchgear and panel manufacturers. |

Recurring demand, product standardization, earlier specification access. |

Requires strict quality consistency and price discipline. |

|

EPC partnership |

Substations, renewable plants, industrial power systems. |

Higher project visibility and ability to bundle services. |

Long tender cycles, payment risk and documentation burden. |

|

Utility prequalification |

Transmission and distribution utilities. |

Creates long-term customer access and credibility. |

Slow, expensive and dependent on type-test references. |

|

Local assembly/service |

India, Middle East, North America or large Southeast Asian markets. |

Improves tender fit, response time and localisation narrative. |

Needs volume, partner control and quality-system transfer. |

9. Standards, Certification and Localization Requirements

Voltage transformers are specification-driven products. International expansion requires more than matching nominal voltage and ratio. Buyers care about insulation coordination, burden, thermal rating, accuracy class, frequency, transient response, seismic/climatic performance, type-test evidence and compatibility with protection relays or metering systems.

|

Standard / requirement |

Where it matters |

Commercial implication |

|

IEC 61869 series |

Most IEC-oriented markets including Europe, Middle East, India, Southeast Asia, Africa and many Latin American utilities. |

Core family for instrument transformers. IEC 61869-3 covers inductive voltage transformers; IEC 61869-6 and related parts cover low-power instrument transformer requirements. |

|

IEEE C57.13 |

United States and many ANSI/IEEE-influenced projects. |

Important for accuracy classes, burdens and requirements for instrument transformers. US buyers may require NRTL/UL/CSA alignment and utility-specific tests. |

|

IEC 61850 compatibility |

Digital substations and advanced utility automation. |

Conventional VTs may still be accepted, but LPVT/digital sensor products need interface strategy with merging units, relays and station bus design. |

|

CE / UKCA / local conformity |

Europe, UK and related markets. |

Needed for legally placed equipment and can influence documentation, risk assessment and declaration requirements. |

|

Climatic and environmental tests |

Middle East, coastal renewables, tropical Southeast Asia, mining and desert projects. |

Humidity, temperature, salt mist, UV and pollution performance can differentiate suppliers. |

|

Local content and origin rules |

India, US public projects, Middle East national programs and some Latin American tenders. |

Can shift strategy toward local service, testing, assembly or partnership even when full manufacturing localisation is not economical. |

10. Regional Strategic Notes

India

India should be treated as a priority market for volume and project visibility. The most attractive openings are utility substations, renewable pooling substations, green hydrogen and ammonia hubs, rail/metro power systems, industrial parks and MV switchgear supply. Entry should start with product homologation, CEA/BIS-aware documentation, local testing support and partnerships with switchgear OEMs and substation EPC contractors. Pure price competition is risky because domestic suppliers are strong and utility tenders require extensive compliance evidence.

Europe

Europe is less about volume-only export and more about replacement, grid digitalisation and high-reliability projects. The EU grid agenda emphasises digitalised, decentralised and flexible networks, while distribution-grid ageing creates retrofit opportunities. Suppliers should position high-accuracy products, LPVT/digital interfaces, testing services and OEM cooperation. Product liability, technical documentation, CE conformity and utility references are decisive.

North America

North America has strong demand drivers from grid resilience, interconnection queues, data centers, extreme-weather hardening and ageing infrastructure. However, the market is difficult for new entrants. IEEE/ANSI compliance, utility approval, local representation, insurance, NRTL testing and spare-part support are required. A realistic route is to serve panel OEMs, private industrial substations, renewable EPCs and selected utilities before attempting broad public-utility penetration.

Middle East

The Middle East is project-rich and EPC-driven. Solar, transmission, desalination, industrial cities and data-center loads create substation demand. Voltage transformer suppliers should offer harsh-climate designs, quick documentation, Arabic/English support, local agents and spare-part availability. Long-term success depends on approved-vendor status with utilities and close relationships with EPC contractors.

Southeast Asia

Southeast Asia is fragmented but attractive due to renewable targets, industrial parks, island grids and cross-border power trade. The best products are MV switchgear VTs, compact substation equipment, spares and rugged products for humidity and coastal environments. Suppliers should use country-specific distributors and panel OEM channels, rather than assuming one ASEAN-wide route.

Latin America

Latin America combines renewable buildout, mining electrification and transmission upgrades. The opportunity is strongest where mining, wind/solar and utility transmission converge. Payment terms, currency exposure and local procurement procedures require careful screening. Regional warehousing can reduce replacement downtime and improve credibility.

Africa

Africa offers real long-term demand but the near-term route should be selective. Donor-funded grid projects, regional interconnectors, mini-grid-to-grid transitions and utility substations can support demand for rugged MV VTs, spares and compact substation packages. The main risks are payment, logistics and procurement transparency. EPC and development-finance-backed projects are preferable.

Central Asia

Central Asia is a replacement and industrial electrification opportunity rather than a broad high-volume market. Grid renewal, mining and interconnections create demand for MV/HV VTs and spares. Entry requires local technical partners, Russian or local-language documentation and strong project risk controls.

11. Risk Analysis and Mitigation

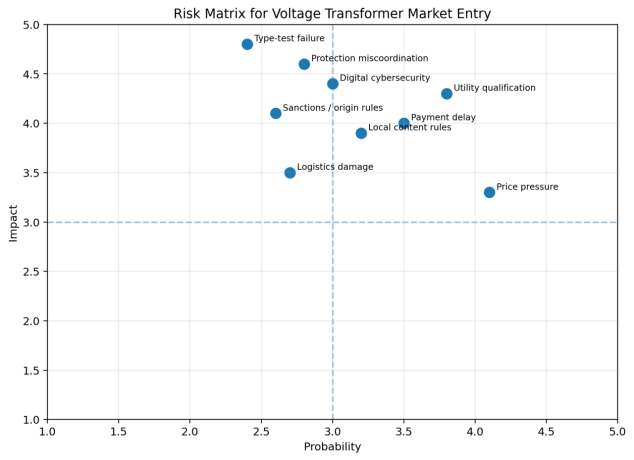

Figure 4. The most damaging risks are qualification failure, type-test or quality problems and miscoordination with protection/metering systems.

|

Risk |

Why it matters for voltage transformers |

Mitigation |

|

Utility qualification failure |

A supplier can be technically capable but still excluded from tenders without utility approval and reference lists. |

Select 2-3 priority utilities per region, prepare type-test dossiers and obtain references through OEM/EPC channels. |

|

Type-test or quality failure |

Partial discharge, insulation coordination or accuracy instability can cause project rejection and reputational damage. |

Use accredited labs, maintain batch QA, keep test records traceable and align designs with target standards. |

|

Protection and metering mismatch |

Wrong burden, ratio, accuracy class or connection scheme can affect relays and revenue metering. |

Review specifications with protection engineers; provide burden and wiring guidance. |

|

Local-content and origin rules |

Public projects may prefer or require domestic content, assembly or local service. |

Use local service, calibration or assembly partnerships where economically justified. |

|

Payment and currency risk |

Project payment delays can erase margin on component orders. |

Use LC, credit insurance, milestone payments and EPC due diligence. |

|

Logistics and handling damage |

Outdoor VTs and CVTs can suffer insulation or oil/gas-seal damage during transport. |

Improve packaging, shock indicators, local inspection and insurance terms. |

|

Price volatility and margin pressure |

Commodity and insulation-material costs can move faster than tender validity periods. |

Use escalation clauses for long tenders and define validity windows. |

|

Digital cybersecurity and data interface risk |

LPVT/digital solutions used in digital substations interact with station automation systems. |

Document interface security, firmware management and IEC 61850/merging unit integration clearly. |

|

Geopolitical and sanctions compliance |

Power grid equipment may be affected by origin restrictions or sanctions in sensitive countries. |

Screen customers, end use and counterparties; manage origin documentation. |

12. Recommended Three-Year Market Entry Roadmap

|

Timeframe |

Main objective |

Priority actions |

Success indicators |

|

0-6 months |

Clarify product-market fit. |

Separate IEC and IEEE product lines; map type tests; choose 3 priority regions; build English technical data sheets. |

Target-country product matrix; standard-compliant documentation; shortlist of OEM/EPC partners. |

|

6-18 months |

Build channel and references. |

Sign regional distributors; supply pilot orders to panel OEMs; join EPC bid packages; create spare-part and warranty process. |

Reference projects; first utility/OEM approvals; repeat orders from switchgear customers. |

|

18-36 months |

Move toward project-based entry. |

Apply for utility prequalification; open local service/calibration support; evaluate assembly/testing partnerships in India or Middle East. |

Approved-vendor status; EPC package wins; service revenue; reduced warranty response time. |

|

36 months+ |

Differentiate beyond conventional VTs. |

Develop LPVT/digital sensor partnerships, IEC 61850 integration references and project lifecycle services. |

Digital substation references; higher-margin product mix; long-term service contracts. |

13. Conclusion

Voltage transformers are a project-linked market. The best opportunities arise where grid investment, renewable interconnection, substation construction and protection/metering upgrades overlap. India, Europe and North America offer the strongest strategic demand signals, while the Middle East and Southeast Asia provide attractive project-based channels for suppliers that can work through EPCs, panel OEMs and local representatives.

The central challenge is not manufacturing a voltage transformer at a competitive cost. It is proving long-term accuracy, insulation reliability, standards compliance and field service capability inside procurement systems that are conservative by design. Suppliers that combine conventional MV/HV product reliability with credible type-test documentation, regional service capability and digital-substation readiness will be better positioned than suppliers that compete only on price.

14. Data Sources and Methodology Note

- International Energy Agency (IEA), Electricity 2026, Grids chapter.

- International Energy Agency (IEA), Electricity Grids and Secure Energy Transitions, executive summary.

- International Energy Agency (IEA), Building the Future Transmission Grid, executive summary.

- European Commission, European Grids and Grid Action Plan page.

- India National Electricity Plan - Transmission public summaries and CEA/PIB-referenced plan data.

- US Department of Energy / Office of Electricity, Grid Resilience and Innovation Partnerships (GRIP) Program Projects.

- Reuters, ASEAN 2026-2030 Plan of Action for Energy Cooperation renewable electricity capacity target.

- IEC 61869 series public previews and standard descriptions; IEEE C57.13 public standard description.

- Public utility, EPC and standards documentation available as of July 2026.

Methodology note: figures in this report are used for strategic comparison and market-entry planning. Grid investment, transmission capacity, renewable targets and utility procurement plans differ across sources because of reporting periods, geographic coverage, commissioning dates, nominal versus real values and project scope. Opportunity scores are qualitative ratings based on publicly available evidence and should not replace project-specific due diligence, local legal review or utility tender analysis.