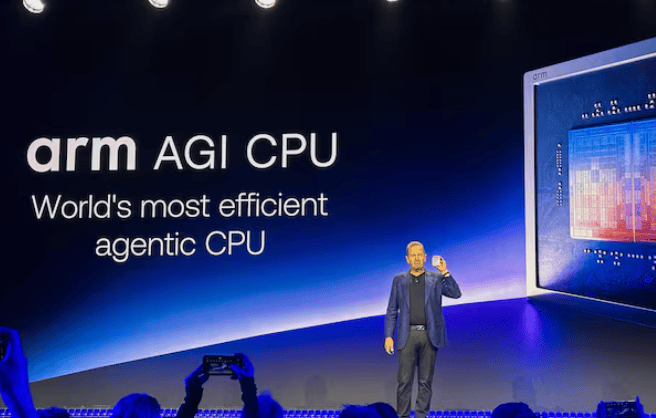

en.Wedoany.com Reported - Recently, Rene Haas, CEO of UK-based chip architecture company Arm, stated that driven by rising demand for artificial intelligence infrastructure, the company's self-developed chip business may achieve its $15 billion annual revenue target earlier than originally expected. Arm's Arm AGI CPU, designed for AI data centers, is gaining adoption from more customers, and data center processors have become a key product line as the company extends from chip IP licensing to selling self-developed chips.

For a long time, Arm has been positioned upstream in the global semiconductor industry chain, participating in the smartphone, server, automotive electronics, and IoT chip markets by licensing CPU architectures and core designs. With the launch of the AGI CPU, its business boundaries have begun to extend from "providing design blueprints" to "delivering chip products ready for data centers." As AI models shift from the training phase to inference and agent applications, demand for central processing units in data centers has undergone new changes: a large number of agent tasks require CPUs to handle scheduling, data flow, memory access, and multi-tasking concurrency. While GPUs remain the core of accelerated computing, the role of CPUs in inference clusters, agent execution, and cloud service orchestration has been re-emphasized. By linking the $15 billion target to AGI CPU demand, Arm highlights that competition in AI infrastructure is no longer focused solely on GPUs; data center processors, memory bandwidth, energy consumption control, and rack-level deployment efficiency are becoming new growth markets.

The AGI CPU can be configured with up to 136 Arm Neoverse V3 cores and has a thermal design power of 300 watts, targeting agentic AI and cloud data center workloads. The product has already established a cooperative foundation with customers like Meta, and the latest information as of June 2 shows that ByteDance and Oracle have also become Arm AGI CPU customers.

This carries strong signaling significance for Arm's revenue structure. The traditional IP licensing model typically relies on licensing fees and royalties, with revenue tied to customers' chip shipment schedules, offering high profit margins but limited revenue per project. In contrast, self-developed chip sales directly enter the data center hardware procurement chain, targeting cloud service providers, internet platforms, and enterprise AI infrastructure customers. If the AGI CPU can enter the data center systems of major customers like Meta, Oracle, and ByteDance, Arm will gain a hardware revenue channel closer to that of chip manufacturers like Nvidia, AMD, and Intel, while retaining its existing advantages in architecture ecosystem, software compatibility, and power efficiency. Haas's mention that demand is stronger than expected just a few weeks ago also indicates that cloud providers are seeking more processor combinations for AI inference and agent operations to alleviate cost pressures from GPU concentration, rising energy consumption, and reliance on a single architecture. For the industry chain, whether Arm can transition the AGI CPU from early customer validation to large-scale procurement will determine whether its self-developed chip strategy can truly change the company's valuation logic.

Arm also faces practical constraints such as production capacity, packaging, memory, and customer adaptation. Once data center processors enter mass production, they must not only rely on advanced manufacturing resources like TSMC but also coordinate memory supply, server manufacturer adaptation, software stack migration, and cloud platform deployment cycles. Procurement decisions for AI infrastructure typically involve entire system configurations, rack power consumption, thermal design, and long-term operations and maintenance. For the AGI CPU to support the $15 billion annual revenue target, it needs to expand from single-chip performance to server ecosystem and customers' long-term deployment capabilities.

The signal released by Arm this time indicates that the AI infrastructure market is shifting from a single focus on accelerator chips to coordinated expansion across CPUs, GPUs, memory, networking, and system software. As data center processors regain growth space, Arm's self-developed chip strategy has entered a critical validation period, and its subsequent progress will directly impact the competitive structure of the global artificial intelligence chip market.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com