en.Wedoany.com Reported - WTI crude oil closed at $96.02 on June 3, 2026, and Brent crude at $97.81, as prices surged due to clashes between U.S. and Iranian forces. A conditional Israel-Lebanon ceasefire announced in early European trading on June 4 reversed the two benchmark oil prices, with Brent falling to $97.03 and WTI to $95.32, as the market viewed this agreement as a prerequisite for broader U.S.-Iran reconciliation.

Such price volatility itself masks a deeper physical issue. The closure of the Strait of Hormuz has reduced global daily supply by 11 million to 14 million barrels. U.S. commercial crude oil inventories fell by 8 million barrels to 433.7 million barrels, marking the sixth consecutive weekly decline, while the Strategic Petroleum Reserve (SPR) released another 8 million barrels over the same period. The U.S. government is tapping strategic reserves to keep oil prices below $100, but this intervention capacity has limits.

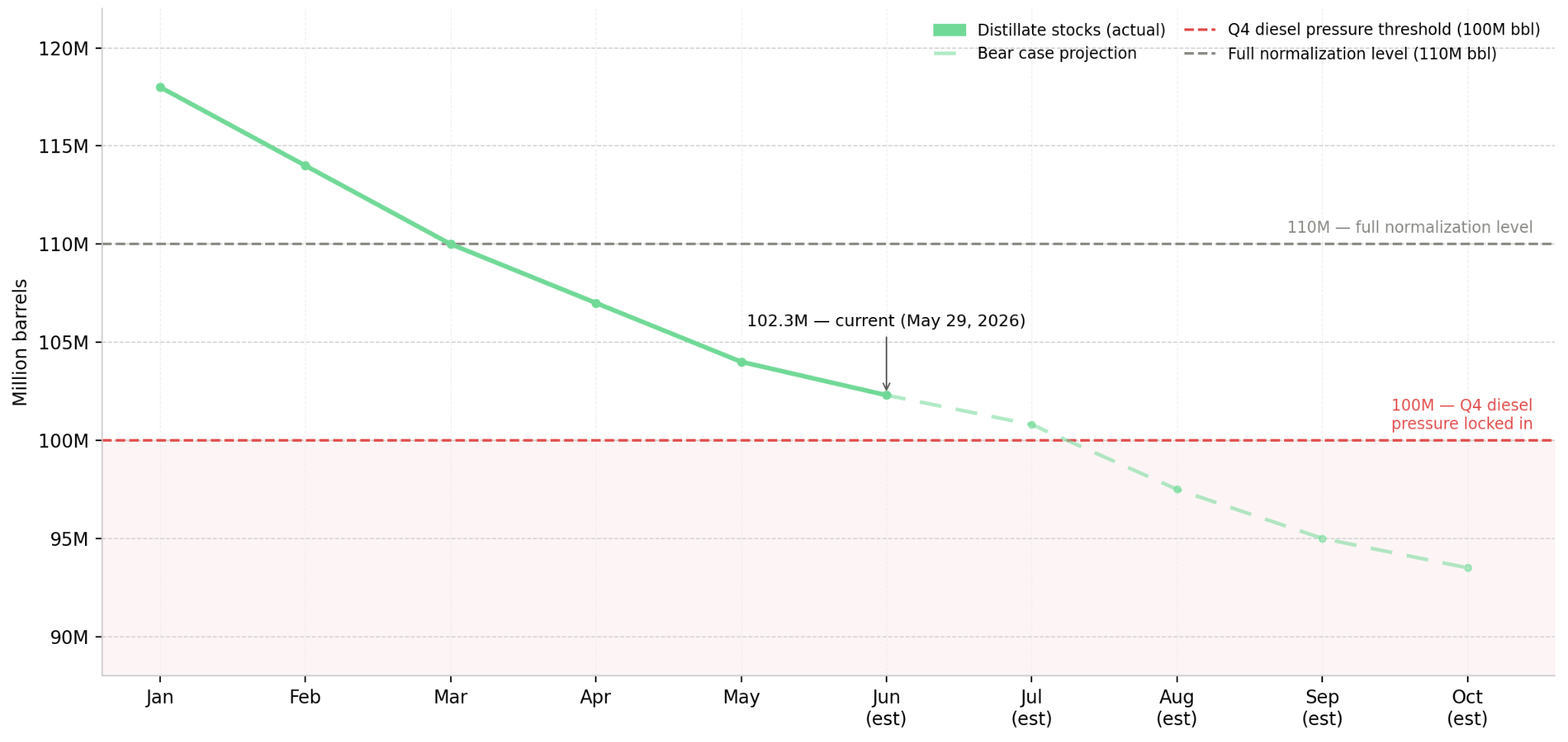

Economists at Macquarie Group assess that at the current drawdown rate, the market's period of ample supply can last approximately one to two months, after which physical supply is expected to tighten significantly if the Strait of Hormuz remains closed. Ritterbusch and Associates reinforced this timeline, noting that Trump has explicitly stated his intention to maintain the blockade until Labor Day on September 1, 2026, making short-term ceasefire negotiations largely irrelevant to the forward supply landscape. Distillate inventories stand at 102.3 million barrels, only 2.3 million barrels above the 2023 lows. Muenster of Breakthrough warns that inventories are trending toward particularly low levels in the fourth quarter, and even if a resolution in the Strait of Hormuz leads to lower crude oil prices, diesel prices may remain under pressure.

Energy exposure is not uniform. Holding positions in broad energy ETFs or upstream crude oil producers captures the binary risk of the Strait of Hormuz, with prices fluctuating with ceasefire headlines, but fails to isolate the distillate profit story. Regardless of crude oil settlement prices, the likelihood of rising freight and fuel costs compressing margins will persist through the fourth quarter.

The Israel-Lebanon ceasefire does not resolve the supply gap in the Strait of Hormuz. The key question is whether Macquarie Group's late-July buffer depletion point will arrive before confirmation of a Strait of Hormuz resolution. In the base case, if the Strait of Hormuz reopens in July 2026, Brent crude could fall below $90 for five consecutive trading days, with crude-related positions retreating from current levels, but distillate inventories would remain below 100 million barrels, keeping fourth-quarter diesel cost pressures persistent in transportation and manufacturing, independent of crude oil price fluctuations. In the bear case, if the Strait of Hormuz remains closed until Labor Day on September 1, 2026, maintaining Trump's explicit blockade timeline, Macquarie Group's supply surplus buffer depletes in late July, physical supply tightens significantly, and Robert Yawger of Mizuho Securities expects Brent crude to trade above $100, while distillate inventories would fall below 100 million barrels. Regardless of how crude oil prices resolve, unhedged transportation and industrial operators will face fourth-quarter diesel headwinds.

Distillate inventories below 100 million barrels confirm that fourth-quarter diesel pressure is structural. If an announcement regarding the Strait of Hormuz is made but Brent crude fails to stay below $90 for five consecutive trading days, it would be a false signal of relief.

Integrated refiners with heavier distillate structures will benefit from the divergence between diesel and crude, gaining from wider profit margins. Regardless of Brent crude settlement prices, unhedged transportation and industrial manufacturers will face fourth-quarter cost headwinds. Holding long upstream crude positions exposes investors to ceasefire binary risk; holding distillate-exposed refining or logistics positions faces the fourth-quarter inventory clock, a 6-to-10-week timeline that diplomatic outcomes cannot shorten. Muenster's fourth-quarter view only requires that distillate inventories fail to rebuild before fourth-quarter demand rises.

Oil prices remain above $95, supported by six consecutive weeks of crude inventory declines and ongoing SPR releases. As long as crude inventories continue to fall and a Strait of Hormuz agreement is not confirmed, crude-related positions benefit if distillate inventories stay above 100 million barrels. Once a U.S.-Iran agreement is confirmed and Brent crude remains below $90 for five consecutive trading days, the crude equity premium will reverse, but this reversal will not normalize diesel: distillate inventories must rebuild to above 110 million barrels to achieve full-cycle cost normalization, requiring 6 to 8 weeks of net inventory growth after reopening. Key monitoring data comes from the U.S. Energy Information Administration's (EIA) Weekly Petroleum Status Report, released every Wednesday. Crude inventories below 420 million barrels signal buffer depletion. Distillate inventories below 100 million barrels confirm fourth-quarter diesel structural pressure. If an announcement regarding the Strait of Hormuz is made but Brent crude fails to stay below $90 for five consecutive trading days, the distillate-related thesis remains unchanged.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com