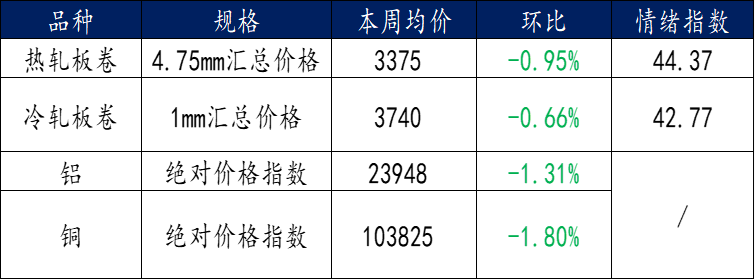

en.Wedoany.com Reported - According to Mysteel data, China's steel market experienced overall fluctuations last week. For hot-rolled coils, prices diverged across major cities. Shanghai prices fell by 20 yuan/ton week-on-week, Guangzhou dropped by 10 yuan/ton, while Tianjin rose by 20 yuan/ton. The national average price stood at 3,398 yuan/ton, down 14 yuan/ton from the previous week. As of June 12, the five-day average trading volume for hot-rolled coils reached 41,143 tons, down 3.57% week-on-week and 7.31% month-on-month. Market activity was primarily driven by rigid demand replenishment, with a low willingness for active stockpiling. While orders maintained a certain level of continuity, overall growth was limited, and there is a lack of clear growth drivers in the short term.

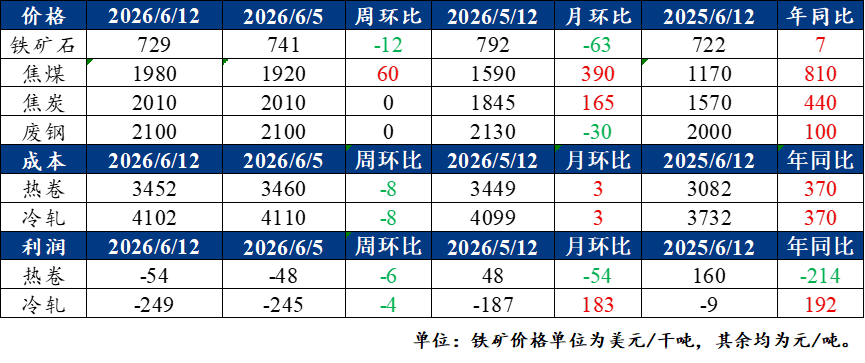

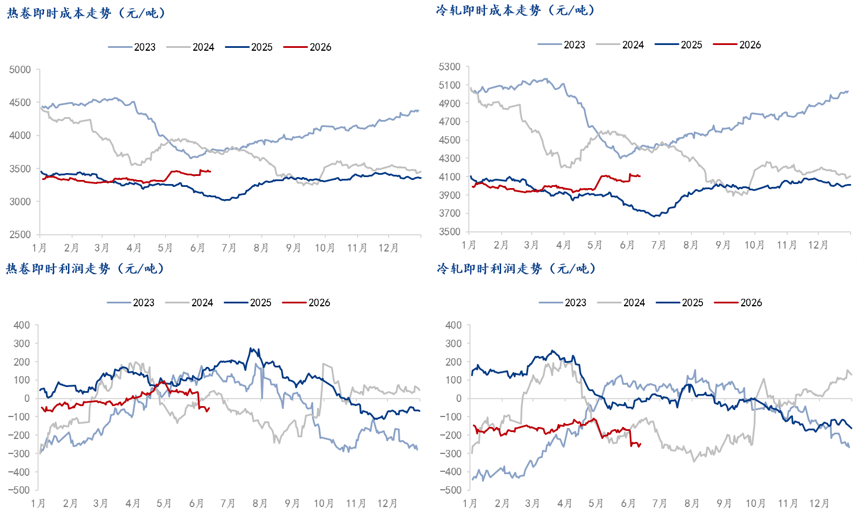

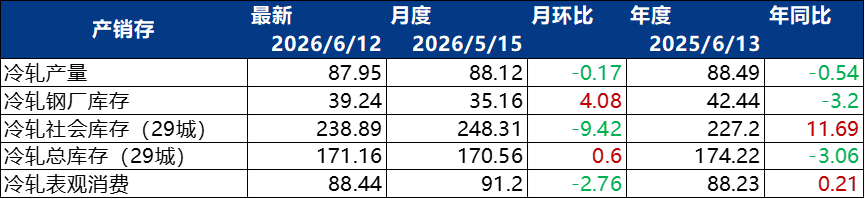

For cold-rolled coils, the average price of 1.0mm cold-rolled coil was 3,853 yuan/ton, down 12 yuan/ton week-on-week. In specific major markets, the price of 1.0mm Benxi Steel cold-rolled coil in Shanghai was 3,740 yuan/ton, 1.0mm Liuzhou Steel cold-rolled coil in Lecong was 3,780 yuan/ton, and 1.0mm Angang Tiantie cold-rolled coil in Tianjin was 3,680 yuan/ton, all down 10 yuan/ton week-on-week. The five-day average daily trading volume was 21,049 tons, up 1.9% from the previous week. In terms of costs and profits, due to the decline in iron ore prices, the costs for hot-rolled and cold-rolled coils decreased slightly, while spot profits for finished steel products contracted modestly.

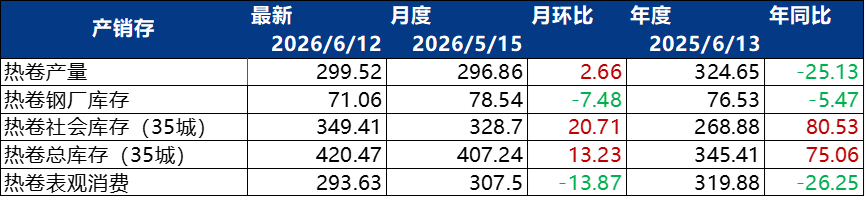

Regarding steel mill dynamics, according to Mysteel's full-sample survey of hot-rolled coils, the total impact volume for hot-rolled coils was 40,000 tons last week, and the actual total impact volume for this week is also 40,000 tons, with an estimated impact volume of 21,200 tons for next week. One steel mill in East China resumed production this week (statistical period from June 4 to June 10, 2026; next week from June 11 to June 17, 2026).

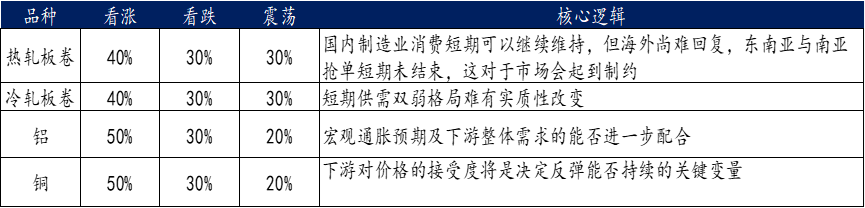

In the non-ferrous metals market, the aluminum market completed a phased bottoming out amid fluctuations. The recovery of overseas macro sentiment and the accelerated destocking of domestic social inventories provided bottom support for aluminum prices. Short-term downside support is solid, but upward momentum still requires cooperation from macro inflation expectations and downstream demand. The copper market showed a tug-of-war between macro sentiment and fundamentals. Spot premiums remained firm, but high prices suppressed downstream demand, leading to a price trajectory of initial decline followed by a rise and high-level fluctuations. The zinc market fluctuated weakly amid mixed factors. Supply-side maintenance and production cuts provided support, but weak consumption and pressure from macro sentiment limited the rebound potential. The nickel market trended lower under the combined pressure of macro headwinds and weak fundamentals, with both the LME and domestic SHFE markets declining. Massive visible inventory became a key resistance to price rebounds. Multiple institutions expect the main Shanghai nickel contract to continue fluctuating within a core range of 133,000 to 142,000 yuan/ton.

In terms of policy and industry hotspots, the steel industry is focusing on the following developments. The China Iron and Steel Association (CISA) held a national promotion meeting for the new capacity replacement measures in Kunming on June 11. The Raw Materials Department of the Ministry of Industry and Information Technology (MIIT) interpreted the replacement rules on-site: China's ironmaking and steelmaking will uniformly implement capacity reduction replacement at a ratio of 1.5:1, which can be relaxed to 1.25:1 for substantive mergers and acquisitions. Starting from 2028, the simple buying and selling of capacity indicators will be prohibited; capacity can only be transferred through mergers and acquisitions. CISA requires the entire industry to strictly adhere to the capacity red line and prohibit disguised capacity expansion through technological transformation or relocation. The Extreme Energy Efficiency Blast Furnace Hot Stove Low-Carbon Technology Exchange Meeting was held in Qingdao on June 8, focusing on energy-saving and carbon-reduction retrofits for long-process furnaces. Crude steel output control and industry self-discipline continue to be implemented, adhering to the target of reducing total crude steel output to 930 million tons in 2026.

In the non-ferrous metals industry, the "Implementation Regulations of the Mineral Resources Law" officially took effect on June 15, placing 25 categories of non-ferrous metals among 36 strategic minerals under the national-level control catalog, including copper, aluminum, lithium, cobalt, nickel, rare earths, tungsten, germanium, gallium, indium, antimony, and molybdenum. Approval authority has been centralized, with exploration and mining rights for strategic large and medium-sized mines now uniformly granted by the Ministry of Natural Resources. Local supporting measures for the "Non-Ferrous Metals Stable Growth Plan (2025-2026)" continue to be implemented, with multiple provinces working towards two hard targets: an average annual industrial added value growth rate of no less than 5% for the industry and total recycled metal production exceeding 20 million tons by 2026.

In the automotive industry, on June 13, 11 government departments issued the "Implementation Plan for Promoting the Large-Scale Application of New Energy Heavy Trucks," proposing to achieve a 40% penetration rate for new energy heavy trucks by 2030, with a total stock exceeding 1.6 million units. The electrification rate for short-haul transportation in the Beijing-Tianjin-Hebei region and the Fenwei Plain needs to exceed 80%. For supporting infrastructure, the plan proposes building 30,000 kilometers of zero-carbon freight corridors and deploying 3,000 heavy truck charging and swapping stations. On June 11, the MIIT and the State Administration for Market Regulation summoned certain automakers involved in low-price competition, requiring strict compliance with price compliance guidelines. On the same day, the 87th batch of the catalog of new energy vehicle models eligible for vehicle and vessel tax reductions was announced, including a total of 963 new energy vehicle models, comprising 802 pure electric, 123 plug-in hybrid, and 38 fuel cell models.

This article is compiled by Wedoany. All AI citations must indicate the source as "Wedoany". If there is any infringement or other issues, please notify us promptly, and we will modify or delete it accordingly. Email: news@wedoany.com