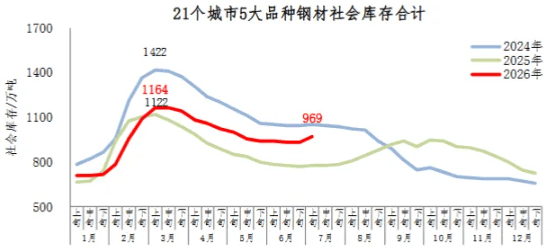

en.Wedoany.com Reported - According to monitoring data released by the Market Research Department of the China Iron and Steel Association, in early July 2026, the total social inventory of five major steel varieties in 21 cities stood at 9.69 million tons, an increase of 340,000 tons month-on-month, up 3.6%, with the inventory growth rate expanding compared to the previous period. Compared to the beginning of the year, inventory increased by 2.48 million tons, up 34.4%; year-on-year, it rose by 1.94 million tons, an increase of 25.0%. Overall, inventory levels are at a historical high for the same period, with continued pressure on market supply.

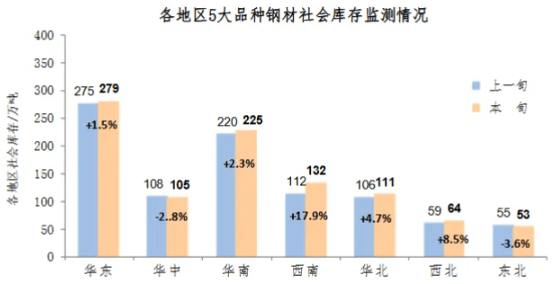

By region, steel social inventory in most of the seven major regions increased month-on-month, with only Central China and Northeast China seeing slight declines. Among them, Southwest China recorded the largest increase in both volume and percentage; Central China saw the largest decrease in volume; and Northeast China experienced the largest percentage decline.

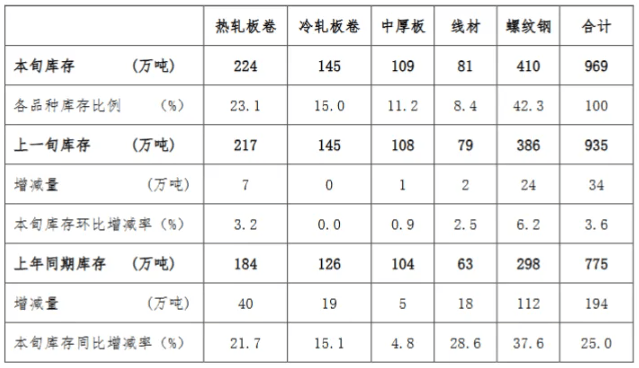

By variety, month-on-month social inventory of the five major steel varieties remained flat for cold-rolled coils, while all other varieties increased. Rebar was the variety with the largest increase in both volume and percentage. Specifically, rebar inventory stood at 4.1 million tons in early July, up 240,000 tons month-on-month, an increase of 6.2%, accounting for 42.3% of total social inventory. Hot-rolled coil inventory was 2.24 million tons, up 70,000 tons month-on-month, an increase of 3.2%. Cold-rolled coil inventory was 1.45 million tons, flat month-on-month. Medium plate inventory was 1.09 million tons, up 10,000 tons month-on-month, an increase of 0.9%. Wire rod inventory was 810,000 tons, up 20,000 tons month-on-month, an increase of 2.5%.

Year-on-year, inventory of all five varieties increased to varying degrees, with rebar being the variety with the largest increase in both volume and percentage. Rebar increased by 1.12 million tons year-on-year, up 37.6%; wire rod increased by 180,000 tons year-on-year, up 28.6%; hot-rolled coils increased by 400,000 tons year-on-year, up 21.7%; cold-rolled coils increased by 190,000 tons year-on-year, up 15.1%; and medium plates increased by 50,000 tons year-on-year, up 4.8%.

The continued rise in steel social inventory in early July reflects the basic market pattern of supply exceeding demand. With a year-on-year inventory increase of 25% and rebar inventory up nearly 40%, it indicates that demand recovery in the construction steel sector has fallen short of expectations. Currently, it is the traditional off-season for steel consumption, with persistent rainy weather in the south and high temperatures in the north suppressing terminal construction progress. Downstream procurement has slowed, and traders face increased pressure to offload inventory. The ongoing accumulation of inventory may further suppress steel price trends, with destocking expected to remain the main theme in the short term. In the later period, attention should be focused on the implementation of steel mill production cuts and maintenance plans, as well as marginal changes in terminal demand.