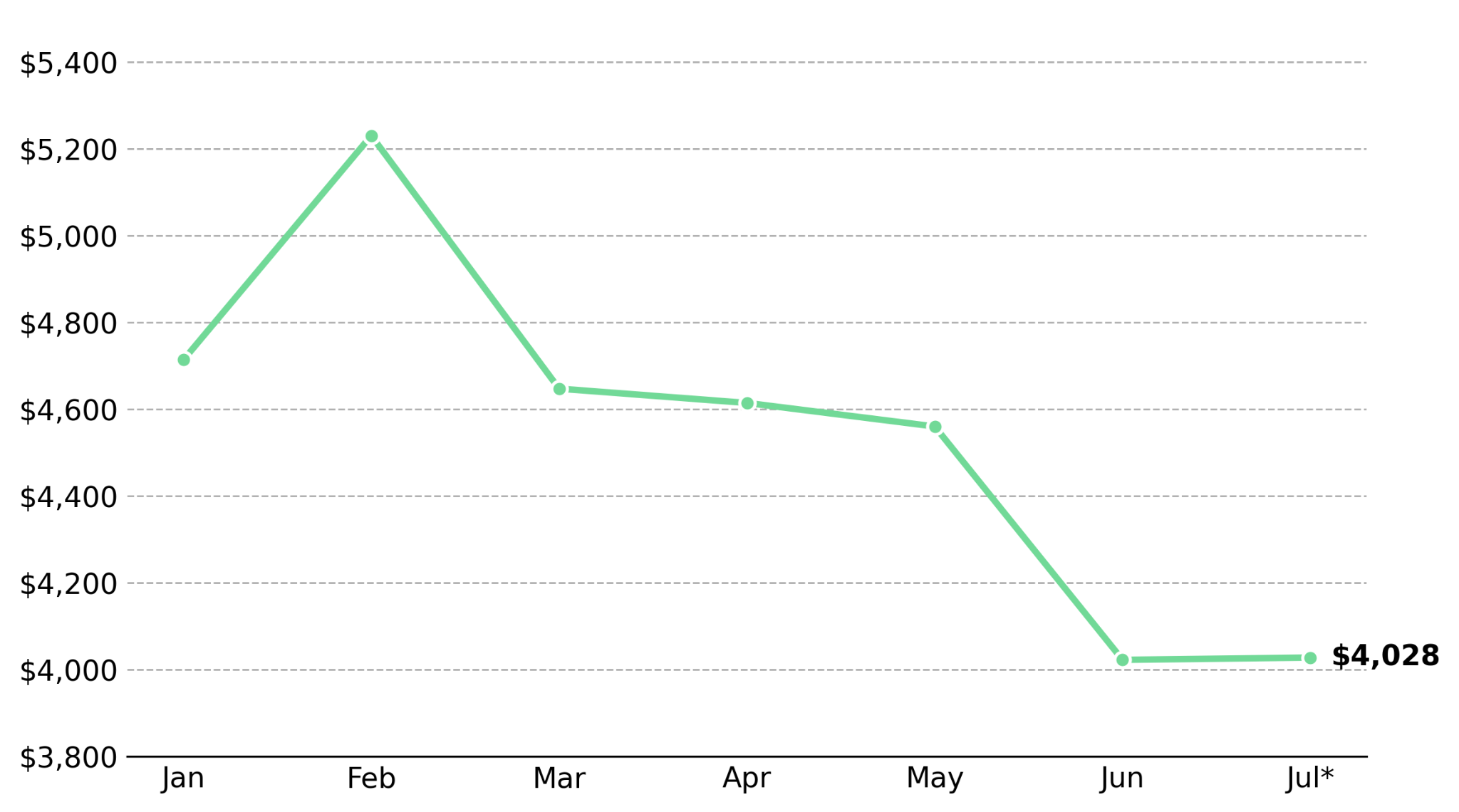

en.Wedoany.com Reported - On July 15, spot gold fell 0.6% to $4,028.13 per ounce, after hitting the World Gold Council's (WGC) second-half target of $4,100.49 per ounce the previous trading day. The June CPI data that drove this rally showed inflation slowing to 3.5% year-on-year and falling 0.4% month-on-month, the first monthly decline since April 2020. The August gold futures contract fell 0.9% that day, closing at $4,033.90 per ounce.

Kelvin Wong, Senior Market Analyst at OANDA, said that when oil prices are above $80 per barrel, market attention shifts from the moderate CPI data back to inflation risks, putting pressure on gold prices.

Analysis by the World Gold Council's Gold Return Attribution Model indicates that heightened geopolitical risks between the U.S. and Iran were the biggest driver of gold's performance in the first half of 2026. The naval blockade of the Strait of Hormuz has kept oil prices above $80 per barrel, fueling inflation expectations. Although the probability of a Fed rate hike in September fell from 76% to 58% after the June CPI data release, inflationary pressures from high oil prices persist.

The yield on the U.S. two-year Treasury note fell 9 basis points from a 16-month high, reflecting a decline in near-term interest rate expectations. Chris Turner, Global Head of Markets at ING, said high energy prices could support the U.S. dollar and keep the Fed's tightening expectations intact. Fed Chairman Kevin Warsh made it clear that the Fed will not tolerate persistently high inflation, limiting gold's upside after the moderate CPI data.

Juan Carlos Artigas, CEO of the Americas and Global Head of Research at the World Gold Council, said long-term buying from central banks, institutions, and consumers has supported gold prices near $4,000 per ounce at multiple points. Based on a spot price of $4,028 per ounce, the council outlined three scenarios in its second-half framework. The baseline scenario assumes the Fed will raise rates at least once by October, with simultaneous tightening by the Bank of England, Bank of Japan, and European Central Bank, and U.S. inflation near 3.9%, forecasting gold prices to remain between $3,895 and $4,305 per ounce this year. The bullish scenario requires a sharp global economic slowdown, pushing gold prices above $4,500 per ounce. The bearish scenario assumes gold prices stay below $4,000 per ounce with increased selling pressure, but historically, price declines of more than 10% tend to attract long-term buying back.

On July 15, spot gold traded at $4,028.13 per ounce, above the World Gold Council's demand threshold of $4,000 per ounce. The council's historical analysis shows that selling pressure increases when prices fall below this level, while buying from central banks and institutions has historically supported prices above it. For producers with all-in sustaining costs (AISC) below $3,000 per ounce, strong operating profits are achievable within the council's baseline scenario range ($3,895 to $4,305 per ounce). Operations with AISC near $3,500 per ounce will see profit margins narrow if gold prices fall below $4,000. Mines requiring gold prices above $4,100 per ounce to maintain returns on capital face greater downside risk in a persistently high-interest-rate environment.

The U.S. Producer Price Index (PPI), as the first inflation data following the June CPI, is expected to show whether rising energy costs are passing through to producer prices. A moderate reading would lower expectations for a September Fed rate hike and support gold prices; a strong reading would strengthen the case for another Fed rate hike and pressure gold prices. The PPI data, subsequent CPI data, and guidance from the July 28-29 FOMC meeting will collectively influence market expectations for September rates. If the probability of a Fed rate hike falls below 50%, gold prices could move toward the upper end of the World Gold Council's valuation range ($4,305 per ounce); if gold prices fall below $4,000 per ounce, historically, selling pressure would increase first before long-term buying returns.