Executive Summary

Industrial valves are essential flow-control assets used in oil and gas, LNG, refining, petrochemicals, power generation, water and wastewater, mining, pharmaceuticals, food processing, semiconductors and emerging hydrogen and carbon-management systems. The market is broad, technically fragmented and difficult to measure through a single revenue figure because product scope varies between commodity isolation valves, severe-service control valves, actuated packages, safety valves and aftermarket services.

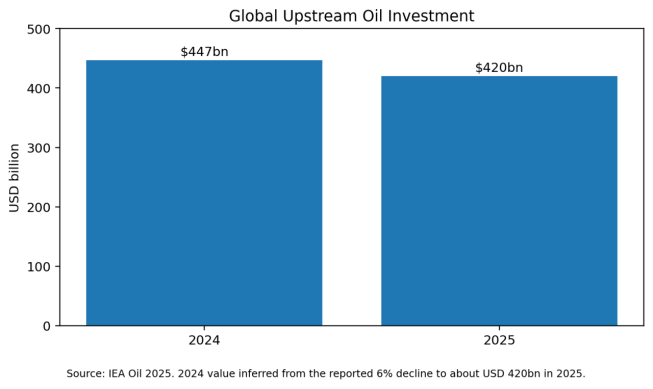

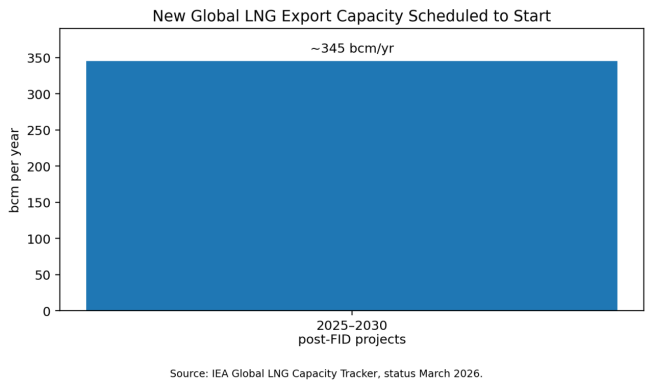

Demand through 2026–2030 is supported by several large investment cycles. The International Energy Agency estimates that global upstream oil investment was about USD 420 billion in 2025, while nearly 345 billion cubic metres per year of new LNG export capacity from post-FID projects is scheduled to enter operation between 2025 and 2030. Each liquefaction train, pipeline, tank farm and export terminal requires thousands of isolation, control, cryogenic, check and safety valves.

At the same time, valve procurement is becoming more demanding. Methane and volatile-organic-compound regulation is increasing the importance of low-emission stem packing, verified fugitive-emission performance and reliable actuator control. Hydrogen service creates new concerns around permeation, embrittlement, leakage and sealing. Water projects need corrosion resistance and low lifecycle maintenance, while mining and slurry applications prioritize erosion resistance and replaceable wear parts.

The purchasing logic is therefore moving away from the lowest unit price. Material traceability, pressure boundary integrity, seat leakage, actuator sizing, emissions performance, test certification, spare-part availability and local service can have greater lifecycle value than a modest saving in the initial quotation.

Key Findings

- Valve demand is diversified across energy, water, mining, chemicals, power and industrial automation, reducing dependence on a single end market.

- Global upstream oil investment remained around USD 420 billion in 2025 despite a reported 6% annual decline, sustaining demand for high-pressure and severe-service valves.

- About 345 bcm per year of new LNG export capacity is scheduled to start between 2025 and 2030, supporting cryogenic and large-bore valve demand.

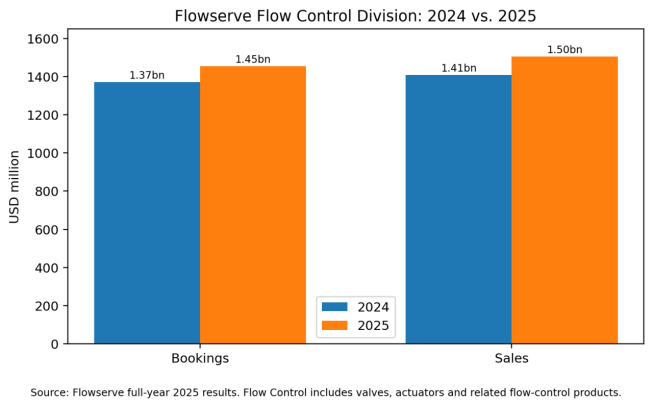

- Flowserve's Flow Control Division reported 2025 sales of about USD 1.50 billion, up 6.8% year on year, indicating healthy demand among major global customers.

- Regulation of methane and fugitive emissions is raising demand for low-emission packing, monitoring, electric actuation and verified leakage performance.

- Hydrogen, carbon capture and high-purity processing are creating technical opportunities but require stricter material, sealing and qualification discipline.

- International procurement is shifting toward lifecycle reliability, documentation quality and aftermarket support rather than ex-works price alone.

Figure 1. Global upstream oil investment, 2024–2025.

1. Product Definition and Market Segmentation

An industrial valve controls, isolates, directs or relieves fluid flow. The main functional categories are isolation valves, control valves, non-return valves and pressure-relief devices. Common designs include ball, gate, globe, butterfly, plug, diaphragm, pinch, knife-gate, check and safety-relief valves.

The market can also be segmented by actuation. Manual valves use handwheels, levers or gear operators. Automated valves use pneumatic, electric, hydraulic or electro-hydraulic actuators, often combined with positioners, limit switches and digital communication. In process plants, the actuator and control package may represent a major share of the total installed cost.

Materials range from cast iron and carbon steel to stainless steel, duplex, super-duplex, nickel alloys, titanium, bronze, engineering plastics and lined constructions. The correct material is determined by pressure, temperature, corrosion, erosion, fluid chemistry, cleanliness and fire-safety requirements.

|

Valve Category |

Typical Applications |

Primary Selection Variables |

Main Failure Risk |

|

Ball / plug |

Pipelines, LNG, terminals, chemical isolation |

Bore, seat design, fire-safe duty, emissions |

Seat damage, stem leakage, cavity pressure |

|

Gate |

Pipelines, power, water, refining |

Wedge/slab design, pressure class, body material |

Galling, seat wear, slow operation |

|

Globe / control |

Process control, steam, refining, chemicals |

Cv, trim, cavitation, noise, rangeability |

Erosion, cavitation, unstable control |

|

Butterfly |

Water, HVAC, power, large-diameter process lines |

Disc offset, seat type, torque, corrosion |

Seat wear, shaft leakage, torque margin |

|

Check |

Pumps, compressors, pipelines |

Closing speed, pressure drop, slam prevention |

Water hammer, disc wear, chatter |

|

Safety / relief |

Pressure vessels, boilers, process plants |

Set pressure, capacity, back pressure |

Incorrect sizing, leakage, failure to lift |

2. Global Demand Drivers

Oil and gas remains one of the largest value pools for engineered valves. Although upstream oil investment declined in 2025, the absolute level remained high. Brownfield maintenance, debottlenecking, pipeline integrity and emissions compliance support recurring valve replacement even when new-project activity slows.

LNG is a particularly valve-intensive growth segment. Liquefaction plants use large quantities of cryogenic ball and butterfly valves, control valves, emergency shutdown valves and safety devices. The IEA's 2026 LNG capacity tracker indicates that approximately 345 bcm per year of post-FID export capacity is scheduled to come online between 2025 and 2030, the largest expansion wave in the sector's history.

Water and wastewater demand is structurally supported by urbanization, aging networks, desalination and industrial reuse. This market favors resilient-seated gate valves, large butterfly valves, check valves, control valves and actuators with long service intervals. Price sensitivity is high, but corrosion resistance and maintainability determine lifecycle cost.

Mining demand is linked to copper, gold, iron ore and critical-mineral investment. Slurry valves face abrasion, scaling and high solids. Successful suppliers often compete through replaceable liners, severe-service materials and local service rather than through standard catalog products.

Figure 2. Scheduled global LNG export capacity additions from post-FID projects.

3. Regional Market Analysis

3.1 North America

North America combines upstream oil and gas, LNG export terminals, refining, chemicals, power, water infrastructure and a large installed base. U.S. methane regulation increases attention to fugitive-emission components, including valves. The region favors API and ASME compliance, NACE material requirements where sour service applies, documented low-emission testing and strong local aftermarket support.

3.2 Europe

Europe has mature refining and chemical assets, large water and district-energy systems and growing investments in hydrogen, biomethane, carbon capture and offshore energy. Buyers frequently emphasize emissions performance, functional safety, pressure-equipment compliance, traceability and energy-efficient actuation. Replacement and modernization are as important as greenfield projects.

3.3 China and Asia-Pacific

China has one of the world's broadest valve manufacturing bases and is a major supplier of cast, forged and automated valves. Domestic demand comes from petrochemicals, LNG, power, water, mining and advanced manufacturing. Export competitiveness is strong in standardized products, but high-end severe-service applications still depend heavily on qualification history, proprietary trim technology and customer trust.

India, Southeast Asia and Australia offer growth through refining, chemicals, LNG, mining, water and power investment. Local-content rules, project financing and service networks strongly influence supplier selection.

3.4 Middle East

The Middle East is one of the most attractive regions for project valves because of upstream expansion, gas processing, LNG, refining, petrochemicals, desalination and hydrogen-related projects. Large EPC packages require approved-vendor status, project-specific documentation, rapid submittals and reliable delivery. High temperature, sand, seawater and sour service raise material and coating requirements.

3.5 Latin America and Africa

Latin America has opportunities in oil and gas, mining, pulp and paper, water and renewable fuels. Brazil, Mexico, Guyana, Argentina, Chile and Peru are notable project markets. Africa combines upstream energy, mining, water and power demand, but local service, financing, customs and spare-parts logistics are significant commercial risks.

4. End-Market Economics

|

End Market |

Demand Outlook |

High-Value Valve Types |

Key Procurement Concern |

|

Oil & gas upstream |

Stable to selective growth |

API 6A/6D valves, choke valves, ESD valves |

Pressure integrity, emissions, sour service |

|

LNG & gas processing |

Strong through 2030 |

Cryogenic ball/butterfly, control, safety valves |

Low-temperature sealing, fire safety, delivery |

|

Refining & chemicals |

Brownfield-heavy |

Control, severe-service, lined, high-alloy valves |

Corrosion, coking, cavitation, emissions |

|

Water & wastewater |

Structurally positive |

Butterfly, gate, check, control valves |

Corrosion, low maintenance, actuator reliability |

|

Power & nuclear |

Selective but high value |

Main steam, feedwater, safety and isolation valves |

Qualification, documentation, long service life |

|

Mining & minerals |

Commodity-cycle dependent |

Knife gate, pinch, slurry control valves |

Erosion, replaceable wear parts, local service |

|

Hydrogen & CCS |

Emerging |

High-integrity ball, control and check valves |

Permeation, leakage, materials, qualification |

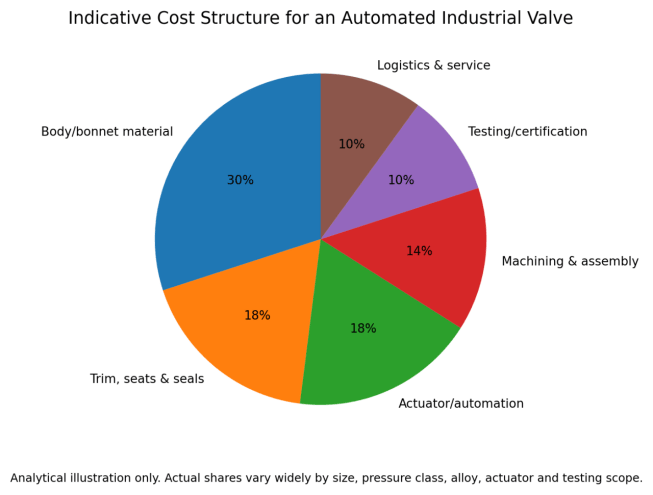

5. Price and Cost Structure

Industrial valve prices vary by several orders of magnitude. A small cast-iron water valve and a large-bore, high-pressure, cryogenic or nuclear-qualified valve cannot be compared by diameter alone. Pressure class, body material, trim alloy, seat technology, actuator, testing, certification and documentation may matter more than nominal size.

Body and bonnet materials are often the largest cost element in manual valves. In automated or control-valve packages, actuators, positioners and instrumentation can equal or exceed the pressure-containing body cost. Severe-service trims using tungsten carbide, Stellite-type hardfacing, ceramics or nickel alloys increase both material and machining expense.

Testing and documentation are genuine cost drivers. Hydrostatic shell testing, seat-leak testing, fire-safe qualification, fugitive-emission testing, nondestructive examination, positive material identification and customer witness inspection can add engineering hours and extend lead times.

Figure 3. Indicative cost structure for an automated industrial valve.

6. Materials and Supply Chain

Carbon steel remains the workhorse pressure-boundary material, while stainless steel and duplex grades are common in corrosive service. Nickel-based alloys are used where chlorides, acids, high temperature or hydrogen-related conditions exceed stainless-steel capability. Material choice affects casting availability, machining difficulty, weld procedures and inspection requirements.

Critical supply-chain items include castings, forgings, stems, seats, packing, elastomers, actuators, gearboxes, solenoid valves, positioners and limit switches. A valve manufacturer may machine and assemble in-house but rely on external foundries and actuator suppliers. Buyers should therefore audit sub-supplier controls and material traceability.

Lead times are most sensitive for large forgings, exotic alloys, high-pressure bodies, cryogenic extensions, custom trim and qualified electric actuators. Commodity valves can often be sourced quickly, while project-specific severe-service valves may require months of engineering, casting, machining and testing.

7. Regulation, Standards and Emissions

ASME B16.34 establishes pressure-temperature ratings, materials, examination, testing and marking for flanged, threaded and welding-end valves. ASME B16.10 standardizes face-to-face and end-to-end dimensions, supporting interchangeability. API Specification 6D is central to pipeline and piping valves.

API has updated API 6D to address hydrogen gas service, reflecting the industry's need to qualify materials, seals and designs for a different leakage and integrity environment. Hydrogen molecules are small, and some metallic materials can lose ductility under certain conditions.

In the United States, EPA methane rules define valves as fugitive-emission components in oil and gas facilities. This strengthens the commercial value of low-emission packing, stem sealing, electric or instrument-air actuation and verified maintenance practices.

|

Requirement |

What It Covers |

Buyer Action |

|

ASME B16.34 |

Pressure-temperature ratings, materials, testing, marking |

Verify pressure class, material group and test scope |

|

ASME B16.10 |

Face-to-face and end-to-end dimensions |

Confirm interchangeability with installed piping |

|

API 6D |

Pipeline and piping valves |

Check edition, monogram status and project addenda |

|

API 607 / 6FA |

Fire testing of valves |

Confirm relevance to soft-seat or project fire-safe duty |

|

API 624 / ISO 15848 |

Fugitive-emission performance |

Specify allowable leakage and test cycle |

|

NACE / ISO 15156 |

Materials for H2S-containing environments |

Confirm hardness, material condition and traceability |

8. Technology Trends

Digital valve positioners, smart electric actuators and wireless monitoring are expanding. These technologies can detect friction, stiction, slow travel, packing deterioration and actuator problems before process performance is affected. Predictive maintenance is most valuable in plants where a failed control valve can constrain production.

Electric actuation is gaining interest where methane or instrument-air emissions must be reduced, where compressed-air infrastructure is limited, or where remote control is required. Pneumatic actuation remains dominant in many process plants because of speed, simplicity and established safety practice.

Additive manufacturing is being evaluated for complex trims, spare parts and rapid prototyping, but pressure-boundary certification and material consistency limit widespread use. Advanced coatings, hardfacing and engineered polymers are improving erosion, corrosion and low-temperature performance.

9. Competitive Landscape

The global valve industry includes diversified flow-control groups, specialist control-valve companies, pipeline-valve manufacturers, water-valve suppliers and thousands of regional producers. Major names include Emerson, Flowserve, IMI, KSB, KITZ, Crane, Velan, Neway, Metso and numerous specialized severe-service brands.

Flowserve's Flow Control Division reported 2025 sales of USD 1.5045 billion and bookings of USD 1.4543 billion, both above 2024 levels. In early 2026, Flowserve announced the acquisition of Trillium Flow Technologies' Valves Division for USD 490 million; the acquired business was expected to contribute approximately USD 200 million in annualized revenue. The transaction highlights consolidation around nuclear, power and severe-service capabilities.

Competition is shifting from product breadth alone toward application engineering, installed-base service, emissions performance and rapid replacement. Suppliers with local service centers and a large installed base can earn resilient aftermarket revenue even when greenfield projects slow.

Figure 4. Flowserve Flow Control Division performance, 2024–2025.

10. International Trade and Procurement

Valve trade is difficult to analyze through a single HS code because industrial valves are split across product categories and can include actuators or complete assemblies. Customs value also mixes commodity and engineered products. Buyers should avoid using average import value as a proxy for a project valve quotation.

China, Italy, Germany, the United States, Japan, South Korea and India are important manufacturing and export bases, but competitive strength varies by segment. China is highly competitive in volume production and increasingly active in API, petrochemical and LNG applications. European, Japanese and U.S. suppliers retain strong positions in control valves, nuclear service, proprietary severe-service trim and demanding installed-base applications.

Cross-border procurement must address Incoterms, inspection, documentation language, spare parts, field service, warranty enforcement, export controls, local certification and customs classification. A low ex-works price can become uneconomic if the project requires repeated document revisions, re-testing or emergency replacement.

11. Total Cost of Ownership

TCO = Purchase + Engineering + Actuation + Installation + Energy Loss + Maintenance + Leakage + Downtime + Spares − Residual Value

A control valve that is incorrectly sized can operate near the seat, create noise and cavitation, consume excessive pumping energy and wear rapidly. A properly selected valve may cost more initially but reduce process variability and maintenance.

Isolation-valve TCO depends on seat life, torque growth, stem packing, actuator margin and the ability to repair in line. In critical service, one unplanned shutdown can exceed the original equipment price many times over.

Leakage has both safety and economic consequences. Fugitive emissions waste product, create regulatory exposure and require maintenance labor. Through-seat leakage can reduce process efficiency or allow hazardous mixing. Buyers should therefore evaluate verified leakage class rather than relying on generic 'bubble-tight' claims.

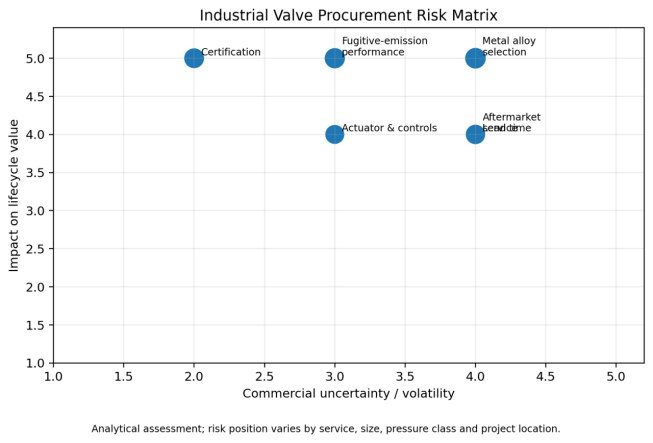

Figure 5. Industrial valve procurement risk matrix.

12. Procurement Recommendations

Define service conditions completely: Provide fluid composition, pressure, temperature, solids, corrosion, cycling, shutoff class and upset conditions.

Specify the applicable standard and edition: Avoid generic references that leave pressure class, testing or emissions requirements ambiguous.

Separate valve and actuator sizing: Confirm maximum differential pressure, safety factor, fail position, stroke time and available utility supply.

Audit material traceability: Require heat numbers, PMI where relevant, weld procedures and certification for pressure-boundary and trim materials.

Validate fugitive-emission claims: Use API 624, ISO 15848 or project-specific leakage criteria rather than marketing language.

Review sub-suppliers: Identify casting, actuator, positioner, packing and seal suppliers and approved alternatives.

Evaluate lifecycle service: Price commissioning, spares, repair kits, diagnostics and field response at the award stage.

Use staged inspection: Apply design review, foundry audit where needed, NDE review, FAT, packing inspection and site acceptance.

Compare delivered TCO: Include pressure drop, actuator energy, maintenance intervals, downtime and emissions exposure.

Standardize where possible: Common sizes, materials, actuators and accessories reduce inventory and training cost.

13. Market Outlook, 2026–2030

The outlook for industrial valves is moderately positive, with stronger growth in LNG, gas infrastructure, water, mining, data-center utilities, hydrogen pilots and carbon-management projects. Oil upstream spending is unlikely to rise uniformly, but brownfield integrity and emissions requirements will sustain replacement demand.

Price competition will remain intense in standard gate, globe, ball and butterfly valves. Engineered segments will be less commoditized because material qualification, emissions performance, actuation, digital diagnostics and field service create higher barriers.

Suppliers that combine cost-efficient manufacturing with application engineering and local aftermarket support are best positioned. Chinese manufacturers will continue to gain export share, but the largest value opportunity lies in moving from catalog products to qualified project packages and installed-base service.

Conclusion

The global valve market is not a single commodity market. It is a collection of application-specific businesses tied to energy, water, mining and process-industry investment. Demand is supported by the largest LNG build-out in history, continuing oil and gas expenditure, water infrastructure needs and the emergence of hydrogen and carbon-management systems.

The commercial center of gravity is moving toward leakage control, severe-service reliability, automation, traceability and lifecycle support. For buyers, the correct objective is not the lowest valve price but the lowest risk-adjusted cost of controlling the process over the asset life.

For manufacturers, long-term competitiveness will depend on qualified materials, repeatable quality, standards compliance, documentation speed, local service and credible performance in demanding applications.