Executive Summary

The global battery industry has entered a scale-and-structure phase rather than a simple expansion phase. Demand is rising rapidly in electric mobility, stationary storage, data centres, industrial backup power and distributed energy systems, but growth is no longer sufficient by itself to guarantee attractive returns. The decisive issues are now chemistry selection, manufacturing utilisation, regional policy, supply-chain concentration, project bankability, safety and recycling.

Because “battery” spans lead-acid, lithium-ion, nickel-based, sodium-ion, flow and emerging solid-state systems, a single market-value estimate is often misleading. This report therefore uses physical demand indicators—GWh/TWh, manufacturing capacity, deployment, price per kWh and regional production shares—as the primary analytical framework. Lithium-ion batteries dominate the fastest-growing segments, while lead-acid remains important in automotive starting, telecom, UPS and industrial standby applications.

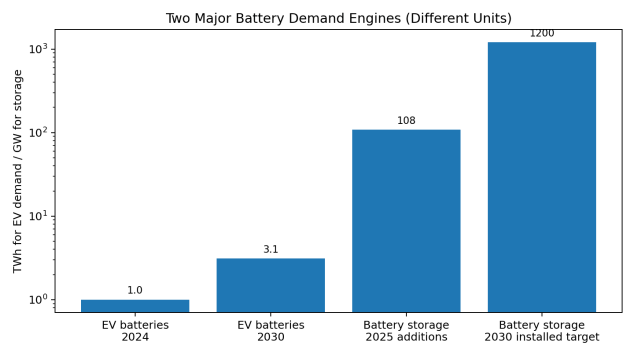

In 2025, global electric-car sales exceeded 20 million and represented roughly one-quarter of new-car sales. EV battery demand was around 1 TWh in 2024 and is expected to exceed 3 TWh by 2030 under stated policies. Battery storage also accelerated sharply: 108 GW of new capacity was deployed worldwide in 2025, 40% more than in 2024. These two demand engines are reinforcing investment across cells, materials, battery-management systems, thermal management, power electronics and recycling.

Key Findings

- Battery demand is becoming structurally diversified: EVs remain the largest volume driver, while stationary storage, UPS and commercial vehicles are growing faster from smaller bases.

- Average lithium-ion battery pack prices fell to about USD 108/kWh in 2025; stationary-storage pack prices fell to about USD 70/kWh, intensifying pressure on manufacturers and accelerating project economics.

- LFP has become the default chemistry for most stationary-storage projects and an increasing share of mass-market EVs because of cost, safety and cycle-life advantages.

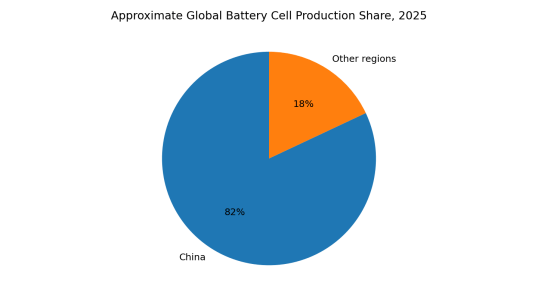

- China remains the centre of the global value chain, accounting for more than 80% of cell production in 2025 and an even higher share of cathode, anode and recycling capacity.

- North America and Europe are expanding local manufacturing, but project delays, utilisation rates, costs, policy uncertainty and dependence on Asian materials remain major constraints.

- Sodium-ion is moving from demonstration toward selective commercialisation, especially where low cost, cold-weather performance and mineral diversification matter more than maximum energy density.

- Solid-state batteries remain strategically important but are unlikely to displace mainstream lithium-ion at scale in the near term; initial adoption will focus on premium vehicles and specialised applications.

- The strongest opportunities are shifting from cell capacity alone toward integrated systems, safety engineering, BMS/EMS, thermal management, recycling, localisation and lifecycle services.

Figure 1. EV battery demand and battery-storage deployment are shown with different units; the figure illustrates scale and direction rather than direct comparability.

1. Global Market Definition and Demand Structure

The rechargeable battery market can be divided into five commercially distinct demand pools: electric mobility; stationary energy storage; consumer electronics; industrial and data-centre backup; and conventional automotive/industrial lead-acid applications. Each has different requirements for energy density, power, cycle life, safety, warranty, certification and cost.

|

Application |

Main chemistries |

Buyer priority |

Commercial model |

2026 direction |

|

Passenger EVs |

LFP, NMC/NCA |

Range, cost, fast charging |

Long-term OEM supply |

Strong volume growth; price pressure |

|

Commercial vehicles |

LFP, high-nickel variants |

Durability, uptime, energy density |

Fleet/OEM contracts |

Faster share gains in battery demand |

|

Grid & C&I storage |

LFP, sodium-ion, flow |

Safety, cycle life, bankability |

System/EPC procurement |

Fastest power-sector growth |

|

Consumer electronics |

LCO/NMC, silicon-enhanced |

Energy density, compactness |

High-volume electronics supply |

Mature, replacement-led |

|

UPS/data centres |

LFP, lead-acid |

Reliability, footprint, response |

Facility/project procurement |

Strong AI/data-centre demand |

|

Industrial/starting |

Lead-acid, lithium-ion |

Cost, robustness, availability |

Distributor/OEM channels |

Stable with selective lithium substitution |

2. Demand Outlook to 2030

2.1 Electric mobility remains the largest volume driver

The IEA reports that global EV battery demand was about 1 TWh in 2024 and is expected to exceed 3 TWh in 2030 under stated policies. Passenger cars remain dominant, but electric trucks, buses, two-wheelers and light commercial vehicles will increase their share. The implication for suppliers is that product portfolios must broaden: high-energy packs for long-range vehicles will coexist with cost-optimised LFP packs and high-cycle commercial-vehicle systems.

2.2 Stationary storage is becoming a second industrial pillar

Battery storage is now the fastest-growing power technology. Global additions reached 108 GW in 2025, and the IEA pathway consistent with tripling renewable-energy capacity requires battery storage to rise to around 1,200 GW by 2030. This creates demand not only for cells but also for containers, racks, liquid cooling, fire detection and suppression, power conversion systems, EMS software, transformers, switchgear and long-term service.

2.3 Data centres and industrial resilience are underappreciated demand sources

AI-related data-centre construction, digital infrastructure and industrial resilience are increasing demand for high-reliability UPS and backup systems. In 2025, battery-based UPS additions—primarily in data centres—rose to roughly 45 GW. Lithium-ion is gaining share where footprint, cycling capability and total cost of ownership are decisive, while lead-acid retains a large installed base because of familiarity and low upfront cost.

3. Price and Cost Trends

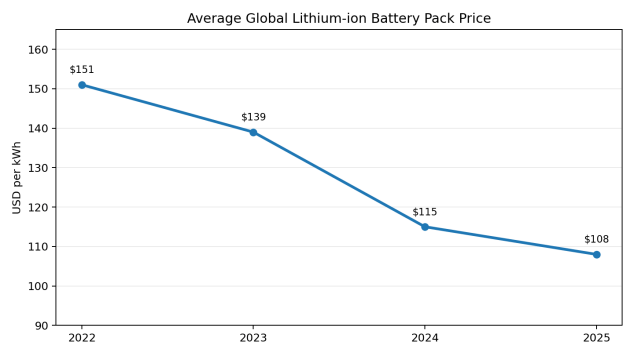

Figure 2. Average lithium-ion pack prices, 2022-2025. Sources: BloombergNEF annual battery price surveys.

Average global lithium-ion pack prices declined from USD 151/kWh in 2022 to USD 108/kWh in 2025. The decline reflects lower material costs than the 2022 peak, manufacturing overcapacity, intense competition, larger LFP penetration, cell-to-pack design and manufacturing learning. Stationary-storage packs fell to approximately USD 70/kWh in 2025, although complete installed BESS costs remain much higher after power electronics, enclosures, thermal management, fire protection, EPC, grid connection and financing are included.

Price declines are positive for EV affordability and project economics but create three risks: squeezed cell margins, aggressive warranty assumptions and quality dispersion among suppliers. Procurement should therefore compare usable lifetime energy, degradation guarantees, thermal performance, safety certification, augmentation requirements and supplier balance-sheet strength rather than headline USD/kWh alone.

4. Technology Routes and Product Evolution

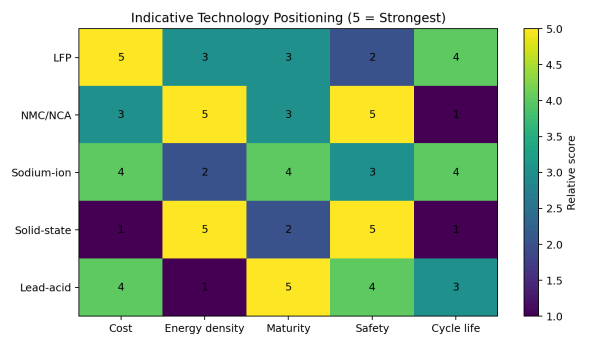

Figure 3. Indicative technology positioning. Scores are qualitative and application-dependent.

LFP

LFP is now the dominant chemistry in stationary storage and a major EV chemistry. It offers lower cost, strong thermal stability and long cycle life, but lower gravimetric energy density than nickel-rich chemistries. Its continued evolution is centred on fast charging, low-temperature performance, higher packing efficiency and improved BMS estimation.

NMC and NCA

Nickel-rich chemistries remain important where energy density, range and weight are critical. Their challenge is balancing performance with cost, thermal stability, material sourcing and more complex recycling economics.

Sodium-ion

Sodium-ion reduces dependence on lithium, nickel and cobalt and can offer good low-temperature performance and safety. Near-term adoption is most plausible in entry-level mobility, short-duration stationary storage, telecom and selected industrial applications.

Solid-state

Solid-state systems promise higher energy density and improved safety potential, but manufacturing yield, interface stability, cycle life and cost remain barriers. Commercial introduction is likely to be gradual and premium-led rather than an abrupt market replacement.

Lead-acid and flow batteries

Lead-acid remains commercially resilient in starting, telecom and backup power. Flow batteries address long-duration storage niches where long cycle life and independent sizing of power and energy can offset lower efficiency and higher balance-of-plant complexity.

5. Global Supply Chain and Manufacturing Geography

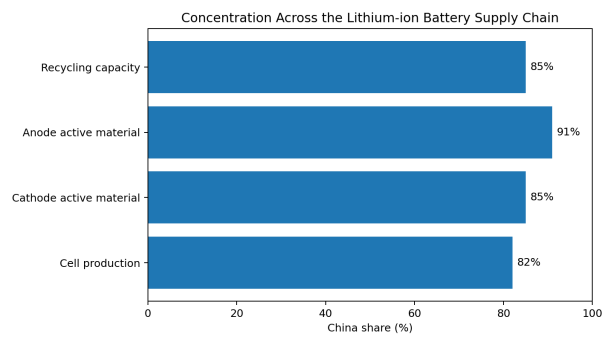

China accounted for more than 80% of global battery cell production in 2025, around 85% of cathode active material and more than 90% of anode active material production. It also hosts over 85% of global recycling capacity. This concentration lowers cost through scale and cluster effects, but increases geopolitical, trade and single-region dependency risks for buyers outside China.

North America is building a more localised supply chain through cell plants, component manufacturing, mineral processing and recycling support. Europe is pursuing lifecycle regulation, carbon-footprint disclosure, recycled-content rules and regional manufacturing. Korea and Japan remain technologically influential through major cell producers and materials companies. India and Southeast Asia are emerging as demand and manufacturing locations, but require deeper local supplier ecosystems and skills.

6. Regional Market Analysis

|

Region |

Demand drivers |

Supply position |

Buyer requirements |

Strategic outlook |

|

China |

EV scale, storage, industrial policy |

Deepest integrated chain |

Aggressive cost, rapid iteration |

Largest market and export base; intense margin pressure |

|

North America |

EVs, data centres, utility storage |

Rapidly expanding but import-dependent |

UL/NFPA, domestic-content rules, bankability |

High-value market with policy and trade risk |

|

Europe |

Fleet electrification, grid flexibility, circularity |

Cell projects face cost/utilisation pressure |

EU Battery Regulation, carbon and traceability |

Strong compliance-led opportunity; difficult economics |

|

Korea & Japan |

Premium batteries, OEM exports, technology |

Strong incumbent manufacturers |

High quality and OEM qualification |

Technology and partnership hub |

|

India |

Two/three-wheelers, buses, storage, telecom |

Early-stage local chain |

Cost, heat tolerance, local service |

High-growth localisation market |

|

Southeast Asia |

Two-wheelers, electronics, renewables |

Emerging manufacturing clusters |

Cost, tropical performance, financing |

Attractive assembly and demand growth |

|

Middle East & Africa |

Solar-plus-storage, mini-grids, backup |

Mostly import-dependent |

Heat, bankability, remote O&M |

Project-led opportunity with execution risk |

|

Latin America |

EV niches, mining, renewables, telecom |

Mineral-rich but limited cell production |

Financing, import logistics, local service |

Strong storage and materials potential |

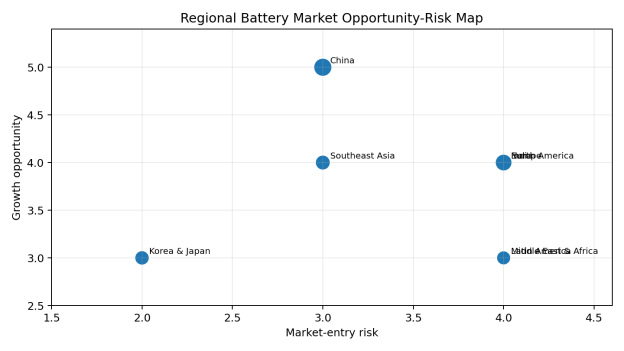

Figure 4. Qualitative regional opportunity-risk assessment for 2026-2030.

7. Competitive Landscape

The competitive landscape is segmented by application and geography. CATL and BYD are major global forces in EV and stationary-storage batteries; LG Energy Solution, Samsung SDI, SK On and Panasonic Energy retain strong relationships with global vehicle manufacturers and premium applications. EVE Energy, CALB, Gotion, Envision AESC and other Chinese producers are expanding internationally. In lead-acid and industrial batteries, companies such as Clarios, EnerSys, Exide and GS Yuasa remain important. System-level competition also includes Tesla, Fluence, Sungrow, Wärtsilä and numerous regional integrators.

Competitive advantage is increasingly defined by more than cell energy density. Key differentiators include manufacturing yield, chemistry flexibility, safety record, warranty credibility, global qualification, software, pack integration, thermal management, local service, financing acceptance, recycling access and the ability to comply with regional trade and sustainability rules.

|

Competitive tier |

Typical strengths |

Typical weakness |

Best-positioned opportunities |

|

Global scale leaders |

Cost, volume, integration, customer base |

Trade exposure, margin pressure |

Global EV platforms and utility storage |

|

Technology-focused incumbents |

Quality, OEM relationships, advanced chemistries |

Higher cost, slower scaling |

Premium EVs and demanding industrial uses |

|

Regional manufacturers |

Local content, service, procurement access |

Limited scale and materials leverage |

Protected/localised markets |

|

System integrators |

Bankability, controls, EPC and service |

Dependence on cell suppliers |

Grid, C&I and data-centre projects |

|

Recyclers/materials firms |

Feedstock recovery and compliance value |

Feedstock timing and price volatility |

Closed-loop contracts and EU/US localisation |

8. Regulation, Certification and Procurement Logic

The EU Battery Regulation establishes lifecycle requirements covering sustainability, safety, labelling, due diligence, collection, recycling and material recovery. Recycling-efficiency targets applicable by the end of 2025 include 65% for lithium-based batteries and 75% for lead-acid batteries. For suppliers, compliance capability is becoming a market-access asset rather than an administrative afterthought.

In North America, project requirements often combine UL product standards, NFPA fire-safety considerations, local permitting, utility interconnection and domestic-content or sourcing rules. Automotive supply requires lengthy OEM qualification, PPAP-style quality systems, traceability and warranty data. Stationary-storage buyers increasingly require bankability studies, cell-level test evidence, propagation controls, cybersecurity and long-term service commitments.

Recommended buyer evaluation criteria

- Verified cell origin and bill of materials

- Independent safety and abuse-test evidence

- Cycle-life data under realistic temperature and C-rate

- Warranty terms linked to throughput and state of health

- BMS/EMS interoperability and cybersecurity

- Thermal-management design and propagation control

- Supplier financial strength and recall history

- Local spare parts, commissioning and emergency response

- End-of-life, recycling and regulatory traceability

- Total installed and lifecycle cost, not cell price alone

9. Industrial and Market Opportunities

Integrated storage systems

Growth in grid, C&I, microgrid and data-centre applications creates demand for complete systems rather than cells alone.

Safety and thermal management

Higher deployment density increases demand for sensors, liquid cooling, fire detection, suppression and safer enclosure design.

BMS, EMS and diagnostics

Software and controls can improve usable energy, reduce degradation and support predictive maintenance.

Localisation and certification services

Regional content rules and complex standards create opportunities for local assembly, testing and compliance engineering.

Recycling and second life

Regulation and future feedstock volumes support closed-loop materials recovery, though economics depend on chemistry and collection.

Sodium-ion supply chains

Early commercial markets may reward suppliers of cathode, electrolyte, cell equipment and application-specific integration.

Industrial equipment and manufacturing tools

Dry rooms, coating, calendaring, formation, testing, inspection and automation remain critical investment areas.

After-sales and performance guarantees

Long-duration warranties and fleet/project data create recurring service and analytics opportunities.

10. Risk Assessment

|

Risk |

Likelihood |

Impact |

Mitigation |

|

Manufacturing overcapacity |

High |

High |

Flexible output, disciplined capex, secured offtake |

|

Trade and localisation barriers |

High |

High |

Regional partnerships, traceable sourcing, dual supply |

|

Raw-material volatility |

Medium |

High |

Long-term contracts, chemistry diversification, recycling |

|

Safety incidents and recalls |

Medium |

Very high |

Independent testing, propagation control, quality systems |

|

Technology obsolescence |

Medium |

High |

Modular platforms and chemistry-agnostic integration |

|

Warranty underpricing |

Medium |

High |

Conservative degradation models and reserves |

|

Project delay/interconnection |

High |

Medium |

Early grid studies, permitting and EPC coordination |

|

Recycling-feedstock mismatch |

Medium |

Medium |

Long-term collection contracts and flexible processes |

11. Outlook: 2026-2030

The global battery market will continue to grow strongly through 2030, but the industry will become more selective. EV demand will expand beyond passenger cars, stationary storage will become a major power-sector asset class, and data centres will add a high-reliability demand layer. LFP will remain the dominant volume chemistry in storage and cost-sensitive mobility, while nickel-rich chemistries will defend applications where energy density matters. Sodium-ion will gain commercial niches, and solid-state batteries will advance through limited, premium-scale introductions.

The central commercial challenge is not whether battery demand will grow, but who can convert growth into durable returns. Companies with scale but weak utilisation may struggle; companies with advanced technology but no bankable manufacturing path may also underperform. The most resilient suppliers will combine cost control, application engineering, safety, local compliance, service, data and recycling into a lifecycle proposition.

For global buyers, the optimal strategy is likely to be diversified rather than purely local or purely lowest-cost. A balanced procurement model should combine globally competitive cell supply with regional integration, certification, inventory, technical service and end-of-life capability. For manufacturers and component suppliers, the strongest opportunities lie where global scale intersects with local execution.