执行摘要

全球断路器市场正进入一个结构性有利的投资周期。电网扩建、老旧电力基础设施的更新换代、数据中心建设、工业电气化、可再生能源并网、电池储能、电动汽车充电以及高压直流系统的兴起等因素共同拉动了市场需求。由于一些研究仅涵盖独立断路器,而另一些研究则涵盖了相关保护设备,因此公开市场预测数据存在差异,但较为可靠的2025年市场规模预测值集中在216亿至244亿美元之间。因此,合理的规划范围应为2025年市场规模约为220亿至240亿美元,大多数预测都指向到2030年将保持中等个位数的年增长率。

市场也日趋细分。传统机械断路器在销量上仍然占据主导地位,尤其是在住宅、商业和传统工业系统中。中压真空断路器是配电网和工业变电站的商业核心。随着电力公司寻求六氟化硫 (SF6) 的替代品,高压断路器正面临技术转型。与此同时,直流断路器和固态断路器虽然基数较小,但增长速度更快,因为数据中心、电池系统、可再生能源、铁路牵引和新兴的直流配电架构需要更快、更可控的故障切断。

对制造商而言,制胜之道在于超越断路器本身。买家越来越重视整体保护性能、数字脱扣器、通信功能、状态监测、电弧闪光抑制、网络安全、认证、可维护性以及与配电盘或开关设备的兼容性。其结果是,低成本的通用产品仍然对价格敏感,而工程断路器和集成保护系统则面临着更高的技术和服务门槛。

主要发现

- Global market value is best treated as a range: approximately USD 22-24 billion in 2025, with published 2030 forecasts generally near USD 28-30 billion.

- Asia-Pacific is the largest demand region, while North America currently offers some of the strongest pricing, backlog and data-center-driven growth conditions.

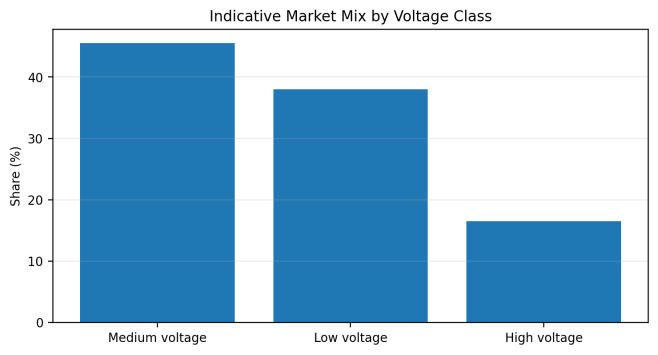

- Medium voltage is the largest voltage segment in several market studies, reflecting distribution-grid reinforcement, renewable interconnection and industrial substation investment.

- Annual global grid investment needs to rise toward roughly USD 600 billion through 2030 in the IEA net-zero pathway, almost double the recent annual level, supporting long-cycle demand for protection equipment.

- DC breakers, hybrid breakers and solid-state designs are the fastest-moving technology niches, although certification, conduction losses and cost still limit near-term mass adoption.

- SF6-free high-voltage switching is becoming a strategic procurement issue in Europe and increasingly in other regulated markets.

- Competition is led by ABB, Schneider Electric, Eaton, Siemens, Mitsubishi Electric, Hitachi Energy and other established electrical groups, but regional manufacturers remain strong in standardized low- and medium-voltage products.

- International suppliers must localize certification, panel integration, service, spare parts and channel coverage; product-only export strategies are less defensible in critical infrastructure applications.

1. Market Definition and Product Scope

A circuit breaker is an automatic switching and protection device that interrupts current under overload, short-circuit, ground-fault or other abnormal conditions. The category spans miniature circuit breakers (MCBs), molded-case circuit breakers (MCCBs), residual-current and ground-fault devices, air circuit breakers (ACBs), medium-voltage vacuum circuit breakers, high-voltage gas or alternative-gas circuit breakers, DC breakers and emerging solid-state breakers.

|

Segment |

Typical voltage/application |

Main demand drivers |

Commercial characteristics |

|

MCB / RCBO / residential |

Low voltage; homes and light commercial |

Building construction, safety codes, renovation |

High volume, channel-driven, strong price competition |

|

MCCB / ACB |

Low voltage; industrial, commercial, data centers |

Power density, selectivity, digital monitoring |

Higher value, often integrated into panels and switchboards |

|

Vacuum circuit breaker |

Medium voltage distribution |

Utilities, renewables, factories, infrastructure |

Engineering-led; reliability and service life are critical |

|

High-voltage breaker |

Transmission and substations |

Grid expansion, interconnectors, offshore wind |

Project-based, long qualification cycles, high service barrier |

|

DC / hybrid / solid-state |

Storage, PV, EV charging, rail, DC microgrids |

Rapid DC electrification and faster protection needs |

Fast growth from a small base; high technical and certification intensity |

2. Global Market Size and Growth Outlook

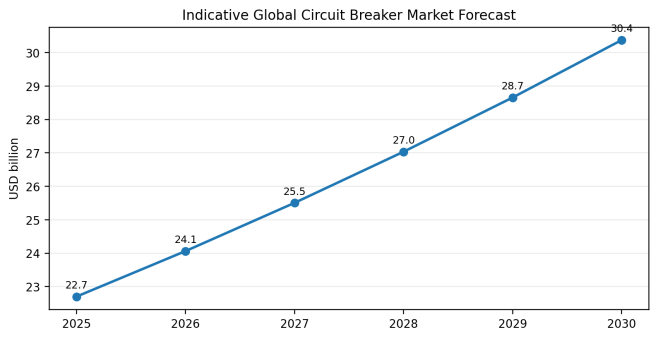

Published market estimates should not be presented as perfectly comparable. MarketsandMarkets estimates USD 22.70 billion in 2025 and USD 30.32 billion in 2030, implying a 6.0% CAGR. Mordor Intelligence estimates USD 21.61 billion in 2025 and USD 28.36 billion in 2030. Fortune Business Insights reports USD 24.41 billion for 2025. The spread primarily reflects differences in product scope, voltage coverage and whether fuses or related protection equipment are included.

Figure 1. Indicative global circuit breaker market forecast, 2025-2030

Source: Calculated from the MarketsandMarkets 2025 estimate of USD 22.70 billion and 6.0% CAGR; cross-checked against other public market estimates.

The most defensible conclusion is not the exact decimal point but the direction: the market is likely to grow at a mid-single-digit rate, while selected subsegments grow faster. Grand View Research estimates the global DC circuit breaker market at USD 4.38 billion in 2024 and projects USD 7.22 billion by 2030, an 8.7% CAGR. This reflects the rapid build-out of storage, EV charging, photovoltaics and DC-rich electrical architectures.

3. Demand Drivers

3.1 Grid expansion and replacement

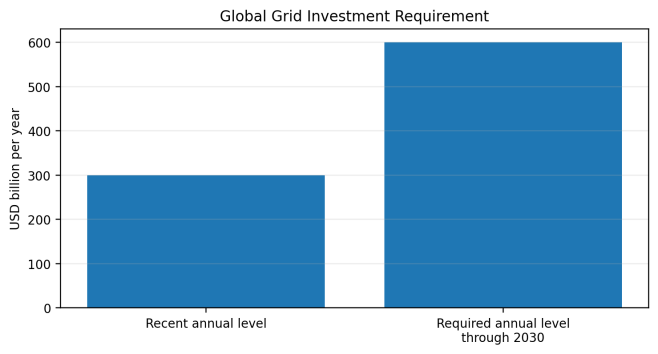

Circuit breakers are indispensable in every new substation, feeder, switchboard and major grid connection. The IEA estimates that electricity-grid investment needs to average about USD 600 billion per year through 2030 to align with its net-zero pathway, almost twice the recent annual level of roughly USD 300 billion. Even outside a net-zero scenario, electrification and reliability requirements imply sustained spending on distribution automation, fault protection and replacement of aging equipment.

Figure 2. Global grid investment requirement

Source: International Energy Agency, Smart Grids and Electricity Grids analysis.

3.2 Data centers and high-density commercial power

AI and cloud infrastructure are increasing power density and fault-current complexity in large facilities. Data centers require selective coordination, high interrupting ratings, arc-flash reduction, remote operation and continuous monitoring. Schneider Electric reported that its Energy Management business grew 11% organically in 2025, led by data centers, while Eaton continued to report strong Electrical Americas growth and rising backlog. These results do not isolate circuit breakers, but they are strong evidence of the demand environment for low-voltage protection and distribution systems.

3.3 Renewables, storage and EV charging

Renewable plants and battery systems introduce bidirectional power flows, high DC voltages and different fault-current behavior from conventional AC networks. This expands demand for DC-rated MCCBs, high-speed DC breakers and coordinated protection with inverters and battery-management systems. EV fast-charging hubs also require high-current low-voltage protection, residual-current protection and increasingly intelligent monitoring.

3.4 Industrial electrification and resilience

Factories, mines, ports, rail systems, semiconductor plants and water infrastructure are increasing electrical loads while reducing tolerance for downtime. Buyers therefore value breakers with predictive maintenance, communication protocols, event logging and rapid replacement. In critical industries, life-cycle service and installed-base compatibility can outweigh the purchase price.

4. Regional Market Structure

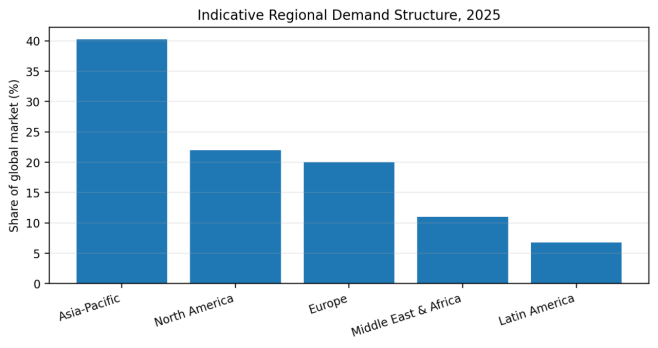

Figure 3. Indicative regional demand structure, 2025

Source: Asia-Pacific share from Fortune Business Insights; other regional shares are an analyst normalization for strategic comparison and should not be read as audited market shares.

4.1 Asia-Pacific

Asia-Pacific is the largest global market, supported by China’s manufacturing scale and grid investment, India’s distribution expansion, Southeast Asian electrification and continued industrial construction. The region is highly competitive in low-voltage products, with local brands exerting strong price pressure. Opportunities are strongest in medium-voltage vacuum breakers, renewable-energy protection, data-center-grade low-voltage systems and products that meet international certification requirements.

4.2 North America

North America combines aging-grid replacement, utility resilience spending, rapid data-center construction, semiconductor investment and reshoring. UL 489, ANSI/IEEE practices, interrupting ratings, short-circuit current ratings and local panelboard compatibility are central to market access. Eaton’s Electrical Americas sales reached USD 3.6 billion in the first quarter of 2026, up 20% year on year, and backlog was 44% higher than a year earlier, illustrating the strength of the broader electrical equipment cycle.

4.3 Europe

Europe is driven by renewable interconnection, offshore wind, cross-border transmission, electrification and replacement of older equipment. The region is also a leading market for SF6 reduction and digital grid technologies. Suppliers must navigate IEC standards, EU conformity requirements, sustainability expectations and increasingly detailed environmental product information.

4.4 India, Middle East and emerging markets

India offers high volume through grid reinforcement, renewable additions, metro systems and industrial growth, but pricing and localization requirements are demanding. The Middle East is attractive for utility-scale renewables, data centers, oil and gas, desalination and urban megaprojects. Southeast Asia, Latin America and Africa offer long-term demand but often involve currency risk, utility credit risk, tender complexity and uneven service infrastructure.

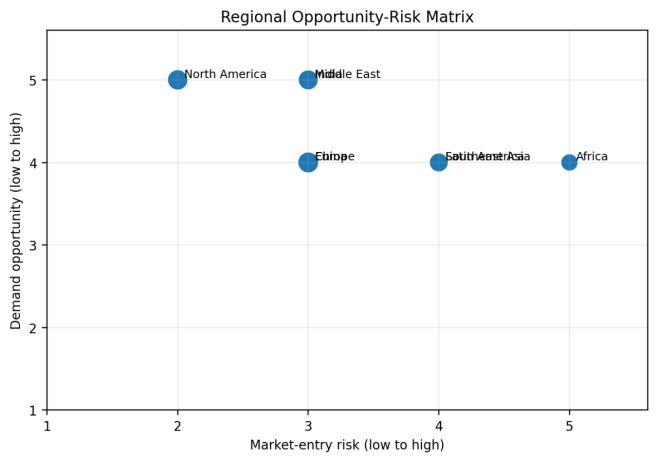

Figure 4. Regional opportunity-risk matrix

Source: Analyst assessment based on demand drivers, standards, localization needs, financing conditions and channel barriers.

5. Technology and Product Evolution

Figure 5. Indicative market mix by voltage class

Source: Medium-voltage share from Fortune Business Insights; remaining shares are an analyst normalization for directional comparison.

5.1 Vacuum technology remains the medium-voltage standard

Vacuum interruption combines long electrical life, low maintenance and strong performance for medium-voltage applications. It is well established in primary and secondary distribution, industrial plants, renewable substations and infrastructure. Product differentiation increasingly centers on embedded sensors, maintenance-free mechanisms, compact switchgear integration and digital diagnostics.

5.2 High-voltage transition away from SF6

SF6 has excellent dielectric and arc-quenching properties but a very high global-warming potential. Utilities and manufacturers are therefore developing vacuum and alternative-gas solutions. Adoption will be fastest where regulation and utility procurement policies are strongest, but the transition requires proven ratings, installed-base confidence, service procedures and lifecycle evidence.

5.3 Digital trip units and connected protection

Low-voltage breakers are evolving from electromechanical protection devices into connected nodes. Electronic trip units can provide adjustable protection curves, energy measurements, event logs, remote status, predictive indicators and communication with building or power-management systems. The value proposition is strongest where downtime, energy quality or arc-flash exposure is costly.

5.4 DC, hybrid and solid-state breakers

DC faults do not naturally pass through a current zero, making interruption more difficult. Mechanical DC breakers remain common, while hybrid breakers combine mechanical contacts with power electronics to improve speed. Solid-state circuit breakers can interrupt faults extremely quickly and enable software-defined protection, but conduction losses, thermal management and cost remain obstacles. ABB has introduced a fully IEC 60947-2-certified solid-state circuit breaker, and UL 489I provides a certification pathway for solid-state molded-case devices in North America.

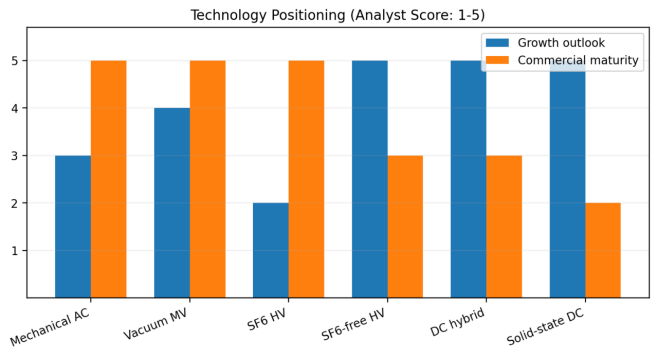

Figure 6. Technology positioning across the breaker landscape

Source: Analyst synthesis; scores are qualitative and intended for strategic comparison, not technical qualification.

|

Technology |

Strengths |

Limitations |

Best-fit markets |

|

Thermal-magnetic mechanical |

Low cost, proven, broad channel availability |

Limited diagnostics and adjustability |

Residential and standard commercial |

|

Electronic-trip MCCB/ACB |

Selective coordination, monitoring, communications |

Higher cost and configuration complexity |

Data centers, industrial and critical buildings |

|

Vacuum MV |

Long life, low maintenance, established supply chain |

Requires engineered switchgear integration |

Distribution, renewables, industrial substations |

|

SF6 HV |

High performance and compactness |

Environmental pressure and lifecycle controls |

Existing high-voltage installed base |

|

SF6-free HV |

Lower climate impact and regulatory alignment |

Qualification, footprint and portfolio maturity |

European and sustainability-led utility projects |

|

Hybrid/solid-state DC |

Very fast interruption and controllability |

Cost, losses, cooling and evolving standards |

Battery storage, DC microgrids, advanced transport |

6. Cost and Pricing Trends

Circuit breaker pricing varies by orders of magnitude, from commodity residential MCBs to engineered high-voltage breakers. The most important cost inputs include copper and silver-based contact materials, steel, molded engineering plastics, vacuum interrupters, electronic trip units, power semiconductors, precision mechanisms, testing and certification. For medium- and high-voltage equipment, project engineering, factory acceptance testing, transport, installation and long-term service materially affect total cost.

Price pressure is most intense in standardized low-voltage products, particularly where local brands have established distribution. In contrast, data-center, utility and industrial buyers often prioritize interrupting capacity, coordination, reliability, delivery time and installed-base compatibility. Recent IEA analysis notes that prices and procurement times for major transmission components such as transformers and cables have nearly doubled over four years. Circuit breakers are not quantified separately in that statement, but the same grid investment wave is tightening qualified manufacturing and engineering capacity across the transmission supply chain.

The likely 2026-2030 pricing pattern is therefore bifurcated: commodity low-voltage products should remain competitive and increasingly localized, while engineered medium-voltage, high-voltage, digital and DC products retain stronger pricing because of certification, project risk and limited qualified supply.

7. Competitive Landscape

The market is led by diversified electrical groups with global certification portfolios, panel and switchgear integration, utility relationships and service networks. Key competitors include ABB, Schneider Electric, Eaton, Siemens, Mitsubishi Electric, Hitachi Energy, Fuji Electric, Toshiba, GE Vernova in selected high-voltage applications, and numerous strong regional manufacturers. Competitive position differs sharply by voltage class and geography; there is no single global share ranking that accurately represents every breaker category.

|

Competitive group |

Representative companies |

Core advantages |

Main challenge |

|

Global diversified leaders |

ABB, Schneider Electric, Eaton, Siemens |

Broad portfolio, channels, digital platforms, service and certification |

High cost base and portfolio complexity |

|

High-voltage specialists |

Hitachi Energy, Mitsubishi Electric, Siemens Energy and others |

Utility qualification, engineering depth, installed base |

Long project cycles and technology-transition risk |

|

Regional industrial leaders |

LS Electric, Hyundai Electric, Fuji Electric, Chint, Delixi and others |

Cost, localization, regional channels |

Global certification and service consistency |

|

Niche technology firms |

DC protection and solid-state specialists |

Fast innovation and application focus |

Scale, bankability and qualification |

主要供应商的财务业绩证实了当前良好的经济周期。施耐德电气公布2025年营收为401.5亿欧元,同比增长8.9%,其中能源管理业务同比增长11%。伊顿公司报告称,其电气业务在2025年及2026年初的业绩将创历史新高。这些数据涵盖了广泛的电气产品组合,但也表明,在断路器所在的系统中,各厂商都在大力投资。

8. 国际采购和市场准入

断路器是安全关键产品,因此市场准入不仅仅取决于价格。供应商应确保产品符合适用的标准和认证体系。IEC 60947-2 是低压工业断路器的核心标准,IEC 60898 涵盖家用及类似微型断路器 (MCB) 应用,IEC 62271-100 涵盖 1 kV 以上的交流断路器,而北美产品通常需要符合 UL 489 或相关标准,并与美国国家电气规范 (NEC) 的要求相协调。

切实可行的全球市场准入策略应包括:经认证的产品系列而非单一型号;与本地配电盘和开关设备的兼容性;已公布的时间-电流曲线和协调数据;本地技术支持;清晰的备件政策;现场服务或授权合作伙伴;以及以客户工程语言编写的文档。对于公用事业公司和大型工业用户而言,参考项目和故障测试数据往往至关重要。

|

买家类型 |

主要采购标准 |

通用商业模式 |

|

公用事业 |

可靠性、型式试验、生命周期、已安装基础兼容性 |

框架协议、合格供应商名单、项目招标 |

|

面板制造商/OEM厂商 |

尺寸、配件、协调数据、价格和供货情况 |

分销商或直接OEM供货 |

|

数据中心 |

选择性协调、电弧闪光缓解、监测、正常运行时间 |

工程系统和经认证的产品平台 |

|

工业厂房 |

坚固性、可维护性、备件、工艺连续性 |

项目采购及服务合同 |

|

住宅/商业频道 |

品牌认知度、代码合规性、供货情况和价格 |

批发、零售和安装商分销 |

9. 风险

- 认证风险:符合某一标准的产品,未经额外测试可能无法在另一个市场获得认可。

- 产品责任风险:防护措施失效可能导致火灾、设备损失、人身伤害和重大法律责任。

- 技术转型风险:SF6 限制和直流电快速创新可能会缩短产品开发周期。

- 价格和渠道风险:标准化低压产品面临激烈的本地竞争和分销商的议价能力。

- 供应链风险:银触点、铜、电子元件、真空断路器和专用机械装置可能会限制产量。

- 项目风险:公用事业和基础设施订单可能会因许可、融资、电网研究或土建工程而延误。

- 网络安全风险:联网的行程单元和远程操作功能对安全设计和更新提出了新的要求。

- 服务风险:本地备件不足和技术响应能力不足可能会导致原本具有竞争力的供应商失去资格。

10. 2030 年展望

到2030年,断路器市场结构性增长预计将保持良好态势,但增长并非均衡。低压建设和配电领域销量将持续增长,而价值增长将集中在中压电网设备、高规格低压系统、无SF6高压解决方案、直流保护和互联产品领域。需求最强劲的领域将是那些负荷快速增长但电网基础设施受限的领域,例如数据中心集群、可再生能源和储能枢纽、工业走廊、城市交通系统以及快速增长的新兴市场网络。

对于全球制造商而言,战略重点在于构建多层次的产品组合。标准产品能够扩大规模并拓展渠道;数字化和高分断能力产品能够提升利润率;工程化的中高压产品能够建立长期的客户关系;而直流或固态产品则能够创造未来的选择价值。将这些产品层次与本地认证、面板集成和服务相结合的公司,将比仅依靠出厂价格竞争的供应商更具优势。

结论

断路器作为一种成熟的产品类别,正步入新的投资时代。电气化正在扩大其装机量,而数字化和直流架构则正在改变保护装置的技术内涵。全球市场增长率可能仍将保持在个位数中段,但技术驱动的细分市场增长速度可能更快。竞争格局的核心转变在于,从销售断路器转向提供经过验证的保护系统:该系统集成了硬件、传感、通信、软件、文档和全生命周期服务。这种转变既为成熟的全球领导者创造了机遇,也为专业领域的后起之秀带来了机遇,同时也提高了认证、工程设计和本地化实施的标准。