Executive Summary

Global demand for switchgear cabinets is entering a sustained expansion cycle. Grid reinforcement, renewable integration, industrial electrification, electric-vehicle infrastructure and the rapid construction of data centers are increasing demand for low-voltage switchboards, medium-voltage metal-clad switchgear, ring main units, motor control centers and customized distribution cabinets.

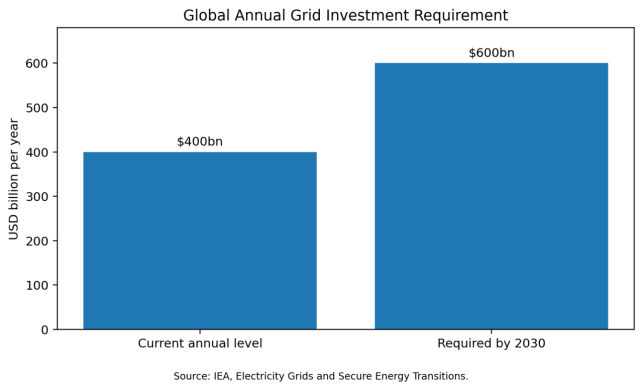

The International Energy Agency estimates that annual global grid investment must rise from roughly USD 400 billion to more than USD 600 billion by 2030. This investment directly supports demand for new substations, feeder panels, protection systems and distribution cabinets. At the same time, supply pressure remains concentrated in circuit breakers, vacuum interrupters, protection relays, copper busbars, instrument transformers and high-power testing capacity.

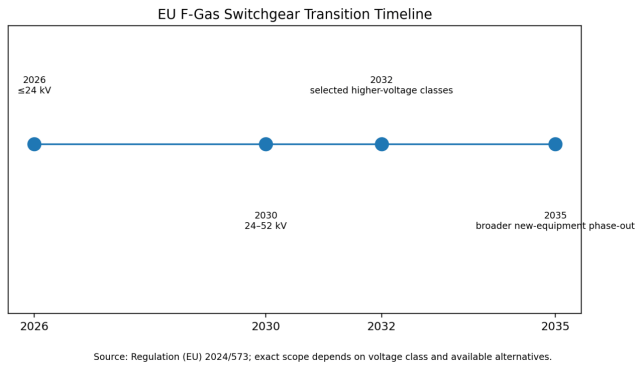

The market is also being reshaped by environmental regulation. In the European Union, Regulation (EU) 2024/573 began restricting new medium-voltage switchgear up to and including 24 kV from 1 January 2026, accelerating the transition from SF₆-based equipment toward vacuum interruption, pure air and other low-GWP insulation systems.

For international buyers, the key decision is no longer the factory price of an empty enclosure. The real economic value of a switchgear cabinet depends on verified short-circuit performance, internal arc classification, breaker quality, digital protection, service continuity, installation scope, spare-part support and compliance with the destination market.

Key Findings

- Grid expansion creates a structural demand base for LV and MV switchgear cabinets through 2030.

- Data centers are becoming one of the fastest-growing end markets for high-current LV boards and MV metal-clad lineups.

- EU F-gas rules are accelerating procurement of SF₆-free medium-voltage cabinets.

- Breaker platforms, relays, busbar materials and type-test capacity are more important cost drivers than the sheet-metal enclosure alone.

- International price comparisons are often misleading because quotations differ in protection, communication, testing, installation and commissioning scope.

- Chinese manufacturers have strong cost and production advantages, but export success depends on IEC/UL compliance, documented type tests, local service and bankable delivery.

- Lifecycle value increasingly depends on uptime, maintainability, arc safety, digital support and spare-part strategy.

Figure 1. Global annual grid investment requirement.

1. Product Scope and Market Definition

Switchgear cabinet is a practical market term covering factory-assembled electrical enclosures that contain switching, protection, metering and control devices. The category includes low-voltage switchboards, medium-voltage metal-clad switchgear, ring main units, motor control centers, distribution boards and project-specific control cabinets.

The product boundary varies widely. Some suppliers quote only the metal enclosure and installed components. Others provide a fully engineered lineup including protection settings, IEC 61850 communication, bus duct interfaces, batteries, control cables, factory acceptance testing, site supervision and commissioning. This variation is why a single global average price per panel is not commercially reliable.

Low-voltage cabinets typically serve buildings, factories, hospitals and data centers. Medium-voltage cabinets serve utility distribution, renewable plants, mining, rail, oil and gas and heavy industry. Ring main units are widely used in urban distribution and renewable collection systems. Motor control centers are tied closely to process industries and water infrastructure.

|

Cabinet Type |

Typical Application |

Main Buying Criteria |

Current Market Direction |

|

LV switchboard |

Data centers, commercial buildings, factories |

Fault rating, arc resistance, busbar temperature, modularity |

Higher current density and digital metering |

|

MV metal-clad cabinet |

Utilities, industrial plants, renewable substations |

Internal arc class, breaker reliability, continuity of service |

Vacuum interruption and SF₆-free insulation |

|

Ring main unit |

Urban distribution, wind and solar collection |

Compactness, automation, environmental sealing |

Remote control and low-GWP insulation |

|

Motor control center |

Water, mining, petrochemical, manufacturing |

Motor protection, maintainability, intelligent starters |

Smart diagnostics and energy monitoring |

|

Control and protection cabinet |

Substations and process plants |

Relay architecture, communication, cybersecurity |

IEC 61850 and condition monitoring |

2. Global Demand Drivers

The strongest demand driver is grid investment. The IEA projects that annual grid spending must exceed USD 600 billion by 2030 to support electrification and energy-transition goals. Every expansion of distribution or transmission infrastructure requires switching, isolation, protection and control equipment.

Data centers are a second major growth engine. Large facilities require redundant MV intake, double-ended LV distribution, high-fault-duty boards, generator synchronization, UPS integration and extensive monitoring. Eaton announced in April 2026 that it would build a new 370,000-square-foot U.S. facility dedicated to medium-voltage switchgear, explicitly linking the expansion to the AI data-center boom.

Renewables and storage also increase cabinet demand. Solar, wind and battery projects require collection switchgear, auxiliary boards, protection cabinets and grid-interconnection equipment. Bidirectional power flow, harmonics and fast-changing operating modes raise the value of advanced protection and communication.

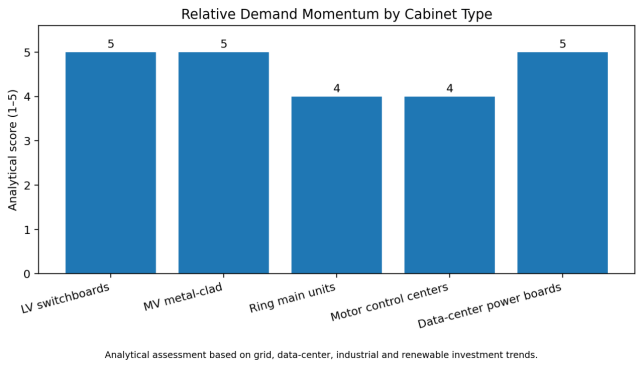

Figure 2. Relative demand momentum by cabinet type.

3. Regional Market Analysis

3.1 North America

The U.S. and Canada are attractive but qualification-intensive markets. Demand is being driven by data centers, manufacturing reshoring, utility modernization and renewable interconnection. ANSI/IEEE ratings, UL listing, arc-resistant construction and local service are central. New entrants face barriers from approved-vendor lists, product-liability exposure and domestic-content preferences.

3.2 Europe

Europe combines high grid investment with the fastest regulatory shift away from SF₆. Utilities are revising framework agreements toward pure-air and vacuum-based MV cabinets. IEC compliance alone is not enough; buyers also evaluate environmental declarations, gas-management obligations, digital interoperability and lifecycle service.

3.3 China and Asia-Pacific

China has a broad and cost-competitive manufacturing base for LV and MV cabinets, vacuum breakers, ring main units and digital protection. India and Southeast Asia are growing through industrialization and grid expansion, while Japan, South Korea and Australia remain high-specification markets with demanding utility qualification.

3.4 Middle East and Africa

The Middle East is supported by utility expansion, oil and gas, desalination, rail, data centers and renewable megaprojects. High ambient temperature, dust, corrosion and localization rules materially affect cabinet design. Africa offers long-term growth but project finance, currency risk and local service remain constraints.

3.5 Latin America

Demand is tied to transmission programs, mining, renewable generation and urban distribution replacement. Brazil, Mexico, Chile, Colombia and Peru are important markets. High altitude, mining dust, seismic duty and spare-parts access are common project considerations.

4. Technology Transition and Product Development

The most important medium-voltage technology transition is the move away from SF₆. Vacuum interruption is already mature, while pure air, dry air and solid insulation are increasingly used for dielectric performance. The EU timetable creates a clear commercial incentive for suppliers with type-tested SF₆-free cabinet platforms.

Digital switchgear cabinets use sensors, intelligent electronic devices and communication networks to reduce conventional wiring and improve monitoring. IEC 61850 allows interoperable protection and control, while online monitoring can track breaker timing, temperature, partial discharge and operating mechanism condition.

Arc safety is also gaining importance. Internal arc classification, pressure relief, remote racking, zone-selective interlocking and arc-flash detection can raise initial cost but materially reduce personnel and outage risk.

Figure 3. EU F-gas switchgear transition timeline.

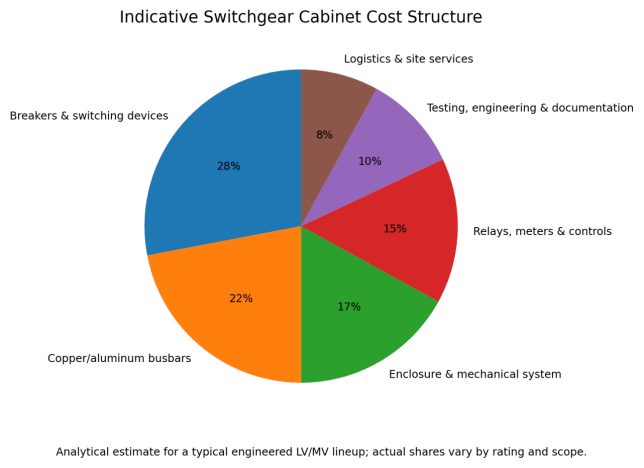

5. Price and Cost Structure

Cabinet pricing depends on far more than enclosure size. Continuous current, short-circuit rating, breaker type, busbar metal, withdrawable or fixed construction, internal arc class, relay brand, communication scope and testing requirements can change the price significantly.

The circuit breaker and switching devices are often the largest functional cost item. Copper or aluminum busbars form another major share. Protection relays, meters and communication gateways are increasingly important as projects become more digital. Engineering, documentation and testing costs rise sharply for customized or utility-qualified designs.

SF₆-free cabinets may carry an initial premium where the technology is new or production scale is limited. However, buyers should also consider avoided gas handling, leakage management, technician training and future regulatory risk.

Figure 4. Indicative switchgear cabinet cost structure.

6. Supply Chain and Manufacturing Constraints

Critical supply items include vacuum interrupters, breakers, instrument transformers, protection relays, current sensors, molded insulation, operating mechanisms and copper busbars. A delay in one qualified component can hold up the entire lineup.

Manufacturing bottlenecks include sheet-metal fabrication, busbar processing, breaker assembly, wiring, dielectric testing, temperature-rise validation and customer witness testing. High-power short-circuit test capacity is particularly important because test evidence must match the offered configuration.

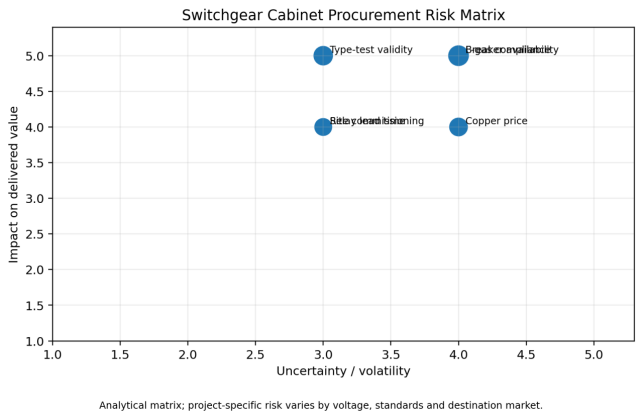

International projects add logistics and site-integration risk. Cabinets may need split shipment, moisture-controlled packing, bus-joint assembly, protection setting, primary injection and commissioning. Contract boundaries should clearly assign these responsibilities.

Figure 5. Switchgear cabinet procurement risk matrix.

7. Standards and Certification

|

Market / Product |

Key Standards |

Main Procurement Risk |

|

IEC LV assemblies |

IEC 61439 |

Confusing certified components with verified assembly performance |

|

IEC MV switchgear |

IEC 62271 series |

Using type-test evidence for a materially different configuration |

|

North America |

ANSI/IEEE and UL requirements |

Offering IEC designs without required NRTL approvals |

|

Digital systems |

IEC 61850 and cybersecurity requirements |

Interoperability and firmware-support gaps |

|

EU environmental compliance |

Regulation (EU) 2024/573 |

Selecting equipment incompatible with commissioning date |

Type-test documentation should be checked against the actual cabinet width, breaker platform, busbar rating, enclosure construction, internal arc class and short-circuit level. A certificate for a related product family may not cover the offered configuration.

8. Competitive Landscape

The global market includes ABB, Siemens, Schneider Electric, Eaton, Hitachi Energy, Mitsubishi Electric, GE Vernova and strong regional and Chinese manufacturers. Competition differs by segment: LV cabinets are more fragmented and channel-driven, while MV metal-clad and utility-qualified cabinets require deeper engineering and testing.

Competition is shifting toward capacity, delivery reliability, SF₆-free portfolios, digital integration and lifecycle service. Data-center buyers favor standardized repeatable designs and short schedules. Utilities increasingly use multi-year framework agreements to secure manufacturing slots.

Chinese suppliers remain highly competitive in factory price and production scale. Their main export challenges are destination-market certification, high-power test evidence, documentation quality, utility bankability and local after-sales service.

9. Total Cost of Ownership

TCO = Purchase + Engineering + Logistics + Installation + Energy Losses + Maintenance + Compliance + Outage Risk − Residual Value

A lower-priced cabinet can become expensive if it causes a delayed energization, requires redesign, lacks local spares or fails to meet type-test requirements. For data centers, hospitals and process plants, outage cost may exceed equipment price within hours.

Withdrawable construction may improve maintainability but increase cost and footprint. Fixed-breaker designs can be economical for less critical applications. GIS or compact insulated cabinets can reduce building space, while air-insulated cabinets may simplify inspection and end-of-life handling.

Lifecycle evaluation should include breaker endurance, relay obsolescence, spare mechanisms, busbar losses, maintenance intervals and expected expansion.

10. International Procurement Recommendations

- Define the complete technical and commercial boundary before comparing quotations.

- Standardize current ratings, short-circuit levels and relay families where possible.

- Verify that type tests apply to the offered cabinet configuration.

- Confirm destination-market standards, UL/NRTL requirements and utility approvals.

- Evaluate SF₆ compliance based on the commissioning date, not only the order date.

- Audit critical sub-suppliers for breakers, interrupters, relays and instrument transformers.

- Separate factory price from freight, installation, commissioning and site testing.

- Score the supplier's delivery backlog, test-slot availability and recent on-time performance.

- Price spare breakers, coils, relays and local service at the award stage.

- Use design review, factory inspections, FAT and documented site acceptance testing.

11. Market Outlook, 2026–2030

The global outlook remains favorable because grid investment, data-center construction, renewable projects and industrial electrification are all expanding simultaneously. Capacity additions will reduce pressure in some standardized product categories, but qualified MV lineups and custom high-current LV boards will remain schedule-sensitive.

Europe will lead the SF₆-free transition, while other regions will adopt similar technologies through utility decarbonization policies and supplier standardization. Digital protection and monitoring will become standard in more projects, especially where uptime and remote operation carry high value.

Price competition will remain intense, but the most attractive margin pools will shift toward engineered solutions, fast delivery, arc-safety performance, digital integration and lifecycle service.

Conclusion

The global switchgear cabinet market is benefiting from a structural expansion in electrical infrastructure. The strongest opportunities lie not in empty enclosures, but in qualified, safe, digitally integrated and regulation-ready assemblies.

For buyers, the correct comparison is delivered lifecycle value rather than panel price. For suppliers, international competitiveness depends on verified performance, standards compliance, manufacturing capacity, documentation and local service.