Executive Summary

The electrostatic precipitator (ESP) market is not a simple extension of the coal-power equipment cycle. New coal-fired capacity is becoming more geographically concentrated, while the commercially important opportunity is shifting toward industrial installations, performance upgrades, high-frequency power supplies, wet ESPs and hybrid systems. Published research places the global market at roughly USD 9–10 billion in 2024–2025, with most current forecasts implying a 5.2–6.4% compound annual growth rate through 2030 or 2034. Differences between estimates reflect whether reports include aftermarket services, power electronics, wet systems and full project scope.

|

Finding |

Assessment |

|

Market range |

Most current estimates cluster around USD 9–10 billion in 2024–2025. Forecast endpoints range from USD 12.25–12.70 billion in 2030 to USD 16.70–16.92 billion in 2034. |

|

Demand centre |

Asia-Pacific remains the largest and fastest-growing region, supported by coal-fleet retrofits, steel and cement output, waste-to-energy development and tighter particulate limits. |

|

Technology direction |

Dry ESPs retain the installed-base advantage; wet ESPs gain in acid mist, ultrafine particulate and post-FGD polishing. Hybrid ESP–fabric-filter configurations are increasingly used when dust properties vary. |

|

Commercial model |

Retrofit engineering, controls, transformer-rectifier upgrades, electrode renewal, digital monitoring and lifecycle service are becoming more defensible revenue pools than commodity steelwork alone. |

|

Competitive pressure |

Baghouses can achieve consistently low outlet dust levels and are often preferred for variable-resistivity dust, but ESPs retain advantages in low pressure drop, large gas volumes, high temperatures and long filter-media life. |

|

Strategic risk |

Coal retirement in advanced economies limits greenfield utility demand. Suppliers that remain concentrated in conventional coal-power projects face higher order volatility than companies serving steel, cement, biomass, waste-to-energy and industrial process markets. |

The decisive procurement issue is no longer whether an ESP can remove bulk particulate matter. The U.S. Environmental Protection Agency states that ESPs can exceed 99% collection efficiency. The investment question is whether the selected configuration can sustain the guaranteed outlet concentration across changing fuel, ash resistivity, process load, gas temperature and maintenance conditions. This shifts value toward process characterization, gas-distribution design, high-voltage controls, emissions monitoring and guaranteed retrofit performance.

1. Scope and Market Definition

An electrostatic precipitator removes suspended particles by charging them in a high-voltage electric field and driving the charged particles toward collecting surfaces. Dry units remove deposited dust by rapping; wet units wash the collecting surfaces. The core assembly includes gas-distribution devices, discharge electrodes, collecting plates or tubes, rappers or wash systems, hoppers, transformer-rectifier sets, insulation, controls and structural casing.

This report treats the market as the sale and modernization of ESP equipment, electrical and control systems, internals, monitoring integration and associated engineering or service. It does not equate the ESP market with the broader flue-gas treatment or air-quality-control-system market, which may also include flue-gas desulfurization, selective catalytic reduction, fabric filtration, mercury control and heat recovery.

|

Configuration |

Typical applications |

Primary advantage |

Main limitation |

|

Dry plate-wire ESP |

Power generation, cement, steel, pulp and paper, biomass |

Large gas volumes; low pressure drop; dry dust recovery |

Sensitive to dust resistivity, gas distribution and rapping re-entrainment |

|

Dry tubular ESP |

Smaller process streams, chemical and specialty applications |

Compact geometry; suited to selected gas streams |

Less common at very large utility scale |

|

Wet ESP |

Acid mist, ultrafine PM, metal fumes, post-scrubber polishing |

No rapping re-entrainment; effective for sticky or low-resistivity aerosols |

Water handling, corrosion materials and wastewater management |

|

Hybrid ESP + fabric filter |

Retrofits requiring lower outlet limits under variable dust conditions |

Combines low pressure drop and bulk capture with final filtration |

Higher integration complexity and fabric replacement requirements |

|

High-frequency power/control retrofit |

Existing ESPs with electrical limitation or unstable corona power |

Can improve collection without major casing expansion |

Performance still constrained by mechanical condition and gas distribution |

Technical basis: U.S. EPA; ANDRITZ; Mitsubishi Heavy Industries. Configuration suitability must be verified against actual gas and dust properties.

In procurement databases, ESPs are most appropriately grouped under particulate matter capture rather than under generic ventilation equipment, because collection guarantees depend on particulate chemistry, resistivity and process integration.

2. Global Market Size and Forecast

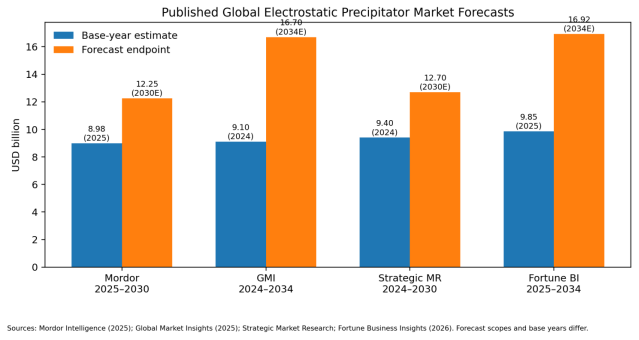

Four current published estimates show a relatively tight base-year range but a wider forecast horizon. Mordor Intelligence estimates USD 8.98 billion in 2025 and USD 12.25 billion by 2030. Global Market Insights reports USD 9.1 billion in 2024 and USD 16.7 billion by 2034. Strategic Market Research reports USD 9.4 billion in 2024 and USD 12.7 billion by 2030. Fortune Business Insights estimates USD 9.85 billion in 2025 and USD 16.92 billion by 2034. The corresponding reported growth rates range from 5.2% to 6.4%.

Figure 1. Published global ESP market forecasts

The consistency of the base-year estimates supports a working 2025 market range of approximately USD 9.0–9.9 billion. Forecast dispersion is more important than the apparent precision of any single figure. Reports with higher endpoints generally include a longer forecast period and may capture a larger share of aftermarket upgrades, wet ESPs, power supplies, digital controls and service revenue. A market participant should therefore compare addressable product scope rather than treating all headline values as directly interchangeable.

|

Source |

Base year |

Base USD bn |

Forecast year |

Forecast USD bn |

CAGR |

Reported emphasis |

|

Mordor Intelligence |

2025 |

8.98 |

2030E |

12.25 |

6.40% |

Asia-Pacific largest and fastest-growing |

|

Global Market Insights |

2024 |

9.10 |

2034E |

16.70 |

6.10% |

Industrialization, upgrades and regulation |

|

Strategic Market Research |

2024 |

9.40 |

2030E |

12.70 |

5.20% |

Global equipment and applications |

|

Fortune Business Insights |

2025 |

9.85 |

2034E |

16.92 |

6.19% |

Wet ESP growth and modernization demand |

The figures are third-party market estimates and should be used as a triangulated range. Scope, currency assumptions and aftermarket inclusion differ.

Market structure: new-build versus installed-base revenue

The installed base is strategically more important than unit shipment counts suggest. ESP casings and structural shells can remain in service for decades, while electrodes, rappers, insulators, hoppers, control cabinets and transformer-rectifier sets require inspection, replacement or modernization. Tightened emission limits often create projects in which the original casing is retained but internals, gas distribution, electrical energization and downstream polishing are upgraded. These projects carry higher engineering content than standardized new-build supply and can offer stronger service margins.

3. Demand Drivers and Structural Constraints

3.1 Particulate regulation and continuous compliance

Regulation remains the strongest demand driver, but compliance is moving from initial equipment installation to continuous performance assurance. The U.S. EPA identifies outlet particulate concentration, opacity, secondary voltage and current, spark rate, gas temperature, gas flow and rapper operation as key ESP performance indicators. This supports demand not only for collectors but also for online diagnostics, emissions monitoring, controls and maintenance services.

As compliance becomes data-driven, the commercial boundary between the precipitator and flue-gas emission monitoring narrows. Suppliers able to integrate CEMS data, field-level electrical signals and predictive maintenance can offer performance-based service rather than one-off hardware.

3.2 Coal power: declining share, persistent installed base

Coal remains a major source of electricity and therefore a large installed-base market for ESPs, even as its global share declines. The International Energy Agency reported coal at about 35% of global electricity generation in 2024 and forecasts its share falling from around 34% in 2025 to 27% by 2030. This is not a uniform retreat: coal remains dominant in parts of Asia, while advanced economies continue retirements. The resulting market is bifurcated—retrofits and reliability work in existing fleets, selective new-build activity in emerging markets, and declining greenfield demand in Europe and parts of North America.

3.3 Heavy industry as the stabilizing demand base

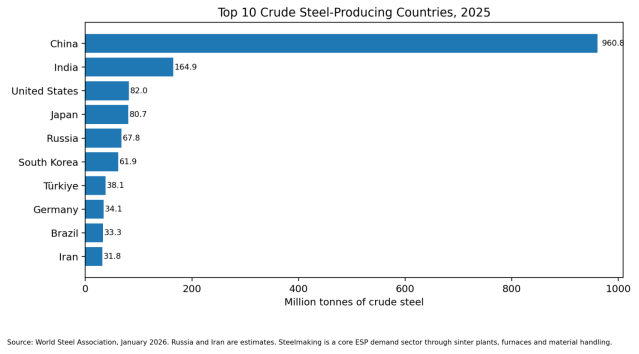

Steel, cement, non-ferrous metals, pulp and paper, biomass and waste-to-energy plants create a broader and more durable market than coal power alone. World crude steel production reached approximately 1.85 billion tonnes in 2025. China and India together accounted for more than 60% of the total, placing a large share of sinter, blast-furnace, basic-oxygen-furnace and material-handling dust-control demand in Asia.

Figure 2. Top crude steel producers and the geographic concentration of ESP demand

The steel chart is not a direct measure of ESP revenue, because technology selection varies by process and plant age. It is nevertheless a strong demand-location proxy. India’s 10.4% increase in crude steel output in 2025 contrasts with declines in China, Japan, Russia and Germany, indicating where new process capacity and associated dust-control investment are more likely to develop.

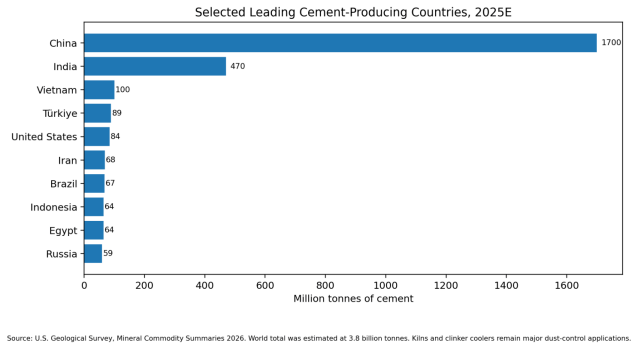

Figure 3. Cement production as a second major demand proxy

Global cement production was estimated at 3.8 billion tonnes in 2025. China remained the dominant producer at roughly 1.7 billion tonnes, followed by India at 470 million tonnes. Cement plants use ESPs and fabric filters across kilns, clinker coolers, raw mills and material handling. The sector’s opportunity is increasingly retrofit-driven: operators must meet lower dust limits while changing fuels, increasing alternative-fuel use and optimizing heat recovery, all of which can alter gas conditions and dust resistivity.

3.4 Structural constraints

|

Constraint |

Market effect |

Supplier response |

|

Coal retirements |

Reduces greenfield utility ESP orders in advanced economies |

Diversify into industrial and service markets |

|

Baghouse substitution |

Fabric filters may provide more stable low emissions for difficult dust |

Offer hybrid systems and application-specific guarantees |

|

Commodity fabrication pressure |

Large casings and steelwork can be price-competitive and locally sourced |

Protect value in engineering, internals, controls and service |

|

Project cyclicality |

Utility and heavy-industry capital spending is lumpy |

Build aftermarket, inspections and spare-parts revenue |

|

Local-content requirements |

Regional procurement may favor domestic fabrication and EPC partners |

Use licensing, local assembly and technology partnerships |

|

Process variability |

Fuel switching and changing production rates can degrade legacy performance |

Use gas conditioning, adaptive controls and digital diagnostics |

4. Technology Landscape and Competitive Substitution

4.1 Why collection efficiency alone is an incomplete specification

The EPA notes that ESPs can achieve collection efficiencies above 99%, but a percentage specification alone can be misleading. A unit removing 99.5% from an inlet loading of 20,000 mg/Nm³ still emits 100 mg/Nm³. Procurement should therefore specify both mass efficiency and guaranteed outlet concentration, together with reference gas flow, temperature, moisture, oxygen content and dust properties.

Particle resistivity is a central design variable. High-resistivity dust can create back corona and suppress the electric field; very low-resistivity dust can lose charge rapidly and re-enter the gas stream. Gas distribution, electrode alignment, rapping intensity and electrical control must be treated as one system. High-frequency energization can increase average corona power and stabilize operation, but it cannot compensate for severe mechanical deterioration or poor gas flow distribution.

The electrical package is not a generic auxiliary. Each field is energized through a transformer-rectifier arrangement; procurement teams assessing a transformer or high-frequency power supply must verify voltage-current characteristics, control logic, insulation coordination, harmonic behavior and compatibility with the existing electrode geometry.

4.2 Dry ESP, wet ESP and fabric filter competition

|

Selection factor |

Dry ESP |

Wet ESP |

Fabric filter |

|

Large gas volume |

Strong |

Moderate |

Strong |

|

Pressure drop |

Low |

Low to moderate |

Higher |

|

Very fine PM / mist |

Moderate without optimization |

Strong |

Strong for solid PM; limited for liquid mist |

|

Sticky particles |

Weak to moderate |

Strong |

Depends on media and cleaning |

|

High temperature |

Strong within material limits |

Usually downstream at lower temperature |

Media-dependent |

|

Water use |

None in collector |

Required |

None in collector |

|

Consumables |

Low |

Water treatment and corrosion materials |

Filter bags and cages |

|

Sensitivity to resistivity |

High |

Lower for washed surfaces |

Not electrostatic |

|

Footprint in retrofit |

Can be large unless internals/electricals are upgraded |

Often compact polishing stage |

Can be constrained by casing and bag length |

Qualitative assessment based on EPA and supplier technical literature. Final selection requires process-specific testing and guarantee conditions.

4.3 Retrofit technologies are reshaping the addressable market

Retrofit engineering can deliver material performance improvements without replacing the entire shell. Solutions include improved discharge electrodes, moving collecting electrodes, upgraded rapping, gas-distribution correction, high-frequency power supplies, sulfur trioxide or ammonia conditioning where permitted, flue-gas cooling, additional electrical fields, and downstream wet or fabric-filter polishing.

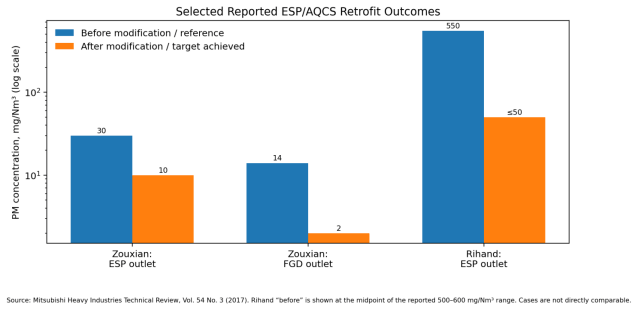

Figure 4. Selected reported performance improvements from integrated retrofit projects

Mitsubishi Heavy Industries reported that a 1,000 MW Chinese project reduced PM at the ESP outlet from 30 to 10 mg/Nm³ and at the downstream FGD outlet from 14 to 2 mg/Nm³. At India’s Rihand plant, a moving-electrode retrofit using the existing space reduced the ESP outlet from a reported 500–600 mg/Nm³ to 50 mg/Nm³ or less. These results show why retrofit design must address the whole gas-cleaning train rather than treating the ESP as an isolated box.

5. End-Use Industry Analysis

|

End-use sector |

Process characteristics |

Commercial opportunity |

Principal risk |

|

Coal-fired power |

Very large gas volumes, fly ash, long operating hours |

Retrofit, high-frequency power, internals, gas conditioning, hybrid polishing |

Fleet retirement and uncertain utilization |

|

Steel and iron |

Sintering, BOF/EAF fumes, high and variable dust loading |

Wet ESP for fine fumes; process-specific dry ESP; secondary dedusting |

Cyclic steel investment and difficult dust chemistry |

|

Cement and lime |

Kilns, clinker coolers, raw mills and bypass gas |

Conversions, electrical upgrades, hybrid filters, alternative-fuel adaptation |

Fabric-filter substitution and temperature/moisture swings |

|

Biomass and waste-to-energy |

Variable fuels, salts, acid mist and fine PM |

WESP polishing, corrosion-resistant materials, integrated multipollutant systems |

Feedstock variability and corrosion |

|

Pulp and paper |

Recovery boilers and process gas |

Dry ESP service, internals, power supplies and ash recovery |

Mill consolidation and local service requirements |

|

Non-ferrous metals |

Metal fumes, smelter dust and acid mist |

WESP and specialized corrosion-resistant systems |

Hazardous dust handling and project-specific metallurgy |

Power generation

Utility ESPs remain the largest installed-base service opportunity because of their scale, multiple electrical fields and long operating lives. However, the revenue mix is moving away from simple new-build units. Owners increasingly procure diagnostic testing, electrode replacement, control upgrades and guaranteed outlet-emission retrofits. The best-positioned suppliers can coordinate ESP performance with boilers, air preheaters, gas-gas heaters, flue-gas desulfurization and induced-draft fans.

Pressure-drop and gas-flow decisions also affect the centrifugal fan and the wider draft system. A low-pressure-drop ESP can preserve auxiliary power advantages, but flow maldistribution or leakage can eliminate those benefits.

Steel and cement

In steelmaking, the highest-value applications are often process-specific rather than standardized. Sinter dust, BOF gas and non-ferrous fumes differ in temperature, resistivity, particle size and explosibility. Wet systems can be attractive for ultrafine fumes and mist, while dry ESPs remain relevant where recoverable dry dust has process value. In cement, the technology battle with fabric filters is more direct. ESPs remain attractive where low pressure drop, high gas temperature and long life dominate, but baghouses can provide more predictable very-low emissions under variable dust resistivity. Hybrid conversion is therefore an important retrofit route.

6. Regional Market Outlook

|

Region |

Market position |

Demand drivers |

Best opportunities |

Main risk |

|

Asia-Pacific |

Largest and fastest-growing |

Coal-fleet retrofit, dominant steel/cement output, industrial capacity additions |

India growth; China ultra-low-emission maintenance and industrial retrofits |

Price competition and local-content pressure |

|

North America |

Mature, service-intensive |

Aging installed base, industrial compliance, biomass and selected WESP applications |

Controls, aftermarket, upgrades and replacement internals |

Coal retirements and long permitting cycles |

|

Europe |

Mature, regulation-led |

BAT compliance, waste-to-energy, biomass, industrial decarbonization |

Hybrid conversions, WESP polishing, service and efficiency upgrades |

Low greenfield coal demand |

|

Middle East |

Selective growth |

Cement, metals, refining and new industrial zones |

High-temperature and harsh-environment systems |

Project concentration and water constraints for WESP |

|

Latin America |

Moderate, project-driven |

Cement, pulp and paper, mining and metals |

Localized service and brownfield modernization |

Currency and financing volatility |

|

Africa |

Early-stage and uneven |

Cement, mining, metals and selected power projects |

Modular systems and local partnerships |

Financing, maintenance capability and spare-parts logistics |

Asia-Pacific

Asia-Pacific combines the world’s largest heavy-industrial base with the most competitive equipment supply chain. China’s opportunity is increasingly centered on maintenance, industrial ultra-low-emission conversion, digital controls and lifecycle renewal rather than first-time installation at coal plants. India offers a stronger capacity-growth profile in steel and power, but projects are highly price-sensitive and often require local fabrication or licensing. Southeast Asia creates selected opportunities in cement, waste-to-energy, pulp and paper and biomass.

Europe and North America

In Europe and North America, coal-power contraction limits new utility installations but does not eliminate demand. Aging collectors require service, spare parts and compliance upgrades, and wet ESPs are used in selected biomass, waste, acid-mist and industrial applications. Suppliers must demonstrate lifecycle economics, digital monitoring and outage execution rather than relying on low capital price. European BAT requirements also favor integrated solutions able to control multiple pollutants across the full gas-cleaning train.

7. Competitive Landscape and Business Models

The market is moderately concentrated at the technology and large-project level but fragmented in fabrication, service and regional supply. Global engineering groups compete with local EPC contractors, specialized retrofit firms and component suppliers. Market shares are difficult to verify publicly because ESP revenue is often embedded inside environmental systems or service segments. The table therefore describes representative positioning rather than ranking suppliers by unverified share.

|

Supplier group |

Representative offering |

Competitive position |

|

ANDRITZ |

Dry and wet ESPs, hybrid filters, high-frequency power supplies, service |

Broad industrial coverage and retrofit portfolio; positions single-digit PM solutions |

|

Mitsubishi Power / MHI Power Environmental Solutions |

Utility and industrial ESPs, moving-electrode systems, integrated AQCS |

Strong system integration and documented retrofit references in Asia |

|

FLSmidth |

Cement and minerals air-pollution-control equipment and services |

Installed-base access in cement and process industries |

|

Babcock & Wilcox Environmental |

Utility and industrial emissions-control systems, service and upgrades |

North American installed base and power-sector engineering |

|

KC Cottrell and regional Asian suppliers |

ESP, fabric filters and air-pollution-control packages |

Competitive regional fabrication and EPC delivery |

|

Specialist WESP providers |

Tubular and plate wet systems for acid mist and fine PM |

Application specialization and corrosion-material expertise |

|

Local fabricators and service companies |

Casings, electrodes, rappers, hoppers, repairs |

Cost advantage and fast field response; technology depth varies |

Where margins are likely to be defended

|

Revenue pool |

Margin defensibility |

Reason |

|

Process and performance engineering |

High |

Dust characterization, CFD/gas distribution, electrical sizing and guarantees are difficult to commoditize |

|

High-voltage power and controls |

Medium to high |

Retrofit-friendly and increasingly digital; requires reliability and controls expertise |

|

Internals and mechanical retrofit |

Medium |

Engineering differentiation exists, but fabrication is locally competitive |

|

Casing and structural steel |

Low to medium |

High material content and intense price competition |

|

Monitoring and analytics |

Medium to high |

Recurring service potential and direct connection to compliance |

|

Long-term service agreements |

High |

Installed-base knowledge, outage planning and spare-parts availability create switching costs |

8. Cost Structure and Procurement Economics

A reliable global benchmark price for an ESP is not available because cost is dominated by gas volume, inlet loading, collection area, number of fields, materials, structural loads, electrical redundancy, site conditions and guarantee level. Retrofit scope can range from controls replacement to complete internal renewal. Quoting a price per cubic metre per hour without defining these variables can be misleading.

|

Cost element |

Primary sizing variables |

Commercial implication |

|

Casing, support steel and hoppers |

Gas volume, pressure, seismic/wind loads, corrosion allowance |

High material and logistics content |

|

Collecting and discharge systems |

Specific collection area, field count, electrode design, alignment tolerances |

Core performance hardware |

|

Transformer-rectifier / high-frequency power |

Field segmentation, power density, redundancy and controls |

Important retrofit lever; electrical reliability critical |

|

Rapping or washing system |

Dust adhesion, re-entrainment, water quality and nozzle coverage |

Direct effect on sustained performance |

|

Gas distribution and ductwork |

Velocity profile, turning vanes, dampers and leakage |

Poor design can negate collector sizing |

|

Instrumentation and CEMS integration |

Compliance regime, data interfaces and diagnostics |

Growing share of lifecycle value |

|

Installation and outage |

Site congestion, lifting, scaffolding and production shutdown |

Often decisive in brownfield economics |

|

Materials and corrosion protection |

Temperature, chloride, acid dew point and wash-water chemistry |

Major WESP and waste-to-energy cost driver |

Total cost of ownership

The lowest installed price may not minimize lifecycle cost. ESP economics should include auxiliary power, downtime, rapping maintenance, electrode alignment, insulator cleaning, hopper blockages, corrosion, control obsolescence and the cost of non-compliance. Compared with fabric filters, ESPs typically avoid periodic bag replacement and can operate with lower pressure drop, but they may require more specialized electrical diagnostics and can be more sensitive to changes in dust properties.

9. Supplier Selection and Project Risk

|

Procurement checkpoint |

Required clarification |

|

Design basis |

Gas flow at normal and upset conditions; temperature; moisture; oxygen; inlet PM; particle size and resistivity |

|

Performance guarantee |

Outlet mg/Nm³ and mass efficiency; reference conditions; load range; allowable fields out of service |

|

Electrical design |

T-R or high-frequency supply rating; spark control; redundancy; grounding; harmonic and EMC requirements |

|

Mechanical reliability |

Electrode alignment, rapping distribution, hopper evacuation, insulator protection, access and maintainability |

|

Materials |

Acid dew point, chloride, erosion, corrosion allowance and WESP wash-water chemistry |

|

Integration |

Duct pressure balance, fans, boiler/process operation, FGD/scrubber interface and CEMS |

|

Retrofit execution |

3D survey, outage duration, temporary works, lifting plan, tie-ins and commissioning sequence |

|

Acceptance testing |

Test method, fuel/process envelope, averaging period, instrument uncertainty and remedy for shortfall |

|

Lifecycle support |

Local service team, critical spares, remote diagnostics, software support and response time |

Risk matrix

|

Risk |

Impact |

Probability |

Mitigation |

|

Dust resistivity outside design range |

High |

High |

Laboratory testing, gas conditioning, temperature optimization, WESP or hybrid option |

|

Gas maldistribution |

High |

Medium |

CFD/model testing, distribution screens, field velocity mapping |

|

Insufficient outage time |

High |

Medium to high |

Modular preassembly, detailed survey and phased retrofit |

|

Corrosion / acid condensation |

High |

Medium |

Material selection, temperature control, drainage and wash design |

|

Rapping re-entrainment |

Medium to high |

Medium |

Rapping optimization, electrode design, moving electrode or polishing stage |

|

Control obsolescence |

Medium |

High in older fleets |

Modern controller retrofit and spare strategy |

|

Baghouse substitution in tender |

Medium |

High |

Technology-neutral lifecycle comparison and hybrid proposal |

|

Local-content non-compliance |

Medium |

Region-specific |

Local fabrication, licensing and qualified partner network |

10. Outlook to 2034

The market’s likely growth path is moderate rather than explosive. The published forecast range indicates a global market potentially reaching roughly USD 16.7–16.9 billion by 2034, but the composition of that growth will matter more than the headline total. Conventional utility greenfield projects will become less dominant. Retrofit engineering, wet polishing, industrial process applications, high-frequency power supplies, digital monitoring and service will account for a larger share of value.

|

Scenario |

Indicative growth |

Conditions |

Commercial implication |

|

Base case |

5–6% annual growth |

Industrial expansion in Asia; ongoing retrofit cycle; steady regulation; continued baghouse competition |

Balanced portfolio across utility, steel, cement and service |

|

Upside case |

Above 6% |

Faster ultra-low-emission adoption; strong waste-to-energy/biomass build; high retrofit conversion rates |

Capacity in WESP, controls and regional service becomes constrained |

|

Downside case |

Below 4% |

Accelerated coal retirements; weak heavy-industry capex; aggressive baghouse substitution; project delays |

Commodity suppliers face severe pricing pressure |

|

Disruption case |

Revenue shifts, not necessarily lower market |

Hybrid collectors, electrified processes and digital performance contracts redefine scope |

Software, diagnostics and guarantees outweigh standalone hardware |

Strategic conclusions

- The market is investable, but not as a pure coal-equipment story. The strongest companies will monetize the installed base and serve multiple particulate-intensive industries.

- Retrofit capability is a primary competitive advantage. Owners need lower emissions within existing footprints and short outages; documented field performance has more value than nominal collection efficiency.

- Electrical and digital systems are becoming core products. High-frequency energization, field-level diagnostics and emissions-data integration can extend asset life and support recurring service.

- Wet ESPs and hybrid systems expand the market boundary. They address ultrafine particulate, acid mist and variable dust where conventional dry ESP performance is constrained.

- Regional execution determines commercial success. Local fabrication, service response and regulatory knowledge are essential in Asia, the Middle East, Latin America and Africa.

- Procurement must be based on process guarantees. A credible tender defines outlet concentration, gas conditions, dust properties, load range, testing method and lifecycle obligations.

Methodology and Sources

The report triangulates public market-research estimates with official industrial production statistics, government technical guidance and supplier engineering references. Market figures were not averaged mechanically because study scopes differ. Steel and cement production are used as demand-location proxies, not as direct revenue forecasts. Forecast years are marked with “E” and should be treated as estimates.

- U.S. Environmental Protection Agency. Monitoring by Control Technique – Electrostatic Precipitators, updated 21 May 2026.

- International Energy Agency. Global Energy Review 2025; Electricity 2026; Coal 2025.

- World Steel Association. December 2025 crude steel production and annual global totals, 23 January 2026.

- U.S. Geological Survey. Mineral Commodity Summaries 2026: Cement.

- Mordor Intelligence. Electrostatic Precipitator Market Size and Share, 2025–2030.

- Global Market Insights. Electrostatic Precipitator Market, 2025–2034.

- Strategic Market Research. Global Electrostatic Precipitator Market, 2024–2030.

- Fortune Business Insights. Electrostatic Precipitator Market Forecast, 2026–2034.

- ANDRITZ. Dry and wet ESP, hybrid filters, high-frequency rectifier and retrofit product information.

- Mitsubishi Heavy Industries. AQCS for Thermal Power Plants Capable of Responding to Wide Range of Coal Properties and Regulations, Technical Review Vol. 54 No. 3.

- Mitsubishi Heavy Industries Power Environmental Solutions. Electrostatic precipitator and AQCS product information.

Data cut-off: 15 July 2026. Public market estimates may be revised by their publishers. No unsupported vendor market-share ranking is used.

— End of Report —