Executive Summary

Flue-gas denitrification equipment is transitioning from a coal-power new-build market into a diversified emissions-control and lifecycle-service market. The commercially relevant perimeter includes selective catalytic reduction (SCR), selective non-catalytic reduction (SNCR), hybrid systems, catalyst modules, reagent preparation and injection, reactor internals, ammonia-slip control, continuous emissions monitoring integration, and performance retrofit services. Published estimates cannot be treated as interchangeable: narrow stationary SCR-system studies place the 2025 market near USD 3.6–4.3 billion, while broader flue-gas DeNOx equipment estimates reach approximately USD 6.3 billion. A still broader SCR universe that includes mobile applications can exceed USD 14 billion and is excluded from the core market range in this report.

The base-case outlook is moderate rather than explosive. Current stationary-market forecasts imply approximately 4.5–6.3% annual growth through 2031–2035. The main growth engine is no longer only additional coal capacity. It is the combination of catalyst replacement, low-load retrofit, stricter industrial-source standards, steel and cement capacity in Asia, waste-to-energy and biomass projects, refinery and chemical applications, marine SCR, and better digital control of reagent consumption and ammonia slip. Suppliers that rely only on reactor hardware will face margin pressure; suppliers that can guarantee outlet NOx across a wide load and temperature envelope, maintain catalyst activity, integrate monitoring, and provide local service are better positioned.

|

Finding |

Assessment |

|

Working 2025 market range |

Approximately USD 3.6–6.3 billion for stationary SCR / flue-gas DeNOx equipment, depending on whether catalyst, aftermarket, EPC and auxiliary systems are included. |

|

Forecast direction |

Most current stationary-market forecasts indicate 4.5–6.3% annual growth to 2031–2035; scope differences matter more than minor point estimates. |

|

Technology hierarchy |

SCR remains the preferred route for deep NOx removal; SNCR remains relevant where moderate reduction, low capital cost and simpler retrofit outweigh reagent efficiency. |

|

Demand centre |

Asia-Pacific is the largest demand base because of its concentration of coal generation, steel, cement and industrial boilers; Europe and North America are more aftermarket- and compliance-service intensive. |

|

Commercial shift |

Catalyst management, low-temperature operation, reagent optimization, CEMS integration and long-term service are becoming more defensible revenue pools than fabrication alone. |

|

Primary risks |

Coal retirement in advanced economies, local-price competition, catalyst poisoning, ammonia-supply and safety constraints, low-load temperature mismatch, and weak project-specific gas characterization. |

|

Report item |

Coverage |

|

Report date |

July 2026 |

|

Geographic scope |

Global, with regional assessment of Asia-Pacific, Europe, North America, Middle East, Latin America and Africa. |

|

Product scope |

SCR, SNCR and hybrid DeNOx systems; catalysts; reagent storage, vaporization and injection; reactor internals; controls; monitoring integration; retrofit and lifecycle services. |

|

Excluded scope |

Automotive and heavy-duty mobile SCR systems; generic air-pollution-control equipment without a defined NOx-removal function. |

|

Forecast horizon |

Market forecasts to 2031–2035, depending on the source; forecasts are marked as estimates. |

1. Scope and Market Definition

Flue-gas DeNOx equipment reduces nitrogen oxides generated by combustion and high-temperature industrial processes. NOx control is not a single-machine category: the performance of the reactor depends on flue-gas temperature, dust loading, sulfur chemistry, oxygen concentration, residence time, reagent distribution, catalyst activity, load profile and upstream/downstream equipment. For this reason, an investable market definition must include the engineered system and its recurring service requirements, not only the steel reactor casing.

Within industrial procurement databases, the closest broad category is waste gas treatment equipment, but project qualification should separate NOx removal from particulate, SOx, VOC and acid-gas control. Integrated air-quality-control systems can combine these functions, while the guarantees, catalyst chemistry and operating risks remain pollutant-specific.

|

Market layer |

Included content |

Revenue characteristics |

Boundary warning |

|

Core DeNOx system |

SCR/SNCR reactor, injection grid, reagent preparation, ductwork, controls and balance of plant |

Project revenue; engineering and fabrication intensive |

System vendors may report DeNOx as part of broader environmental divisions. |

|

Catalyst and internals |

Honeycomb, plate or corrugated catalyst modules; replacement layers; seals and support structures |

Recurring aftermarket; activity testing and replacement cycles |

Catalyst studies may include mobile SCR or marine applications. |

|

Monitoring and optimization |

NOx/O2/NH3 measurement, CEMS integration, ammonia-flow control, digital optimization |

Higher software/service content; retrofit-friendly |

Monitoring equipment is sometimes counted in instrumentation markets, not DeNOx. |

|

Lifecycle services |

Inspection, tuning, catalyst regeneration/replacement, flow modeling, outage work and guarantees |

Recurring and locally delivered |

Often omitted from equipment-only market estimates. |

|

Excluded mobile SCR |

On-road and off-road vehicle urea-SCR systems |

Large but structurally different market |

Including mobile systems materially overstates stationary industrial opportunity. |

Health and regulatory logic

NO2 is a respiratory irritant; short-term exposure can aggravate asthma and longer exposure may contribute to respiratory disease. The World Health Organization’s 2021 guideline is 10 µg/m³ annual mean and 25 µg/m³ for a 24-hour mean. These ambient objectives are translated into source-specific permitting, best-available-technique and stack-emission limits. As a result, demand for DeNOx systems is ultimately connected to air quality monitoring systems and verifiable continuous compliance rather than to equipment installation alone.

2. Global Market Size and Forecast

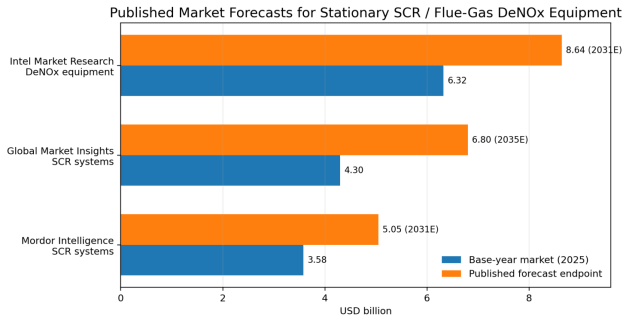

Current published estimates form three different market perimeters. Mordor Intelligence and Global Market Insights focus on SCR systems and place the 2025 market at approximately USD 3.58 billion and USD 4.3 billion, respectively. Intel Market Research uses the broader term “flue gas denitrification equipment” and estimates USD 6.32 billion in 2025. The gap is plausible because the broader estimate can capture SNCR, catalyst, auxiliary equipment, and a wider set of industrial projects. Grand View Research reports USD 14.4 billion for the overall SCR market in 2024, but its scope includes mobile applications and therefore should not be used as a stationary-equipment benchmark.

|

Source |

Scope |

Base year |

Base USD bn |

Forecast year |

Forecast USD bn |

CAGR |

Interpretation |

|

Mordor Intelligence |

SCR market; stationary emphasis |

2025 |

3.58 |

2031E |

5.05 |

5.89% |

Narrower system perimeter; highlights shift toward marine and industrial demand. |

|

Global Market Insights |

SCR systems |

2025 |

4.30 |

2035E |

6.80 |

4.5% |

Longer horizon; Asia-Pacific largest. |

|

Intel Market Research |

Flue-gas denitrification equipment |

2025 |

6.32 |

2031E |

8.64 |

6.3% |

Broader equipment perimeter, likely including more auxiliaries and industrial applications. |

|

Grand View Research |

SCR market including mobile and stationary |

2024 |

14.40 |

2030E |

19.70 |

5.5% |

Not included in the core stationary range; useful only as a scope comparison. |

Figure 1. Published stationary SCR / flue-gas DeNOx market forecasts

Source: Mordor Intelligence; Global Market Insights; Intel Market Research. Forecast scope differs by source; values are not additive.

The most defensible 2025 working range for stationary DeNOx equipment is therefore USD 3.6–6.3 billion. The range should not be compressed into a single pseudo-precise value. A project supplier’s addressable market will depend on whether it sells complete systems, catalysts, reagent skids, controls, retrofits or only selected components. The recurring catalyst and service pools can also be strategically more valuable than their share of initial project capital suggests.

Catalyst market as a recurring revenue pool

Catalyst-specific estimates are also inconsistent because some include mobile and marine applications. Two narrower published studies place the 2026 SCR-catalyst market at roughly USD 1.9–2.15 billion and forecast approximately USD 2.87–3.61 billion by 2035. These figures indicate a material aftermarket, but they should not be added directly to the system-market estimates because catalyst revenue may already be embedded in those totals.

3. Demand Drivers and Structural Constraints

3.1 Coal power: a declining share, a persistent installed base

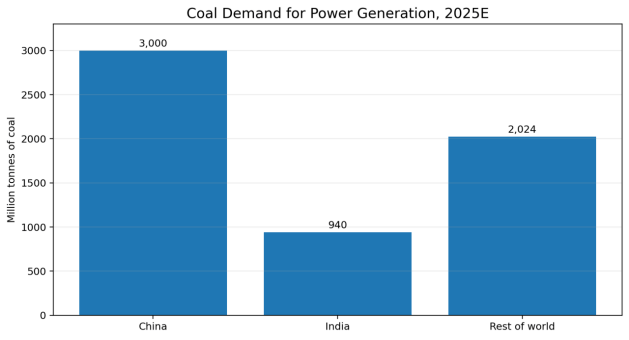

The coal-power market is structurally mixed. The International Energy Agency estimates power-sector coal demand at 5,964 million tonnes in 2025, with China near 3,000 million tonnes and India at approximately 940 million tonnes. By 2030, the IEA expects power-sector coal demand to decline toward 5,710 million tonnes and coal’s share of global electricity generation to fall from 35% in 2024 to 27%. For DeNOx suppliers, this means the opportunity is increasingly concentrated in retrofit, catalyst replacement, flexible-operation upgrades and service for existing coal-fired power generation assets rather than uniform global growth in new utility projects.

Figure 2. Coal demand for power generation, 2025E

Source: International Energy Agency, Coal 2025. China value is reported as “near 3,000 Mt”; rest of world is calculated from the IEA global total.

Cycling operation is becoming a technical demand driver. Conventional vanadium-based SCR catalysts generally perform best in a defined temperature window. When coal units operate at low load to balance renewable generation, reactor temperature can fall below the effective range, increasing ammonia slip and reducing conversion. Solutions include economizer bypass, flue-gas reheating, catalyst formulation changes, reactor relocation, additional catalyst volume and improved reagent distribution. These modifications can be more complex than the original installation because they interact with boiler efficiency, SO3 formation, air preheater fouling and outage schedules.

3.2 Steel and cement: the stabilizing industrial demand base

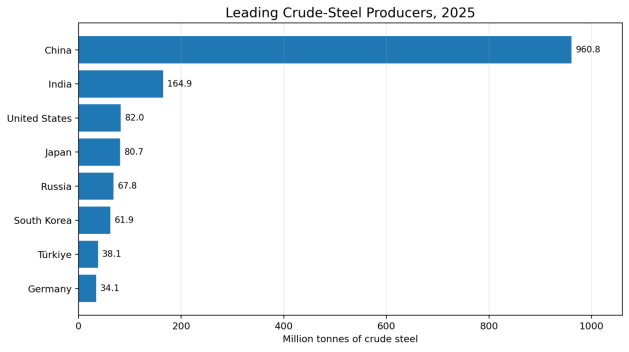

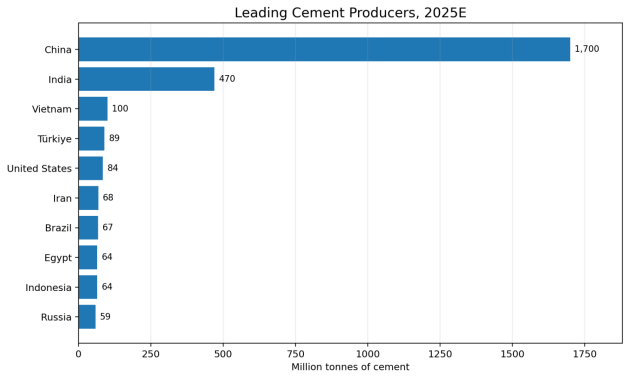

Steel and cement create a geographically concentrated and technically demanding market. Worldsteel reports 1,849.4 million tonnes of global crude-steel production in 2025, led by China at 960.8 million tonnes and India at 164.9 million tonnes. Sinter plants, coke ovens, reheating furnaces and selected ironmaking processes require application-specific NOx control. Cement production was approximately 3.8 billion tonnes in 2025 according to the U.S. Geological Survey, with China and India accounting for more than half. Cement kilns are a major SNCR application and an expanding SCR or hybrid opportunity where lower limits, ammonia-slip constraints or difficult fuels exceed SNCR capability.

Figure 3. Leading crude-steel producers, 2025

Source: World Steel Association, December 2025 crude-steel production release.

Figure 4. Leading cement producers, 2025E

Source: U.S. Geological Survey, Mineral Commodity Summaries 2026. Values are estimated production.

3.3 Industrial-source regulation and continuous compliance

The European Union’s best-available-technique associated emission levels for coal- and lignite-fired large combustion plants generally become tighter as unit size increases, with annual-average ranges for new large units commonly below 100 mg/Nm³. Similar compliance logic is spreading to industrial boilers, waste-to-energy plants, refineries and chemical facilities. Because the guarantee is measured continuously, project value increasingly includes flue gas emission monitors, instrument validation, data acquisition and control-loop tuning. A reactor that meets a short acceptance test but cannot maintain NOx and ammonia-slip limits through load changes is no longer commercially sufficient.

|

Demand driver |

Market effect |

Most exposed equipment/services |

Constraint |

|

Tighter outlet-NOx limits |

Raises required reduction and increases SCR penetration |

SCR reactor, catalyst, AIG tuning, CEMS integration |

Higher capital cost and stronger guarantee risk |

|

Low-load / cycling operation |

Creates temperature mismatch and transient ammonia slip |

Low-temperature catalyst, bypass/reheat, digital controls |

Efficiency penalty and retrofit complexity |

|

Industrial capacity in Asia |

Supports new and retrofit demand in steel, cement and process industries |

SNCR, SCR, hybrid, local EPC and service |

Local-content and price competition |

|

Catalyst aging and poisoning |

Creates recurring replacement and testing demand |

Catalyst modules, lab testing, regeneration, inspection |

Waste handling and performance uncertainty |

|

Ammonia safety and logistics |

Influences reagent choice and site permitting |

Aqueous ammonia, anhydrous ammonia or urea systems |

Storage, transport, corrosion and emergency response |

|

Carbon transition |

Reduces some long-term coal new-build demand |

Diversification into WtE, marine, refining and industrial sectors |

Stranded-project and utilization risk |

4. Technology Landscape

4.1 SCR, SNCR and hybrid systems

Selective catalytic reduction injects ammonia or urea-derived ammonia into the flue gas and passes the mixture over a catalyst. The U.S. EPA describes practical commercial SCR removal efficiency of approximately 70–90%, while well-designed projects can target above 90% under favorable conditions. Conventional metal-oxide catalysts have a broad effective range of roughly 250–427°C, with common high-dust utility operation near 320–400°C. Typical design ammonia slip is often 2–5 ppm. These performance values are not universal guarantees: sulfur content, ash composition, arsenic, alkali metals, dust erosion, temperature and flow distribution can materially change results.

SNCR injects ammonia or urea into a high-temperature zone without a catalyst. It requires lower initial capital and is easier to retrofit, but typically achieves lower removal and can consume more reagent. EPA technical material commonly cites approximately 30–50% reduction as a practical range, while specific datasets show broader results depending on reagent and combustion conditions. Hybrid SNCR-SCR uses upstream SNCR for bulk reduction and a smaller downstream catalyst for polishing, potentially reducing catalyst volume while widening the operating envelope.

|

Attribute |

SCR |

SNCR |

Hybrid SNCR-SCR |

|

Typical NOx-removal range |

70–90%; higher targets possible with project-specific design |

Commonly 30–50%; broader reported ranges depend on application |

Intermediate to high; combines bulk reduction with catalytic polishing |

|

Capital intensity |

High |

Low to moderate |

Moderate to high |

|

Reagent efficiency |

Generally better |

Generally lower; over-injection increases slip |

Potentially optimized across two stages |

|

Temperature sensitivity |

Catalyst-specific window; low-load operation can be difficult |

Narrow high-temperature injection window |

Can widen practical operating range |

|

Pressure drop |

Reactor/catalyst pressure drop and fan penalty |

Minimal additional pressure drop |

Lower catalyst volume than full SCR may reduce pressure drop |

|

Best fit |

Deep compliance, large units, stringent ammonia-slip control |

Moderate reduction, smaller units, limited retrofit space/capital |

Variable operation or requirements beyond stand-alone SNCR |

|

Primary risk |

Catalyst poisoning, plugging, SO2-to-SO3 conversion, low-load temperature |

Ammonia slip, N2O formation with urea, incomplete mixing |

Control complexity and guarantee allocation between stages |

4.2 SCR reactor configurations

|

Configuration |

Location / condition |

Advantage |

Main trade-off |

|

High-dust SCR |

Upstream of air preheater and particulate control |

Adequate temperature without reheating; common for utility boilers |

High ash exposure, erosion, plugging and poisoning risk |

|

Low-dust SCR |

After particulate removal, before or around desulfurization depending process |

Lower dust loading extends catalyst cleanliness |

Temperature may be lower; duct and heat-integration complexity |

|

Tail-end SCR |

Downstream of particulate and sulfur controls |

Clean gas; strong catalyst protection; suited to difficult industrial streams |

Often requires reheating; energy penalty and corrosion management |

|

In-duct / compact SCR |

Smaller boilers, gas turbines, process units or constrained retrofits |

Reduced footprint and faster installation |

Shorter residence time and tighter flow-distribution requirements |

|

Marine SCR |

Engine exhaust with urea dosing and compact catalyst reactor |

Compliance with IMO NOx requirements in applicable operating areas |

Space, sulfur/fuel compatibility, load transients and urea logistics |

4.3 Catalyst technology and lifecycle economics

Stationary SCR catalysts are commonly based on titanium dioxide carriers with vanadium, tungsten or molybdenum oxides. Honeycomb modules provide high surface area and are widely used in cleaner or moderate-dust applications; plate and corrugated designs can be selected for higher dust tolerance. Catalyst selection is a chemical and mechanical design exercise. Required activity must be balanced against pressure drop, SO2-to-SO3 conversion, arsenic resistance, abrasion, plugging, thermal durability and end-of-life handling.

The EPA notes that catalyst can represent at least 20% of SCR capital cost in some applications. Actual coal-service layer life can be approximately five to seven years, while cleaner gas or oil applications can last longer. This creates a recurring market for activity testing, layer rotation, replacement, regeneration and disposal. It also creates a bankability issue: a low-cost catalyst with weak poisoning resistance can raise lifecycle cost through early replacement, lost availability or reagent overconsumption.

|

Catalyst decision |

Why it matters |

Procurement evidence required |

|

Activity at design temperature |

Determines catalyst volume and outlet NOx capability |

Activity curve across expected temperature and load range |

|

SO2-to-SO3 conversion |

Excess conversion can increase acid mist, air-preheater fouling and visible plume |

Guaranteed conversion rate at stated sulfur and temperature |

|

Poison resistance |

Arsenic, alkali, phosphorous and other species deactivate active sites |

Fuel/ash analysis, reference installations and deactivation model |

|

Erosion and plugging |

High-dust units can lose area or flow distribution |

Pitch, wall thickness, abrasion data and cleaning strategy |

|

Pressure drop |

Drives ID-fan power and operating cost |

Clean and end-of-run pressure-drop guarantee |

|

Replacement strategy |

Outage duration and spare-layer planning affect availability |

Layer management plan, module interchangeability and local service |

|

End-of-life route |

Spent catalyst may contain regulated constituents |

Regeneration, recycling or disposal pathway and responsibility |

Technology selection should be treated as an integrated waste gas treatment technology decision. Downstream air preheaters, particulate collectors and desulfurization systems can be affected by ammonia bisulfate, SO3 and temperature changes. A low bid based only on reactor steel weight can therefore transfer cost into boiler efficiency, fouling, reagent use and maintenance.

5. End-Use Market Assessment

|

End-use sector |

Typical NOx source |

Preferred route |

Commercial opportunity |

Principal risk |

|

Coal-fired power |

Boiler combustion |

High-dust SCR; low-load retrofit; catalyst service |

Large installed base, catalyst replacement, AIG tuning, digital optimization |

Fleet retirement, cycling operation and sulfur/ash poisoning |

|

Gas turbines / combined cycle |

Turbine combustion, often with CO control |

Compact SCR, often in HRSG |

New gas capacity, hydrogen-blend readiness, low outlet limits |

Low-temperature transients, ammonia distribution and space |

|

Cement and lime |

Kiln and calciner combustion |

SNCR, staged combustion, SCR or hybrid |

Large production base, alternative fuels, tighter industrial standards |

Dust, alkali, variable fuel and high-temperature-window control |

|

Steel and iron |

Sintering, coke ovens, reheating and process furnaces |

Tail-end SCR, low-temperature catalysts, SNCR for selected furnaces |

Major Asian production base and complex multi-pollutant retrofits |

Variable gas chemistry, sulfur and dust, fragmented sources |

|

Waste-to-energy / biomass |

Boilers and furnaces |

SNCR plus tail-end SCR or catalytic bag filter |

Strict urban permits and stable service demand |

Catalyst poisoning, corrosion and public permitting |

|

Refining / petrochemicals |

FCC regenerators, heaters, boilers, sulfuric-acid and process units |

SCR, SNCR or process-specific catalytic systems |

High-value compliance projects and service contracts |

Shutdown scheduling, hazardous areas and process integration |

|

Pulp and paper |

Recovery boilers, lime kilns, biomass boilers |

SNCR or SCR depending limit and gas condition |

Mature retrofit and biomass demand |

Alkali, dust and variable operating conditions |

|

Marine engines |

Diesel engine exhaust |

Compact urea-SCR |

IMO-compliance market and retrofit/service opportunity |

Space, operating-area rules, urea logistics and sulfur compatibility |

Power remains the largest installed-base market, but the industrial mix determines resilience. Cement and steel are attractive because production is concentrated in jurisdictions with tightening pollution controls; however, their dust and gas chemistry often require more complex engineering than utility boilers. Waste-to-energy and refineries support higher-value tail-end or low-dust systems, while gas turbines support compact SCR packages integrated into heat-recovery steam generators. Marine SCR is adjacent rather than identical, but it offers diversification for catalyst and compact-system suppliers.

5.1 Economics: capex, reagent and energy

Current public cost manuals are useful for identifying cost drivers but not for quoting 2026 project prices, because many underlying examples are in historical dollars and site conditions vary widely. The economic hierarchy is still clear. SCR requires a reactor, catalyst, structural steel, ductwork, ammonia or urea handling, injection, controls and often fan or heat-integration modifications. SNCR avoids the catalyst reactor but can require more reagent and may carry a higher ammonia-slip risk. The EPA estimates that SCR-related pressure drop can require incremental fan power on the order of 0.3% of plant output in representative utility applications; actual values depend on ducting, catalyst layers and existing fan margin.

|

Cost element |

Primary sizing variables |

Commercial implication |

|

Engineering and process design |

NOx inlet profile, gas flow, temperature/load envelope, fuel chemistry, target limit |

Strongly affects guarantee risk; under-characterization is a common source of change orders |

|

Reactor, ductwork and structure |

Gas volume, pressure, temperature, seismic/wind loads, available space |

High fabrication and site-installation content |

|

Catalyst |

Required activity, pitch, layer count, poisoning resistance and life |

Material recurring cost; can be ≥20% of SCR capital in some applications |

|

Reagent system |

Ammonia versus urea, storage volume, vaporization/hydrolysis, safety code |

Site permitting, logistics and operating cost |

|

Injection and mixing |

Duct geometry, residence time, load range and flow uniformity |

Controls outlet NOx and ammonia slip; grid tuning is critical |

|

Fan / heat integration |

Pressure drop, available ID-fan margin, temperature shortfall |

Creates energy penalty and may require major boiler-side retrofit |

|

Instrumentation and controls |

NOx/O2/NH3 measurement points, response time, redundancy |

Supports reagent optimization and continuous guarantee |

|

Outage and construction |

Tie-ins, heavy lifts, access, scaffolding, commissioning window |

Can dominate retrofit schedule and lost-production cost |

6. Regional Market Outlook

|

Region |

Market position |

Demand drivers |

Best opportunities |

Main risk |

|

Asia-Pacific |

Largest global demand base |

Concentration of coal generation, steel, cement and industrial capacity; ongoing retrofit and replacement |

India industrial growth; China catalyst/service and low-load upgrades; Southeast Asian power/cement projects |

Aggressive local pricing, local-content requirements and uneven enforcement |

|

Europe |

Mature, regulation- and retrofit-intensive |

Industrial Emissions Directive, BAT-AELs, WtE, biomass, marine and replacement demand |

Tail-end/low-temperature SCR, catalyst service, digital optimization, multi-pollutant integration |

Coal phase-out, long permitting and high installation cost |

|

North America |

Mature installed base with selective new projects |

Utility and industrial compliance, gas turbines, refineries, biomass and WtE |

Aftermarket, AIG tuning, catalyst management, gas-turbine SCR and controls |

Coal retirement, project litigation and long outage planning |

|

Middle East |

Project-led industrial growth |

Refineries, petrochemicals, gas power, desalination-linked power and metals |

Integrated AQCS, high-value process applications and service localization |

Extreme climate, reagent logistics and project-payment risk |

|

Latin America |

Selective industrial and utility demand |

Cement, mining, refining, pulp and paper, urban air-quality regulation |

Modular systems, industrial retrofits and lifecycle service |

Currency, financing and inconsistent enforcement |

|

Africa |

Early-stage and project-specific |

Cement, mining/metals, refineries and selected power projects |

Compact/modular systems and EPC partnerships |

Financing, local service capability and reagent supply |

Asia-Pacific’s share is supported by physical production assets, not only by forecast narratives. China and India dominate power-sector coal use, while the region also contains most of the world’s steel and cement output. The addressable opportunity, however, differs by country. China is increasingly a replacement, optimization and industrial-retrofit market with intense local competition. India combines new industrial capacity with tighter pollution control but project timelines and enforcement can vary. Southeast Asia remains project-led. In Europe and North America, lower greenfield utility volumes are offset by technically demanding retrofit, catalyst and service work.

7. Competitive Landscape and Business Models

The market is fragmented across system integrators, boiler and power-equipment groups, catalyst specialists, environmental EPC firms, reagent suppliers, controls companies and regional fabricators. No single supplier category controls all value pools. Global system vendors compete on process guarantees and references; catalyst specialists compete on activity, poison resistance and lifecycle management; regional EPC companies compete on price, local construction and permitting; controls and monitoring providers increasingly influence operating cost and compliance reliability.

|

Supplier group |

Representative companies / capabilities |

Competitive position |

|

Integrated environmental-system suppliers |

ANDRITZ; Mitsubishi Power / MHI environmental businesses; Babcock & Wilcox; Dürr; Valmet; selected GE Vernova legacy AQCS capabilities |

Broad process integration, large references, retrofit and lifecycle service; generally higher overhead and project selectivity |

|

Catalyst specialists |

Topsoe; Johnson Matthey; Cormetech; Yara and regional catalyst producers |

Materials know-how, activity testing, replacement and recurring revenue; exposed to price competition and mobile/stationary scope differences |

|

Power and boiler OEM-linked suppliers |

Utility boiler OEMs and regional power-equipment groups |

Strong installed-base access and boiler integration; may bundle DeNOx with wider plant upgrades |

|

Regional environmental EPC firms |

China, India, Europe and other regional specialists |

Local cost, permitting and construction capability; quality and long-term guarantee capability vary |

|

Reagent and handling suppliers |

Ammonia/urea producers, storage and vaporization/hydrolysis specialists |

Essential to safety, logistics and OPEX; often partner rather than lead system contract |

|

Monitoring and optimization vendors |

CEMS, NOx/O2/NH3 analyzers, advanced process controls and digital-service providers |

Retrofit-friendly, recurring service and measurable reagent savings; depend on reliable sensing and integration |

ANDRITZ publicly positions SCR and SNCR for power stations, waste-to-energy and industrial plants, including pulp and paper, mining and metals, oil and refining, and marine applications. Topsoe lists stationary and marine SCR catalyst products. These examples illustrate the competitive direction: suppliers are broadening from a single power-sector reactor into application-specific catalyst, engineering and service portfolios. Market-share comparisons are difficult because many companies report DeNOx within larger environmental or power divisions.

|

Revenue pool |

Margin defensibility |

Why |

|

Process design and performance guarantee |

High |

Requires gas characterization, chemistry, flow modeling and responsibility for outlet NOx/slip across load range. |

|

Catalyst formulation and lifecycle management |

Medium to high |

Recurring demand and proprietary know-how; commodity grades face price pressure. |

|

Controls, sensing and optimization |

Medium to high |

Can reduce reagent and improve compliance; scalable retrofit opportunity. |

|

Reagent preparation and injection package |

Medium |

Safety and process integration matter, but hardware can be standardized. |

|

Reactor steel and duct fabrication |

Low to medium |

High material/logistics content and strong local competition. |

|

Construction and outage execution |

Medium, locally defensible |

Site knowledge and schedule control are valuable; project risk can erode margin. |

|

Long-term service and spare modules |

High where installed base is proprietary |

Customer switching costs and outage timing support recurring revenue. |

8. Procurement and Supplier Selection

A DeNOx procurement specification should be based on an agreed design envelope rather than a single nominal operating point. Inlet NOx concentration, gas flow, temperature, moisture, oxygen, SO2/SO3, dust, trace poisons and load profile must be defined at normal, minimum, maximum and upset conditions. Guarantees should state reference oxygen and dry/wet basis. Without this discipline, suppliers can quote different technical scopes while appearing commercially comparable.

|

Procurement checkpoint |

Required clarification |

|

Design basis |

Gas flow, temperature, moisture, oxygen, pressure, inlet NOx, SO2/SO3, dust and poison species at normal/minimum/maximum load. |

|

Performance guarantee |

Outlet NOx and/or removal efficiency; reference conditions; load range; startup and transient exclusions. |

|

Ammonia slip |

Guaranteed ppm at stated measurement point, temperature, catalyst age and load; measurement method and averaging time. |

|

Reagent consumption |

Ammonia or urea consumption at defined inlet NOx and efficiency; reagent purity and conversion assumptions. |

|

Catalyst performance |

Initial activity, end-of-run activity, pressure drop, SO2-to-SO3 conversion, poison resistance and warranted operating hours. |

|

Temperature envelope |

Minimum/maximum continuous and short-term temperatures; low-load mitigation and reheating/bypass responsibility. |

|

Flow distribution |

CFD/model criteria, velocity and NH3/NOx uniformity, grid tuning and acceptance-test methodology. |

|

Availability and outage |

System availability, planned maintenance, catalyst replacement duration, spare strategy and liquidated damages. |

|

Monitoring and controls |

CEMS interface, NH3 slip measurement, analyzer redundancy, control philosophy, cybersecurity and historian access. |

|

Safety and compliance |

Reagent storage code, hazardous-area classification, leak detection, emergency response and operator training. |

|

Waste and end of life |

Spent catalyst, purge streams and contaminated wash-water handling; regeneration/recycling/disposal responsibility. |

|

Local service |

Response time, regional spares, commissioning team, language, remote support and performance-reference access. |

A modern tender should also define the boundary between the DeNOx package and power plant equipment: boiler controls, economizer bypass, ID fans, air preheaters, particulate collectors, desulfurization, stack and electrical systems. Interface ambiguity is a major source of retrofit delay and guarantee disputes.

9. Risk Matrix

|

Risk |

Impact |

Probability |

Mitigation |

|

Catalyst poisoning or deactivation |

High |

Medium to high |

Fuel/ash characterization, poison-resistant formulation, activity testing, spare-layer strategy and performance trend monitoring |

|

Low-load temperature below catalyst window |

High |

High for cycling units |

Load-profile analysis, bypass/reheat, low-temperature catalyst, reactor relocation and control optimization |

|

Ammonia slip / bisulfate formation |

High |

Medium |

AIG tuning, online measurement, mixing improvement, catalyst management and air-preheater monitoring |

|

Excess SO2-to-SO3 conversion |

High |

Medium |

Low-conversion catalyst, sulfur basis, temperature control and explicit guarantee |

|

Flow or reagent maldistribution |

High |

Medium |

CFD, physical modeling where justified, grid design, field mapping and commissioning tuning |

|

Reagent-supply interruption or safety incident |

High |

Medium |

Dual sourcing, inventory policy, urea alternative, storage code compliance and emergency procedures |

|

Pressure-drop / fan-margin shortfall |

Medium to high |

Medium |

Full-system hydraulic model, dirty-end pressure-drop guarantee and fan study |

|

CEMS or analyzer bias |

High |

Medium |

Redundancy, calibration, data validation, independent performance testing and maintenance contract |

|

Local construction / outage delay |

High |

Medium |

Detailed constructability review, modularization, lift plan, interface register and schedule contingencies |

|

Policy or asset-utilization change |

Medium to high |

Medium |

Diversify across industrial, WtE, gas-turbine, marine and service markets |

10. Market Outlook to 2035

The most likely market path is a mid-single-digit expansion, with revenue quality improving faster than unit shipments. System new-build demand will remain uneven, but installed-base service, catalyst replacement, industrial-source compliance and low-load retrofit should support the market. The upside case requires faster tightening of industrial NOx standards, sustained steel/cement investment in Asia, stronger waste-to-energy and gas-turbine construction, and rapid adoption of low-temperature catalysts and digital optimization. The downside case combines accelerated coal retirement, delayed industrial enforcement, price-led local competition and weak project financing.

|

Scenario |

Indicative annual growth |

Conditions |

Commercial implication |

|

Base case |

Approximately 4.5–6% |

Installed-base replacement; industrial regulation; moderate Asian capacity growth; steady catalyst/service demand |

Balanced portfolio across SCR/SNCR, catalysts, industrial sectors and regional service |

|

Upside case |

Above 6% |

Faster low-NOx standards; strong India/SE Asia industrial growth; WtE/gas-turbine/marine expansion; low-temperature retrofit adoption |

Capacity constraints emerge in catalysts, specialist engineering and commissioning |

|

Downside case |

Below 4% |

Rapid coal retirement; enforcement delays; project cancellations; severe price competition and weak industrial capex |

Hardware margins compress; aftermarket and digital optimization become essential |

Strategic conclusions

|

Strategic question |

Judgment |

|

Is the market still dependent on coal? |

Coal remains the largest installed base, but growth resilience increasingly comes from industrial sources, gas turbines, WtE, marine and services. |

|

Will SCR displace SNCR? |

No. SCR will dominate deep-removal applications, while SNCR remains economical for moderate reduction and constrained retrofits; hybrid configurations will expand selectively. |

|

Where is pricing power strongest? |

Process guarantees, catalyst lifecycle management, low-temperature engineering, CEMS integration and local service—not commodity reactor steel. |

|

What is the key technology bottleneck? |

Maintaining high conversion with low ammonia slip across variable load, temperature and gas chemistry. |

|

What should suppliers invest in? |

Application laboratories, catalyst/activity diagnostics, CFD and mixing design, digital optimization, regional service and multi-pollutant integration. |

|

What should buyers avoid? |

Comparing bids without a common design basis, catalyst-end-of-life guarantees, reagent assumptions, fan/temperature interfaces and acceptance-test definitions. |

Conclusion

Flue-gas DeNOx equipment is a mature technology category with a changing commercial center of gravity. The market is not defined by one global emission limit or one combustion sector. It is defined by the growing difficulty of maintaining compliance over the full operating envelope of aging and increasingly flexible assets, while industrial sources face more measurable and enforceable air-quality requirements. This shifts value from one-time reactor fabrication toward catalyst science, integration, monitoring, optimization and service.

A credible supplier must demonstrate more than nominal NOx-removal efficiency. It must quantify ammonia slip, pressure drop, reagent consumption, catalyst life, SO2-to-SO3 conversion, load range, availability and interface responsibilities. A credible buyer must provide a realistic gas and operating profile. Where these disciplines are present, the market offers durable mid-single-digit growth and recurring aftermarket value. Where they are absent, low initial price can mask higher lifecycle cost and compliance risk.

Methodology and Source Notes

Market estimates were triangulated rather than averaged. Stationary SCR-system studies and broader flue-gas denitrification-equipment studies were treated as different perimeters. Mobile SCR estimates were shown only to explain scope inflation and were excluded from the core range. Production and fuel-demand data were taken from international or official statistical bodies. Technical performance ranges were taken from U.S. EPA cost and technical manuals and should be treated as application ranges, not universal guarantees. Supplier examples are illustrative and do not represent a market-share ranking.

- International Energy Agency, Coal 2025 – Demand

- World Steel Association, December 2025 crude-steel production

- U.S. Geological Survey, Mineral Commodity Summaries 2026 – Cement

- U.S. EPA Air Pollution Control Cost Manual – Selective Catalytic Reduction

- U.S. EPA Air Pollution Control Cost Manual – Selective Non-Catalytic Reduction

- European Commission / EUR-Lex, BAT conclusions for large combustion plants

- World Health Organization, Nitrogen dioxide and air-quality health impacts

- Global Market Insights, Selective Catalytic Reduction System Market

- Mordor Intelligence, Selective Catalytic Reduction Market

- Intel Market Research, Flue Gas Denitrification Equipment Market

- Grand View Research, Selective Catalytic Reduction Market

- ANDRITZ, DeNOx Selective Catalytic Reduction

- ANDRITZ, Selective Non-Catalytic Reduction

- Topsoe, catalyst portfolio

- IMO, Prevention of Air Pollution from Ships under MARPOL Annex VI