en.Wedoany.com Reported - SK Hynix and CXMT (ChangXin Memory Technologies) have each disclosed their development data, revealing distinctly different growth paths and stage-specific characteristics in the same memory upcycle, spanning revenue, profitability, R&D investment, product structure, and capacity planning.

Although CXMT's revenue base is smaller, its growth momentum is stronger. From 2023 to 2025, the company's operating revenue surged from 9.087 billion yuan to 61.799 billion yuan, achieving a compound annual growth rate of 160.78%. In the first quarter of 2026 alone, quarterly revenue reached 50.8 billion yuan, a year-on-year increase of 719%, nearly matching the total for the full year 2025; the company expects first-half revenue to reach 110 billion to 120 billion yuan, a year-on-year increase of over 600%.

The underlying logic behind the revenue explosion of both companies shares commonalities and differences. The commonality lies in the strong upward cycle of global DRAM prices. Since the end of 2024, the spot price of DDR5 has accumulated an increase of approximately 4 times, while prices for high-end HBM products have continued to rise, leading to volume and price growth across the entire industry. The difference is reflected in product structure: SK Hynix's growth is driven by high-value-added products like HBM, with AI-related business revenue accounting for nearly half of its total; CXMT's growth stems more from the release of traditional DRAM capacity and increased penetration of domestic substitution.

Profitability is the most closely watched indicator in both companies' prospectuses, with both achieving record-high profitability. SK Hynix posted a net profit of 28.19 billion U.S. dollars in 2025, with a net profit margin of 44.2%; its operating profit margin climbed to 72% in the first quarter of 2026, higher than TSMC's 58.1% and Nvidia's approximately 65.6% for the same period, setting a new profit margin record for large enterprises in the global semiconductor industry. This high profit margin is primarily attributed to the strong pricing power of the HBM business—SK Hynix holds a 56% to 58% global market share in HBM, with long-term contracts locked in until 2028, and customized HBM quotations range from 120 to 200 U.S. dollars per GB, with gross margins far exceeding those of traditional DRAM.

CXMT's profitability turnaround is equally remarkable. In 2024, the company still reported a net loss attributable to parent company of 7.145 billion yuan; it turned profitable in 2025, with a net profit attributable to parent company of 1.875 billion yuan; in the first quarter of 2026, this figure surged to 24.762 billion yuan. The company expects a net profit attributable to parent company of 50 billion to 57 billion yuan in the first half of the year, with average daily earnings exceeding 300 million yuan, enough to cover cumulative losses over the past nine years and still leave a surplus. However, the composition of high profit margins differs between the two: SK Hynix's high gross margin is built on product structure upgrades, with high-end products like HBM contributing the majority of profit growth and possessing strong technical barriers; CXMT's current high profit margin benefits more from the general price increase across the industry. Professional media outlet SemiAnalysis estimates that its unit bit cost is still over 30% higher than that of the three international giants, with products primarily consisting of mainstream DDR5 and LPDDR5, while HBM is still in the R&D and trial production stage. Some analysts point out that once industry prices decline, CXMT's profit margin could be more elastic.

Looking at gross margin trends, CXMT's improvement has been steeper: its comprehensive gross margin was still negative in 2023, turned positive to around 5% in 2024, and rapidly increased to 41% in 2025; SK Hynix's comprehensive gross margin was approximately 49% in 2025, and further increased in the first quarter of 2026 due to a higher proportion of HBM, making its overall earnings quality more stable.

In the technology-intensive memory track, the intensity and direction of R&D investment determine future rankings. CXMT's R&D expenditure in 2025 was 9.593 billion yuan, with an R&D expense ratio of 15.52%, significantly higher than SK Hynix's 6.66%, Samsung's 11.31%, and Micron's 10.16% for the same period. From 2023 to 2025, the company's cumulative R&D investment reached 20.6 billion yuan, accounting for 21.67% of its revenue over the period, with funds primarily directed towards improving yield and mass production of mainstream processes like LPDDR5 and DDR5, as well as exploratory investments in high-end packaging technologies such as HBM. Against the backdrop of international export controls, high R&D spending is both an offensive move and a necessity for building a secure supply chain fortress. SK Hynix's R&D investment was approximately 4 trillion Korean won in 2024, further increasing in 2025, with an absolute amount about three to four times that of CXMT, focusing on EUV lithography processes, HBM3E and next-generation HBM4, as well as NAND flash memory with over 300 layers, giving it a clear technological generation lead.

The two companies have also taken distinctly different paths in their R&D strategies. SK Hynix adopts a "generational iteration" strategy, closely following Moore's Law to advance process miniaturization while leading industry standards in new forms like HBM. CXMT, on the other hand, employs a "generation-skipping" R&D strategy, achieving mass production across four generations of process platforms within a decade. Without EUV equipment, it has caught up technologically through innovations like multi-patterning, and has now mass-produced DDR5 and LPDDR5X products, with speed indicators entering the global first tier.

The difference in product structure is the most fundamental divergence between the two companies. SK Hynix has formed a complete product matrix, with three major DRAM product lines—HBM, server DDR5, and mobile LPDDR5X—advancing in parallel. It holds the top global market share in HBM and is a core supplier to AI chip manufacturers like Nvidia and AMD; its NAND flash memory business, through the acquisition of Intel's flash memory business, has risen to second place globally, with enterprise SSD business growing rapidly. Overall, AI-related business has become SK Hynix's primary growth engine.

CXMT's products are concentrated in the mainstream DRAM market, with the DDR series accounting for about 28% of revenue, the LPDDR series for 70%, and server-grade DRAM's share gradually increasing to 25% annually. Its customers are primarily domestic Chinese cloud vendors and consumer electronics brands, with Alibaba Cloud, Tencent, ByteDance, Lenovo, and Xiaomi as core clients, and its adoption rate in the Android phone market has exceeded 30%. In terms of HBM products, it has delivered HBM3 samples and plans small-scale mass production by the end of 2026, but it is unlikely to contribute significant revenue in the short term.

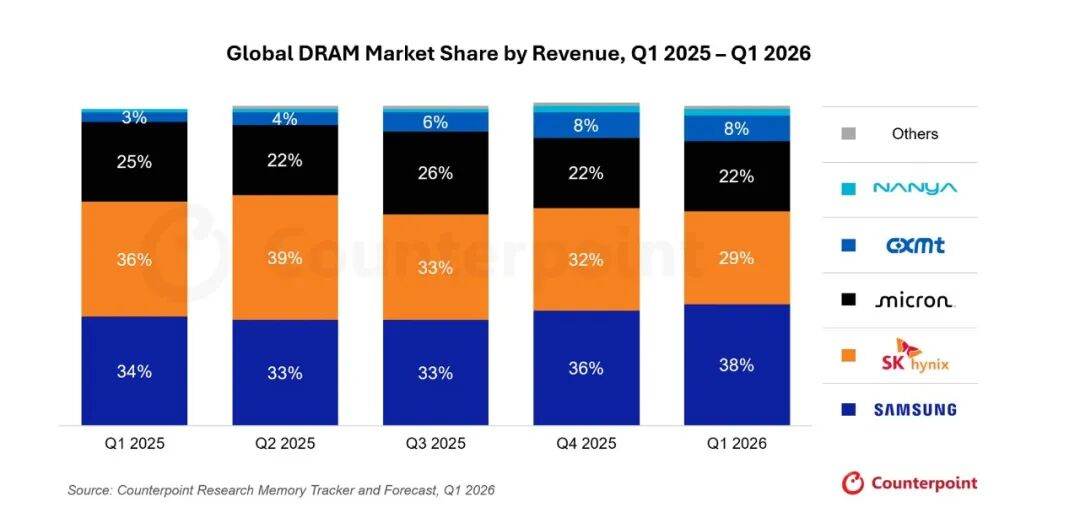

In terms of market share, SK Hynix leads the global HBM track with a 56.4% share. CXMT ranks fourth globally with a 7.7% market share, having increased its share by nearly 5 percentage points in one year, the fastest growth rate among the top four manufacturers, breaking the previous pattern where Samsung, SK Hynix, and Micron monopolized nearly 90% of the market.

The funds raised from the listings of both companies are primarily directed towards capacity expansion and technological R&D. SK Hynix's current U.S. stock listing raised approximately 26.5 billion U.S. dollars, setting a historical record for foreign companies' IPOs in the U.S., mainly used for expanding HBM production lines in Cheongju and Yongin, as well as R&D for next-generation HBM5 and 1b nm DRAM processes. As of the end of the first quarter of 2026, the company held monetary funds exceeding 3.2 trillion Korean won, with a debt-to-asset ratio of 26%, indicating a healthy financial structure. This fundraising is more of a strategic global capital deployment rather than a pure capital need. CXMT plans to raise 29.5 billion yuan on the STAR Market, all of which will be invested in DRAM process R&D and capacity expansion. The company currently operates three 12-inch wafer fabs in Hefei and Beijing, with a monthly capacity of approximately 300,000 wafers and a utilization rate exceeding 95%. It aims to increase monthly capacity to 400,000 wafers by the end of 2026, and after the completion of a new fab in Shanghai, it will add another 400,000 to 600,000 wafers of monthly capacity, with a long-term target of 15% to 20% global market share. Compared to SK Hynix, CXMT's fundraising is more urgent and practical, serving as a key source of capital to support its capacity ramp-up and technological catch-up.

While there are still significant gaps between the two companies in terms of technology generation, product high-endization, and global customer coverage, Chinese memory manufacturers have truly stepped onto the main stage of global competition. The AI wave is reshaping the amplitude and structure of the memory cycle. The challenge for SK Hynix lies in how to convert its HBM leadership into long-term technological barriers, while CXMT's challenge is to continuously narrow the technological gap amid cyclical fluctuations, achieving a leap from scale expansion to value upgrade.