Executive Summary

Sludge drying is moving from a disposal-support process to a strategic interface between wastewater treatment, energy recovery and materials management. The market is expanding, but it is not a uniform equipment category: published 2025 estimates range from USD 1.2 billion for narrowly defined drying equipment to approximately USD 3.0 billion for broader industrial sludge-dryer systems. The difference reflects whether a study includes air treatment, heat recovery, granulation, controls, installation and industrial applications beyond municipal sewage sludge.

The strongest commercial driver is not sludge generation alone. A project becomes investable when drying materially changes the downstream route: reducing haulage and landfill mass, producing a stable Class A-type biosolids product, enabling cement-kiln or incinerator co-processing, improving fuel value, or allowing phosphorus and ash recovery. Energy availability therefore determines market quality. Plants with low-grade waste heat, biogas, steam, solar resources or favorable electricity tariffs can support drying economics that are difficult to reproduce at sites dependent on purchased fossil heat.

|

Finding |

Assessment |

|

Market size |

Current public estimates imply a 2025 market range of roughly USD 1.2-3.0 billion, with most forecasts indicating mid-single-digit to low-high-single-digit growth. Scope differences prevent a single precise global figure. |

|

Demand center |

Municipal wastewater remains the largest volume base, while chemicals, pharmaceuticals, pulp and paper, food processing, textiles, mining and refining create higher-value industrial applications. |

|

Technology shift |

Low-temperature belt and heat-pump systems are gaining attention where electricity or waste heat is available; drum, fluid-bed and paddle systems retain advantages in throughput, compactness or end-product quality. |

|

Regional structure |

Europe is the most regulation-intensive mature market; Asia-Pacific combines the largest broad sludge-equipment base with rapid industrial wastewater investment; North America is shaped by disposal economics and biosolids-quality risk. |

|

Competitive advantage |

The defensible offer is an integrated process guarantee covering evaporation capacity, final dry solids, energy consumption, odor and dust control, safety, condensate treatment and downstream product acceptance. |

|

Primary constraint |

Drying is energy-intensive. Inlet cake solids, heat integration and disposal fees have more influence on project economics than nominal dryer purchase price. |

|

Outlook |

Growth to 2034 is likely to be steady rather than explosive. Suppliers positioned around waste-heat integration, low-emission operation, modular systems and full lifecycle service should outperform commodity fabricators. |

1. Scope and Market Definition

This report defines sludge drying equipment as the process systems used after thickening and mechanical dewatering to remove remaining water from municipal or industrial sludge. It includes dryers, feed and discharge systems, air or vapor loops, condensers, odor treatment, controls and selected heat-recovery components. It does not treat all wastewater treatment equipment as part of the dryer market, and it excludes standalone centrifuges, filter presses and screw presses unless supplied within an integrated drying package.

|

Included market layer |

Included in this report |

Boundary issue |

|

Core dryer |

Belt, drum, paddle/disc, fluid-bed, thin-film, solar greenhouse, heat-pump and hybrid systems |

Some market studies count only the dryer body; others include complete process trains. |

|

Balance of plant |

Sludge feeding, mixing, recycle, cooling, product handling, air treatment, condensate and automation |

Project revenue can be materially larger than equipment-only revenue. |

|

End-product systems |

Granulation, pellet cooling, storage and interfaces to incineration, cement kilns, fertilizer or fuel use |

Value depends on whether the dried product has a permitted and bankable outlet. |

|

Services |

Engineering, commissioning, retrofit, process optimization, parts and lifecycle service |

Aftermarket is often excluded from public market estimates. |

|

Excluded categories |

Mechanical dewatering only, generic industrial dryers not designed for sludge, sludge hauling and disposal services |

These adjacent markets are larger and should not be added directly to drying-equipment revenue. |

The market is therefore best understood as a project-engineered subsegment of sludge treatment rather than a catalog-equipment market. Dryer selection depends on water evaporation duty, sludge rheology, corrosivity, sticky-phase behavior, volatile solids, dust explosibility, final product route and available thermal energy.

2. Global Market Size and Forecast

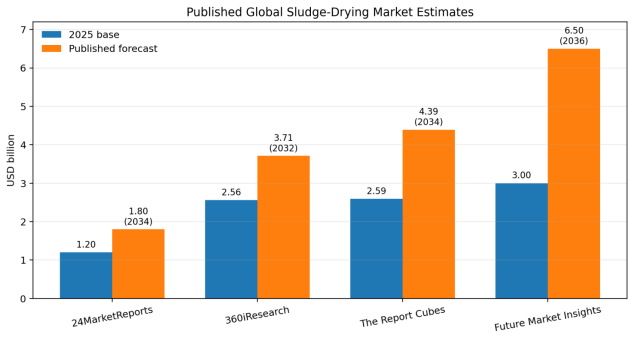

Four recently published estimates illustrate both the commercial scale and the measurement problem. The narrowest equipment definition places the 2025 market at USD 1.2 billion. Broader water-treatment and industrial-sludge definitions place it between USD 2.56 billion and USD 3.0 billion. Forecast growth ranges from 5.3% to 7.2% annually, depending on scope and horizon.

|

Source |

2025 base (USD bn) |

Forecast |

Reported CAGR |

Interpretation |

|

24MarketReports |

1.20 |

USD 1.80 bn by 2034 |

5.3% |

Narrow sludge-drying equipment scope. |

|

360iResearch |

2.56 |

USD 3.71 bn by 2032 |

5.43% |

Water-treatment sludge drying; likely includes wider system content. |

|

The Report Cubes |

2.59 |

USD 4.39 bn by 2034 |

6.03% |

Municipal and industrial drying systems; reports municipal sludge at 52% and Europe at 36%. |

|

Future Market Insights |

3.00 |

USD 6.50 bn by 2036 |

7.2% |

Broad industrial sludge-dryer scope and longer forecast horizon. |

Figure 1. Published global sludge-drying market estimates

Source: 24MarketReports; 360iResearch; The Report Cubes; Future Market Insights. Values are not directly additive because scope differs.

A reasonable publication approach is to avoid presenting a single false-precision number. The defensible conclusion is that dedicated sludge-drying equipment and associated systems represent a low-single-digit-billion-dollar global market in 2025, with a mid-single-digit baseline growth trajectory. The higher forecasts assume broader industrial coverage, greater balance-of-plant revenue and faster adoption of advanced low-temperature systems.

2.1 Revenue pools inside the market

|

Revenue pool |

Typical content |

Growth quality |

|

New municipal installations |

Dryer, air loop, feed system, building, odor control, product handling and commissioning |

Large project values; long procurement cycles and high qualification barriers. |

|

Industrial packaged systems |

Compact heat-pump, belt, paddle or thin-film systems for chemical, food, textile and pharmaceutical sludge |

Faster decisions; feed variability and corrosion create execution risk. |

|

Retrofit and heat integration |

Burner replacement, heat exchangers, control upgrades, air-loop optimization and capacity debottlenecking |

High-margin where installed base is large and energy prices are high. |

|

Aftermarket and service |

Wear parts, belts, paddles, seals, fans, sensors, cleaning, software and process support |

Recurring revenue; depends on installed-base access and response capability. |

3. Demand Base and Structural Drivers

Dryer demand begins with the quantity and disposal cost of dewatered sludge, but the addressable market is shaped by regulation and downstream outlets. Broad sludge treatment equipment markets are substantially larger than the drying segment because most plants still rely on mechanical dewatering, land application, landfill, composting or incineration without full drying.

3.1 A large and persistent dry-solids burden

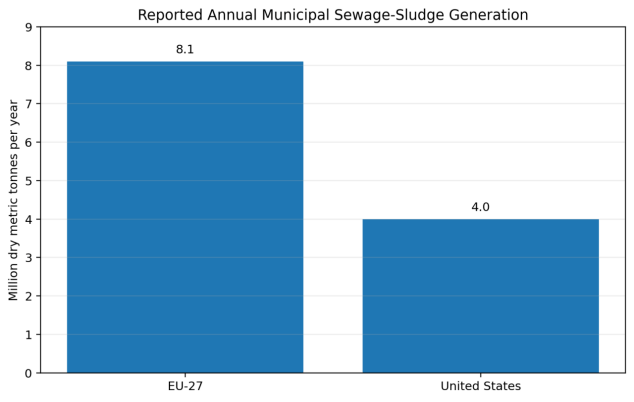

European Commission research estimates that the EU-27 produces approximately 8.1 million tonnes of sewage-sludge dry matter annually. The U.S. EPA reports about 4.0 million dry metric tonnes in 2024 reporting. These figures are not fully comparable because reporting boundaries differ, but they demonstrate a large recurring solids stream that must be transported, reused, destroyed or stored every year.

Figure 2. Reported annual municipal sewage-sludge generation

Source: European Commission Joint Research Centre, approximately 8.1 Mt dry matter for EU-27; U.S. EPA 2024 Biosolids Annual Reports, approximately 4.0 Mt dry metric tonnes. Different reporting boundaries apply.

3.2 Disposal-route volatility creates optionality value

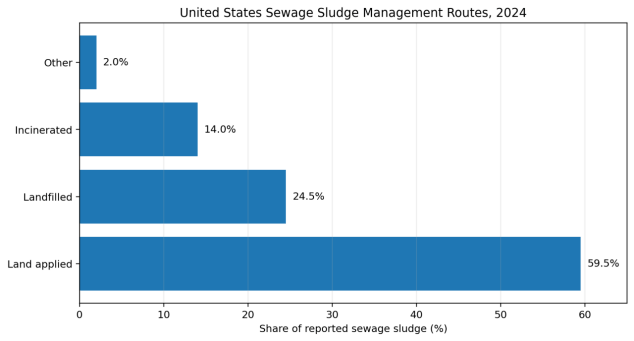

In the United States, 59.5% of reported sewage sludge was land applied in 2024, 24.5% was landfilled, 14% was incinerated and 2% followed other routes. Drying can support all three major pathways: it lowers hauled mass, improves storage stability and combustion behavior, and can create a marketable or distributable product when contaminant and pathogen requirements are met.

Figure 3. United States sewage-sludge management routes, 2024

Source: U.S. Environmental Protection Agency, Biosolids Annual Reports covering 2024.

The commercial value of this optionality is rising as utilities confront PFAS and other contaminant concerns. In June 2026, the U.S. EPA issued draft guidance on reducing risks from PFOA and PFOS in biosolids while emphasizing that land application remains a major national management route. The policy direction does not automatically favor drying, because drying does not destroy all contaminants. It does, however, increase demand for systems that can feed controlled thermal destruction, pyrolysis, gasification or other downstream treatment when land application becomes restricted.

3.3 Regulation and energy policy

|

Driver |

Market implication |

Qualification |

|

EU revised Urban Wastewater Treatment Directive |

More treatment coverage, nutrient and micropollutant removal, resource recovery and energy-neutrality targets increase sludge-management investment. |

The Directive entered into force on 1 January 2025 and targets energy-neutral treatment plants by 2045. |

|

Landfill constraints and gate fees |

Drying reduces transported mass and can avoid wet-sludge acceptance restrictions. |

Economics vary widely by jurisdiction and distance. |

|

Biosolids-quality requirements |

Thermal residence time and final product handling can support Class A-type pathogen reduction. |

Chemical contamination and end-use acceptance require separate verification. |

|

Incineration and co-processing |

Higher dry solids improve autothermal potential and reduce auxiliary fuel demand. |

Drying must be optimized with the furnace, cement kiln or boiler, not designed independently. |

|

Carbon and energy costs |

Waste heat, biogas and renewable electricity improve project viability; purchased thermal energy can destroy returns. |

Energy source and carbon accounting must be included in tender guarantees. |

|

Industrial compliance |

Hazardous, saline, oily, metal-bearing or chemically reactive sludges require specialized enclosed systems. |

Material compatibility and off-gas treatment are often more important than headline throughput. |

4. Technology Landscape

No single dryer architecture dominates all applications. Modern wastewater treatment technology increasingly combines mechanical dewatering, thermal integration, closed-loop air handling and automated control. The relevant comparison is not simply direct versus indirect heat; it is the combination of evaporation efficiency, sludge handling, gas volume, dust risk, footprint and compatibility with the final product route.

|

Technology |

Typical temperature / heat mode |

Best fit |

Main advantages |

Primary constraints |

|

Low-temperature heat-pump belt |

Often about 40-80°C; electricity, recovered heat or hybrid heat pump |

Small to medium municipal and industrial plants; sites needing enclosed modular systems |

Low exhaust temperature, modularity, potentially favorable energy use where electricity is competitive |

Electricity price, refrigerant and compressor maintenance, belt cleaning, slower footprint-intensive duty. |

|

Medium-temperature belt |

Hot air, frequently below 130°C with waste heat; some systems use higher staged temperatures |

Municipal sludge, waste-heat integration, product requiring gentle drying |

Flexible energy sources, low product agitation, scalable throughput |

Large footprint, air-loop equipment, odor control and belt maintenance. |

|

Drum dryer |

Direct convective hot gas; often high throughput |

Large municipal plants, granulated fuel or fertilizer product |

High capacity, integrated granulation, 90-95% DS products possible |

Dust and explosion protection, recycle complexity, high gas volume and odor treatment. |

|

Paddle / disc dryer |

Indirect steam, thermal oil or hot water; optional vacuum |

Sticky, hazardous or odor-sensitive industrial sludge; compact plants |

Low off-gas volume, compact footprint, high heat-transfer area, enclosed operation |

High torque through sticky phase, wear, shaft-seal maintenance and sensitivity to hard contaminants. |

|

Fluid-bed dryer |

Convective gas through fluidized granules |

Uniform granules and large continuous plants |

Strong heat and mass transfer, uniform product, good thermal integration |

Complexity, dust control, product fluidization behavior and capital intensity. |

|

Thin-film dryer |

Indirect heated surface with rotor or wiper |

Difficult pastes, chemical sludge and compact continuous duty |

Short residence time, compact equipment, limited gas volume |

Mechanical wear, feed pretreatment, high-quality maintenance. |

|

Solar greenhouse dryer |

Solar radiation with mechanical turning and ventilation |

Dry climates, land-rich sites and lower throughput |

Low purchased heat, simple concept, potential renewable integration |

Weather dependence, large land requirement, odor, long residence time and seasonal capacity. |

4.1 Belt systems: energy flexibility versus footprint

ANDRITZ describes its belt drying system as a low-temperature, closed-circulation system able to use low-grade waste energy, with drying air below 130°C. Veolia's Biocon system uses staged hot-air ranges and can reach approximately 90% dryness, with residence time designed to support disinfection. Belt systems are commercially attractive where the site can recover low-grade heat from engines, incineration, industrial processes or district-energy systems.

4.2 Indirect systems: compactness and low off-gas

Paddle and disc dryers transfer heat through metal surfaces rather than large volumes of hot air. ANDRITZ and Komline-Sanderson emphasize compact footprints, high heat-transfer efficiency and low off-gas volumes. These attributes are valuable for chemical or hazardous sludge, but procurement teams must test behavior through the plastic or sticky phase, verify torque margin and specify materials against chlorides, sulfur compounds, solvents and abrasive minerals.

4.3 Drum and fluid-bed systems: scale with safety obligations

Drum dryers remain relevant for large throughput and granulated end products. ANDRITZ reports 90-95% dry solids for its drum system and explicitly designs around explosive-atmosphere and ignition-source controls. Large direct systems can deliver robust economics at scale, but the balance of plant - hot-gas generation, recycle, dust collection, cooling, storage and explosion protection - is a major part of project cost and risk.

Air-loop design requires careful selection of the centrifugal fan, ducting, condenser and odor-control train. Fan power, fouling and corrosion can materially change lifecycle cost even when the dryer core meets its evaporation guarantee.

5. Process Economics and Mass Reduction

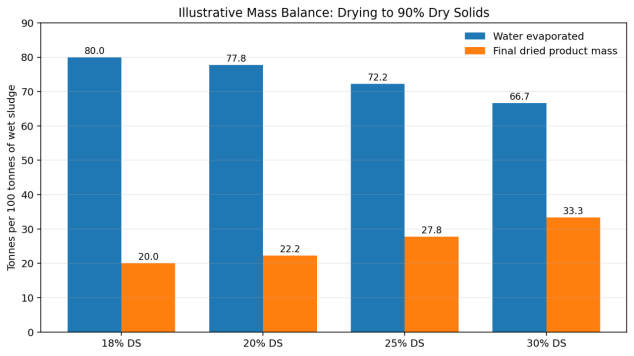

Dryer economics are fundamentally a water-evaporation calculation. A plant processing 100 tonnes per day of sludge cake at 20% dry solids contains 20 tonnes of solids and 80 tonnes of water. Drying to 90% dry solids produces approximately 22.2 tonnes of final material, requiring about 77.8 tonnes of water to be evaporated. Raising inlet cake solids before the dryer is therefore one of the highest-value optimization measures.

Figure 4. Illustrative mass balance for drying to 90% dry solids

Source: Wedoany calculation. Basis: 100 tonnes wet sludge; dry-solids mass conserved; no solids loss. Actual systems may have dust, condensate and product recycle streams.

The U.S. EPA reports that conventional heat-drying systems can require approximately 1,400-1,700 Btu per pound of water evaporated, equivalent to roughly 0.90-1.10 kWh of thermal energy per kilogram of water. This is an indicative historical benchmark rather than a universal guarantee. Modern waste-heat, heat-pump and high-recovery systems can improve purchased-energy performance, but vendor claims must state whether consumption is measured per tonne of wet sludge, dry solids or evaporated water.

|

Economic variable |

Why it matters |

Tender requirement |

|

Inlet dry solids |

Each additional point of mechanical dewatering reduces evaporation load and dryer size. |

Guarantee average and minimum cake DS across seasons and sludge blends. |

|

Heat source |

Waste heat, biogas, steam, hot water, natural gas and electricity have different cost and carbon profiles. |

Provide energy balance by source, temperature and operating load. |

|

Disposal or outlet fee |

Avoided hauling and gate fees are often the largest cash benefit. |

Use contracted or verified local rates, not generic assumptions. |

|

Operating hours |

Continuous large systems and batch modular systems have different redundancy requirements. |

Specify annual availability, turndown and maintenance outages. |

|

Final dry solids |

Higher dryness reduces mass but can increase dust, energy and fire risk. |

Define permitted range and downstream acceptance criteria. |

|

Condensate and off-gas |

Evaporated water carries ammonia, VOCs and odor compounds. |

Include condensate quality and air-treatment guarantees. |

|

Wear and corrosion |

Industrial sludge may contain grit, salts, acids, alkalis, oils or solvents. |

Require feed analysis, material selection and wear-part life assumptions. |

|

Labor and automation |

Dryers are process plants, not unattended boxes. |

Define staffing, remote diagnostics, alarms and manual intervention. |

Heat recovery should be engineered around correctly sized Heat Exchangers, condenser approach temperatures, fouling allowances and cleaning access. A nominal waste-heat source has limited value if its temperature, availability or seasonal profile does not match the dryer duty.

6. End-Use Industry Analysis

|

End-use sector |

Sludge characteristics |

Commercial case for drying |

Key qualification |

|

Municipal wastewater |

Biological sludge, often digested; variable polymer and grit |

Haulage reduction, Class A-type product, incineration or nutrient recovery |

Pathogens, PFAS and end-market acceptance. |

|

Chemicals and pharmaceuticals |

Potentially saline, toxic, solvent-bearing or reactive |

Volume reduction, secure destruction feed, controlled handling |

Hazardous classification, VOC control, corrosion and explosion risk. |

|

Pulp and paper |

Fibrous, high-volume sludge with variable ash |

Boiler or kiln fuel, landfill reduction, waste-heat use |

Fiber handling, ash content and calorific value. |

|

Food and beverage |

High organic content; odor and rapid biological degradation |

Stable product, fuel or soil use where permitted |

Hygiene, odor, fat and protein fouling. |

|

Textile and dyeing |

High color, salts and chemical residues |

Lower disposal mass and integration with industrial steam systems |

Corrosion, condensate treatment and product disposal. |

|

Metals and mining |

Mineral, abrasive and potentially metal-bearing sludge |

Concentrated residue, smelter or cement integration, water recovery |

Abrasive wear, heavy metals and low fuel value. |

|

Oil, gas and refining |

Oily sludge, hydrocarbons and high hazard potential |

Preconditioning for thermal destruction or recovery |

VOC, fire, explosion and hazardous-waste permitting. |

|

Drinking-water treatment |

Alum, ferric or lime sludge with low organic content |

Transport reduction and possible mineral reuse |

Low fuel value, chemical recovery and local end uses. |

Municipal systems provide the largest repeatable equipment opportunity, but industrial applications often support better margins because standard dryers cannot safely handle the feed without materials, sealing and air-treatment customization. Suppliers should resist using municipal reference data for industrial sludge without pilot tests or representative drying curves.

7. Regional Market Outlook

|

Region |

Market position |

Primary drivers |

Commercial constraints |

|

Europe |

Mature and regulation-intensive; one 2026 study reports 36% of the water-treatment sludge-drying market. |

Landfill reduction, energy-neutral wastewater plants, incineration, phosphorus recovery and established district/waste-heat networks. |

High engineering standards, permitting, lifecycle carbon scrutiny and strong incumbents. |

|

Asia-Pacific |

Largest broad sludge-treatment equipment base; dense industrial and municipal demand. |

Urban wastewater expansion, industrial compliance, large manufacturing supply chain and rapid adoption of low-temperature systems. |

Price competition, project quality variation, electricity mix and fragmented disposal practices. |

|

North America |

Large installed wastewater base with diverse land-application, landfill and incineration routes. |

Hauling economics, Class A biosolids, PFAS-related route uncertainty, aging solids infrastructure. |

Long municipal procurement, state-level rule differences and public acceptance. |

|

Middle East |

Selective high-value market, especially large municipal plants and industrial zones. |

Water reuse, centralized treatment, solar resources, desalination and refinery/petrochemical sludge. |

Heat, dust, corrosion, limited end-product outlets and dependence on imported service. |

|

Latin America |

Project-driven growth around major cities, pulp and paper, mining, food and chemicals. |

Landfill logistics, industrial compliance and infrastructure investment. |

Financing, power cost, municipal credit quality and service coverage. |

|

Africa |

Early-stage and highly selective; solar and modular approaches can be relevant. |

Urban sanitation investment, industrial parks and reduced transport burden. |

Capital constraints, operator capacity, spare parts and limited downstream outlets. |

7.1 Europe

Europe's strategic demand is increasingly linked to the full resource-recovery chain. The revised EU Urban Wastewater Treatment Directive requires broader collection and treatment, tighter nutrient and micropollutant removal, circular resource recovery and energy-neutrality by 2045. Drying systems that consume purchased high-carbon heat face a more difficult investment case than systems integrated with digestion, combined heat and power, waste heat, incineration or industrial heat networks.

7.2 Asia-Pacific

Asia-Pacific combines scale and supplier diversity. Fortune Business Insights places the region at 38% of the broader sludge treatment and handling equipment market in 2025, while Grand View Research reports a 33.9% share of sludge dewatering equipment in 2024. These are adjacent-market indicators rather than dryer-specific shares, but they support the conclusion that the region has the largest equipment demand base. Growth quality will vary by power price, disposal regulation and the availability of industrial waste heat.

7.3 North America

North American procurement is increasingly route-sensitive. Utilities that can continue cost-effective land application may not justify full drying, while plants facing long hauling distances, landfill constraints, product-distribution goals or thermal treatment can generate strong projects. PFAS policy uncertainty increases the value of flexible systems, but drying alone should never be presented as contaminant destruction.

8. Competitive Landscape and Business Models

The market is moderately concentrated among global process specialists at large municipal scale and fragmented among regional manufacturers in packaged industrial systems. No reliable public global market-share ranking is available, and company presence varies by dryer architecture and geography.

|

Supplier / group |

Relevant positioning |

Commercial strength |

Watch item |

|

ANDRITZ |

Belt, drum, paddle and fluid-bed drying; global sludge and separation portfolio |

Breadth of technology, large references, waste-heat integration and process engineering |

Large-project complexity and premium engineering cost. |

|

Veolia Water Technologies |

Biocon belt drying and integrated combustion/energy-recovery systems |

Municipal process integration, Class A product positioning and full treatment capability |

Project availability varies by region and contracting model. |

|

HUBER |

Municipal sludge treatment, solar and thermal-drying solutions in integrated plant context |

Strong wastewater installed base and municipal relationships |

Dryer portfolio and local delivery scope should be verified per market. |

|

Komline-Sanderson |

Indirect paddle dryers and biosolids systems |

Compact low-off-gas design, difficult-feed handling and North American references |

Mechanical wear, torque and service access. |

|

GEA / Alfa Laval |

Thermal process and sludge-treatment capabilities in broader portfolios |

Heat-transfer, separation and global industrial customer access |

Specific sludge-dryer offering varies by region and project. |

|

Shincci |

Low-temperature heat-pump and waste-heat sludge dryers |

Modular product range, industrial references and energy-efficiency positioning |

Performance basis and local service must be independently verified. |

|

LCI / regional thin-film specialists |

Thin-film and compact indirect drying |

Difficult sludge, short residence time and industrial customization |

Niche scale and rotor/wear maintenance. |

|

Centrifuge and dewatering OEMs |

Integrated dewatering-drying packages and channel partnerships |

Ability to optimize inlet cake DS and offer one process guarantee |

Dryer technology may be partner-supplied. |

|

Regional fabricators |

Belt, rotary and heat-pump systems at competitive capital cost |

Customization, price and local manufacturing |

Reference quality, safety certification and lifecycle service. |

8.1 Where margins are defendable

|

Business model |

Value proposition |

Margin defense |

|

Equipment-only sale |

Lower capital price and local fabrication |

Weak unless protected by proprietary internals, controls or references. |

|

Engineered package |

Dryer plus air loop, feed, heat recovery and automation |

Stronger because interfaces and guarantees are controlled. |

|

EPC / turnkey plant |

Complete buildings, utilities, odor, storage and downstream integration |

High revenue, but schedule and civil-risk exposure is substantial. |

|

Retrofit and optimization |

Capacity increase, burner/heat-pump conversion, controls and heat recovery |

Attractive installed-base economics and shorter decision cycles. |

|

O&M / service agreement |

Availability, energy and product-quality support |

Recurring revenue and customer retention. |

|

Performance-based or DBO model |

Payment linked to treated tonnes, energy or disposal savings |

Potentially strong but requires financing, feed-risk allocation and bankable outlets. |

9. Procurement Specification and Project Risk

A sludge dryer should be procured as a guaranteed process train. A tender based only on wet-tonne capacity and final moisture invites disputes because evaporation duty and feed behavior can change sharply with inlet solids, temperature, polymer, ash, oil, salt and seasonal sludge blend.

|

Specification item |

Minimum information |

Reason |

|

Feed basis |

Wet tonnes/day, dry solids/day, average and minimum inlet DS, sludge sources and blending ratios |

Defines evaporation duty and prevents capacity ambiguity. |

|

Physical behavior |

Particle size, viscosity, sticky-phase range, grit, fibers and foreign objects |

Determines feeding, torque, fouling and cleaning. |

|

Chemical profile |

pH, chlorides, sulfur, ammonia, heavy metals, solvents, oils and VOCs |

Determines materials, corrosion, off-gas and safety design. |

|

Thermal basis |

Heat-source temperature, flow, annual availability and backup fuel |

Determines purchased energy and achievable capacity. |

|

Product guarantee |

Final DS range, particle size, pathogen target, temperature, odor, dust and bulk density |

Links dryer output to storage and final outlet. |

|

Energy guarantee |

Thermal and electrical energy per kg water evaporated, at defined conditions |

Allows fair lifecycle comparison. |

|

Air and condensate |

Exhaust flow, NH3/VOC/odor limits, condensate volume and quality |

Prevents hidden treatment costs. |

|

Safety |

ATEX/NFPA zoning, fire detection, explosion protection, inerting, shutdown logic and product cooling |

Critical for dry organic solids and hot gas systems. |

|

Availability |

Guaranteed operating hours, turndown, redundancy, cleaning and maintenance duration |

Defines real annual throughput. |

|

Testing |

Representative pilot test or reference-feed validation; acceptance method and instruments |

Reduces scale-up and feed-variability risk. |

|

Lifecycle support |

Wear parts, belt/shaft/seal life, remote diagnostics, local service and training |

Prevents long outages and unavailable spares. |

Product handling is often underestimated. The Belt Conveyor, screw conveyors, cooling stage, storage silo and truck-loading system must be designed for dust, bridging, self-heating and variable granule strength, not treated as generic bulk-solids auxiliaries.

9.1 Risk matrix

|

Risk |

Probability |

Impact |

Mitigation |

|

Feed sludge differs from design sample |

High |

High |

Use long-duration composite sampling, pilot testing and contractual feed envelope. |

|

Energy source unavailable or lower temperature |

Medium |

High |

Guarantee heat-source conditions; provide backup and derating curves. |

|

Sticky-phase fouling or torque overload |

Medium |

High |

Pilot test; recycle strategy; torque margin; cleaning and access. |

|

Odor/VOC/condensate non-compliance |

Medium |

High |

Mass balance, contaminant testing and guaranteed treatment train. |

|

Dried product lacks permitted outlet |

Medium |

High |

Secure outlet and quality criteria before final investment decision. |

|

Dust fire or explosion |

Low-Medium |

Very high |

ATEX/NFPA design, cooling, housekeeping, detection and suppression. |

|

Corrosion and wear exceed assumptions |

Medium |

Medium-High |

Material coupons, feed chemistry, replaceable wear zones and warranty. |

|

Vendor service unavailable |

Medium |

Medium-High |

Local parts stock, remote support, training and response-time agreement. |

10. Outlook to 2034

The most likely global trajectory is steady expansion supported by wastewater infrastructure, disposal constraints and resource-recovery policy. The market should not be modeled as a simple function of wastewater-treatment capacity: many plants will continue using dewatering without drying, while a smaller number of high-value projects will account for a large share of revenue.

|

Scenario |

Market logic |

Implication for suppliers |

|

Base case |

Mid-single-digit growth; gradual municipal upgrades; industrial compliance; moderate waste-heat integration |

Build regional service, modular products and verified lifecycle guarantees. |

|

High-growth case |

Faster restrictions on land application and landfill, high disposal fees, stronger carbon incentives and waste-heat projects |

Integrated drying plus thermal destruction/resource recovery gains share. |

|

Low-growth case |

Low landfill costs, weak enforcement, high electricity/gas prices and constrained municipal budgets |

Retrofit, mobile systems and low-capex dewatering dominate over new dryers. |

Strategic conclusions

- Market size must be communicated as a range. Public 2025 estimates differ by more than two times because equipment-only and complete-system scopes are mixed.

- Energy integration is the core competitive variable. A dryer without a credible heat and power strategy is rarely a strong project, regardless of capital price.

- Higher inlet cake solids are often the cheapest capacity expansion. Dryer vendors that optimize dewatering and drying together can create superior economics.

- Low-temperature systems will continue gaining share in modular industrial and medium municipal applications, but large drum, fluid-bed and indirect systems retain defensible niches.

- Regulatory uncertainty increases the value of route flexibility. Drying can support land application, storage, fuel and thermal destruction, but it does not by itself solve contaminant risk.

- The product guarantee must extend beyond final moisture. Energy, emissions, condensate, safety, availability and downstream acceptance determine lifecycle value.

- The best suppliers will combine process knowledge, local service and installed-base optimization rather than compete only on fabricated equipment cost.

Methodology and Sources

The report triangulates current public market-research estimates with official sludge-generation and regulatory data, government technology guidance and supplier technical literature. Market estimates are presented separately rather than averaged mechanically because their scope differs. Calculated mass-balance values assume conservation of dry solids and are explicitly labeled as Wedoany calculations.

- 24MarketReports. Global Sludge Drying Equipment Market, 2026 forecast to 2034.2025 value USD 1.2 billion; 2034 forecast USD 1.8 billion; 5.3% CAGR.

- 360iResearch. Water Treatment Sludge Drying Market - Global Forecast 2026-2032. Published June 2026; 2025 value USD 2.56 billion; 2032 forecast USD 3.71 billion.

- The Report Cubes. Global Water Treatment Sludge Drying Market Outlook 2034. 2025 value USD 2.59 billion; 2034 forecast USD 4.39 billion; reported Europe share 36%.

- Future Market Insights. Industrial Sludge Dryer Market 2026-2036. 2025 value USD 3.0 billion; 2036 forecast USD 6.5 billion; 7.2% CAGR.

- U.S. Environmental Protection Agency. Basic Information about Sewage Sludge and Biosolids.2024 generation and management-route statistics.

- U.S. Environmental Protection Agency. Fact Sheet: Heat Drying.Technology, performance and energy guidance; page updated December 2025.

- U.S. Environmental Protection Agency. Draft Guidance for Reducing Risk from PFOA and PFOS in Biosolids.Published June 2026.

- European Commission. Urban Wastewater.Revised Directive entered into force 1 January 2025; energy-neutrality target by 2045.

- European Commission. Sewage Sludge.EU sludge policy and agricultural-use framework.

- European Commission Joint Research Centre. Feasibility study in support of future policy developments of the Sewage Sludge Directive.Approximately 8.1 million tonnes of sewage-sludge dry matter generated annually in EU-27.

- ANDRITZ. Thermal systems for sludge drying and recycling. Belt, drum, paddle and fluid-bed process information.

- ANDRITZ. Belt drying system BDS for sludge. Waste-heat and low-temperature belt drying.

- ANDRITZ. Drum drying system DDS. 90-95% dry-solids product and safety concept.

- ANDRITZ. Gouda paddle dryer. Indirect drying, compact footprint, low off-gas and technical specifications.

- Veolia Water Technologies. Biocon ERS. Belt drying, 90% dryness and integrated energy recovery.

- Komline-Sanderson. Biosolids/Sludge Dryer.Indirect paddle drying and feed-handling characteristics.

- Shincci Global. Heat Pump/Waste Heat Sludge Dryer.Vendor-reported low-temperature system parameters; claims require project-specific verification.

- Fortune Business Insights. Sludge Treatment and Handling Equipment Market. Adjacent market benchmark; Asia-Pacific 38% share in 2025.

- Grand View Research. Sludge Dewatering Equipment Market. Adjacent market benchmark; Asia-Pacific 33.9% share in 2024.

Data cut-off: 16 July 2026. Public market estimates may be revised by publishers. No unsupported vendor market-share ranking is used. Vendor technical claims are treated as configuration-specific information and should be verified during procurement.