1. Market Definition and Measurement Scope

Gravimeters measure gravitational acceleration or changes in the local gravity field. In commercial geophysics, a distinction must be made between absolute instruments, which determine gravity in SI-traceable terms, and relative instruments, which measure differences between stations. Dynamic systems add inertial navigation, stabilization and motion correction for aircraft or vessels. Gravity gradiometers measure spatial gradients and are adjacent to, but not identical with, conventional gravimeters.

|

Instrument class |

Measurement principle |

Primary role |

Key limitation |

|

Relative land gravimeter |

Spring/quartz sensor |

Dense terrestrial surveys, microgravity, exploration |

Drift and need for reference ties |

|

Free-fall absolute gravimeter |

Laser interferometry of falling test mass |

National standards, geodesy, calibration |

Sensitive to vibration; setup and logistics |

|

Superconducting gravimeter |

Levitated superconducting sphere |

Continuous observatory monitoring |

Not an absolute instrument; infrastructure intensive |

|

Cold-atom quantum gravimeter |

Atom interferometry |

Continuous absolute measurement, emerging field surveys |

Cost, complexity and service ecosystem |

|

Dynamic airborne/marine gravimeter |

Stabilized or strapdown inertial sensing |

Large-area mapping from moving platforms |

Motion correction and navigation integration |

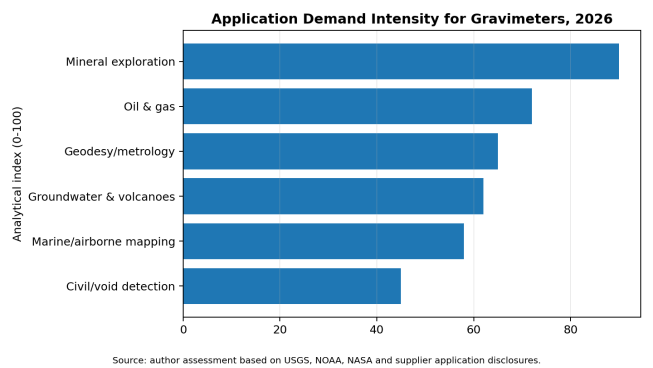

Figure 1. Application demand intensity. The index is analytical rather than a revenue estimate.

2. Global Market Structure and Demand Drivers

The gravimeter market is project-driven. Mineral exploration programs purchase or rent relative instruments and frequently procure survey services rather than instruments. National mapping and metrology agencies acquire absolute instruments in small numbers and retain them for long operating lives. Observatory networks use superconducting systems for continuous records. Airborne and marine instruments are often embedded in complete survey platforms, meaning that the equipment price is only one element of a much larger data-acquisition contract.

Demand is supported by renewed critical-mineral exploration, improved geoid and height reference systems, groundwater-storage monitoring, volcanic and crustal-deformation research, offshore resource mapping, and defense/navigation research. Constraints include the substitution of some reconnaissance work by satellite gravity data, high operator skill requirements, slow public procurement, limited calibration infrastructure and competition from seismic, electromagnetic and magnetic methods.

3. Regional Market Structure

|

Region |

Demand base |

Most attractive segments |

Entry considerations |

|

North America |

USGS/NOAA research, mining, groundwater, oil and gas, quantum programs |

Relative land, absolute reference, airborne, quantum |

Strong technical requirements; service and calibration credibility essential |

|

Europe |

Metrology institutes, geodesy, volcanology, civil infrastructure, quantum R&D |

Absolute, superconducting, quantum, marine |

CE compliance, public tenders, research partnerships |

|

China |

Geological surveys, mining, geodesy, domestic instrumentation programs |

Relative, dynamic, quantum |

Localization, institutional relationships, domestic standards |

|

Japan & Korea |

Earth science, metrology, disaster monitoring, precision instrumentation |

Absolute, superconducting, quantum |

High reliability and local support expectations |

|

Australia |

Mineral exploration and regional geophysics |

Relative land, airborne |

Rental/service model attractive; harsh-field robustness |

|

Middle East |

Oil and gas, groundwater, infrastructure and geodesy |

Relative, absolute, dynamic |

Project-based demand and local partner value |

|

Latin America |

Mining, volcanoes, groundwater and national mapping |

Relative, absolute, monitoring |

Financing, import logistics and training |

|

Africa |

Minerals, groundwater, geological mapping |

Relative land, airborne services |

Budget constraints favor services, rental and donor-backed programs |

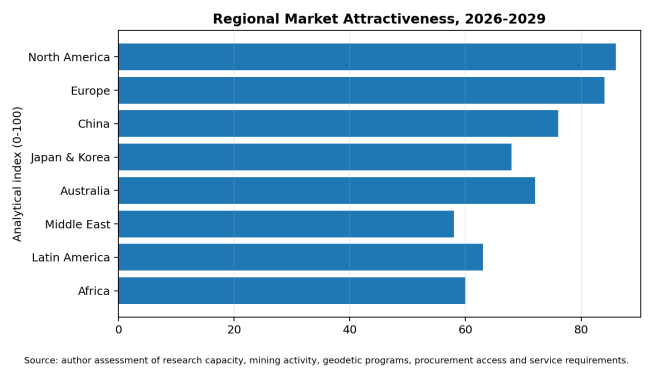

Figure 2. Regional attractiveness index, 2026-2029. Analytical assessment, not a market-share estimate.

4. Technology Roadmap and Product Evolution

The key industry transition is from mechanically referenced relative measurement toward hybrid and absolute sensing. Spring gravimeters will remain important because they are portable, proven and efficient for dense grids. Their weakness—instrument drift—can be reduced through repeated base ties, loop design and periodic calibration. Absolute free-fall systems provide traceability but are less convenient in harsh or highly mobile environments. Superconducting gravimeters provide exceptional long-term stability but still require absolute calibration. Cold-atom instruments can deliver drift-free absolute measurements and continuous operation, making them strategically important for volcanology, hydrology, civil engineering and future mobile platforms.

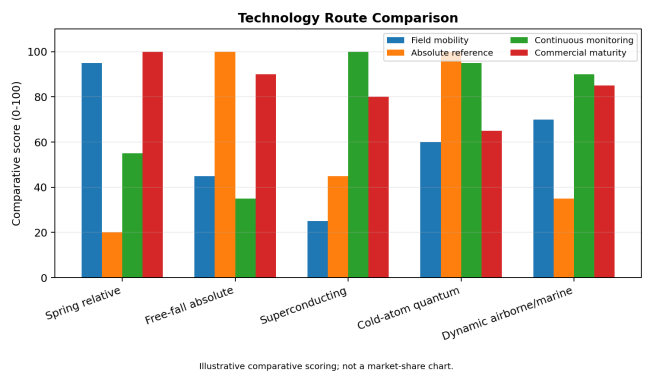

Figure 3. Comparative technology scoring. Scores summarize functional positioning and are not laboratory test results.

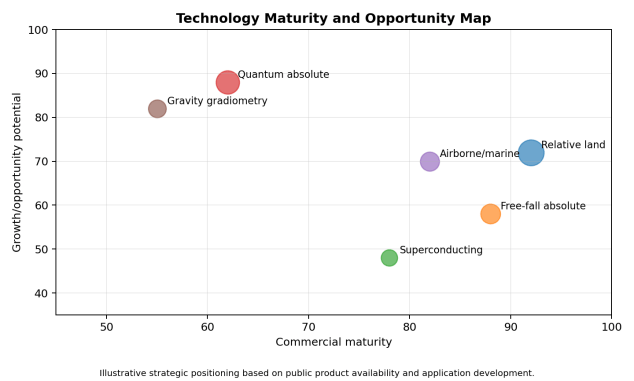

Figure 4. Technology maturity and opportunity map.

5. Cost, Pricing and Project Economics

Public list prices are uncommon because gravimeters are sold with configuration-specific accessories, training, transport cases, software, calibration and service. A buyer should therefore avoid comparing a bare sensor quotation with a complete delivered survey system. For dynamic systems, navigation hardware, stabilized platforms, aircraft integration, certification and post-processing can exceed the sensor cost. For absolute and quantum systems, vibration isolation, environmental control and expert commissioning may materially affect total cost.

The lifecycle cost is shaped by calibration frequency, sensor drift, downtime, international shipping for repair, proprietary software, helium or cryogenic support for some superconducting systems, operator training and the need for repeat surveys. Rental or survey-as-a-service is often economically superior for intermittent mineral or marine campaigns, while ownership is more defensible for national agencies, observatories and contractors with sustained utilization.

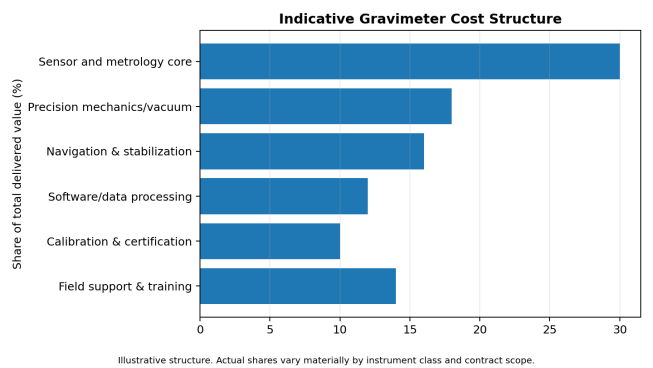

Figure 5. Indicative cost structure by delivered value. Actual shares vary significantly by technology.

6. Value Chain and Supply Structure

|

Value-chain stage |

Critical capabilities |

Commercial pressure |

Opportunity |

|

Core sensing |

Quartz/spring mechanics, laser interferometry, superconducting sensors, atom optics |

Very high technical barriers; low volumes |

Premium sensors, ruggedization, reduced drift |

|

Precision subsystems |

Vacuum, optics, electronics, inertial navigation, thermal control |

Specialized suppliers; long lead times |

Modular subsystems and dual sourcing |

|

System integration |

Mechanical design, stabilization, firmware and correction models |

Certification and field-validation burden |

Turnkey application packages |

|

Software and processing |

Tide, pressure, tilt, terrain, motion and drift corrections |

Increasing differentiation |

Cloud workflows, automated QA and AI-assisted interpretation |

|

Calibration and metrology |

Reference stations, comparison campaigns, traceability |

Geographically concentrated |

Regional calibration centers |

|

Survey services |

Field crews, aircraft/vessel access, geological interpretation |

Project cyclicality |

Rental, managed surveys and recurring monitoring |

|

After-sales support |

Repair, spare parts, training and upgrades |

Supplier concentration |

Local service hubs and multi-year support |

The supplier base is concentrated. Scintrex is a prominent provider of relative land gravimeters; Micro-g LaCoste supplies free-fall absolute and dynamic systems; GWR Instruments supplies superconducting gravimeters; Exail and AOSense are active in atom-interferometric instruments; Sander Geophysics and iMAR are associated with airborne gravimetry systems and services. Competitive advantage depends less on production scale than on calibration pedigree, field references, software, operator support and the ability to keep instruments operational over long service lives.

7. Competitive Landscape

|

Supplier / ecosystem |

Publicly visible position |

Strength |

Buyer diligence point |

|

Scintrex |

CG-6 relative land gravimeter |

Established field workflow and quartz-sensor heritage |

Service coverage, calibration and long-term parts support |

|

Micro-g LaCoste |

FG5-X, A10, marine and dynamic systems |

Absolute-gravity and mobile-platform portfolio |

Configuration, vibration environment and training scope |

|

GWR Instruments |

Superconducting gravity meters |

Continuous high-stability monitoring |

Site infrastructure and absolute calibration plan |

|

Exail |

Commercial absolute quantum gravimeter |

Continuous absolute cold-atom measurement |

Field references, support model and total installed scope |

|

AOSense |

Atom-optic gravimeter technology |

Quantum sensing expertise |

Commercial readiness and application-specific integration |

|

Sander Geophysics / iMAR / DgS ecosystems |

Airborne and dynamic gravimetry |

Navigation, stabilization and survey integration |

Platform compatibility and processing methodology |

|

Chinese emerging suppliers |

Relative and dynamic systems; expanding quantum research |

Localization and cost competitiveness |

Independent validation, calibration traceability and export support |

8. International Market Entry and Export Opportunities

New entrants are unlikely to win by copying a mature mechanical gravimeter alone. More attractive positions include ruggedized quantum systems, inertial-navigation integration, automated field correction, hybrid absolute-relative survey workflows, compact systems for drones or unmanned vessels, calibration services, regional repair centers and application-specific packages for groundwater, carbon storage, mining and civil void detection.

Direct export is viable for portable relative instruments and standardized accessories where local training can be delivered. Absolute, superconducting and quantum systems generally require consultation, site qualification, commissioning and long-term technical support. Airborne and marine markets are more effectively entered through survey contractors, aircraft/vessel integrators or joint projects with geological agencies. Exporters should prepare English technical documentation, software support, calibration records, warranty procedures, spare-parts plans and clear rules for controlled or dual-use components.

9. Procurement and Project Implications

- Define whether the project requires absolute gravity, relative differences, gradients or dynamic measurements.

- Specify target repeatability, noise floor, sampling time and acceptable drift under realistic field conditions.

- Confirm environmental limits for temperature, vibration, tilt, humidity, altitude and transport shock.

- Require a complete correction workflow covering tides, atmospheric pressure, polar motion, terrain, elevation and platform motion where applicable.

- Compare delivered-system scope: sensor, tripod/platform, navigation, batteries, software, cases, training, calibration and commissioning.

- Assess reference-station access and the method for tying relative surveys to absolute gravity.

- Include acceptance tests, repeat-line tests, crossovers and reference-site measurements in the contract.

- Obtain repair turnaround commitments, spare-parts availability and remote diagnostic capability.

- Evaluate data ownership, processing transparency and export-control restrictions.

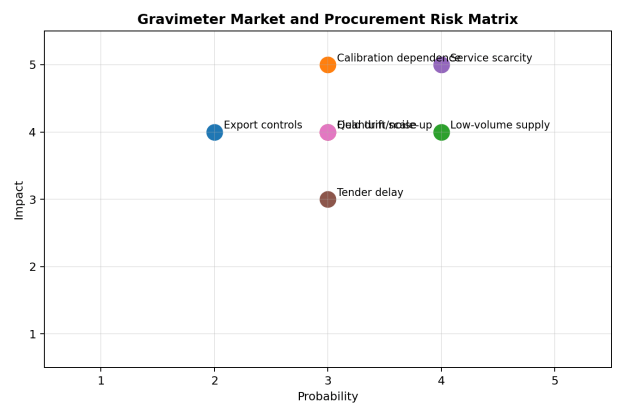

10. Risks and Mitigation

Figure 6. Market and procurement risk matrix.

|

Risk |

Why it matters |

Mitigation |

|

Calibration dependence |

Untraceable or poorly tied data can invalidate long-term comparisons |

Specify calibration chain, reference sites and comparison intervals |

|

Low-volume supply |

Long lead times and limited spare parts |

Framework agreements, critical spares and service-level clauses |

|

Field noise and drift |

Nominal sensitivity may not be achieved in real conditions |

Site tests, loop closure, repeat lines and environmental logging |

|

Service scarcity |

International repair can cause long downtime |

Local partner, loan unit, remote diagnostics and operator training |

|

Tender/project delay |

Public science procurement is slow and budget-sensitive |

Stage-gated bids and validity clauses |

|

Quantum scale-up risk |

New systems may have limited field history |

Pilot deployment, acceptance milestones and performance guarantees |

|

Trade/export controls |

Precision inertial and quantum components may be regulated |

Early classification and licensing review |

11. Outlook to 2030

The gravimeter market should grow in technical value faster than in unit volume. Mature relative instruments will continue to serve mineral exploration and microgravity surveys, but buyers will expect better automation, lower drift, easier data integration and stronger service. Absolute free-fall and superconducting systems will remain essential reference technologies. The largest structural change will come from cold-atom sensors, particularly where continuous absolute measurement can replace periodic campaigns or strengthen hybrid surveys.

Commercial growth will depend on whether quantum systems can demonstrate repeatable performance outside laboratories, reduce commissioning complexity and build regional service capacity. At the same time, increased demand for critical minerals, groundwater accountability, carbon-storage monitoring, geodetic modernization and resilient navigation should broaden the application base. The winning suppliers will be those that combine credible metrology with field usability, software transparency and lifecycle support.