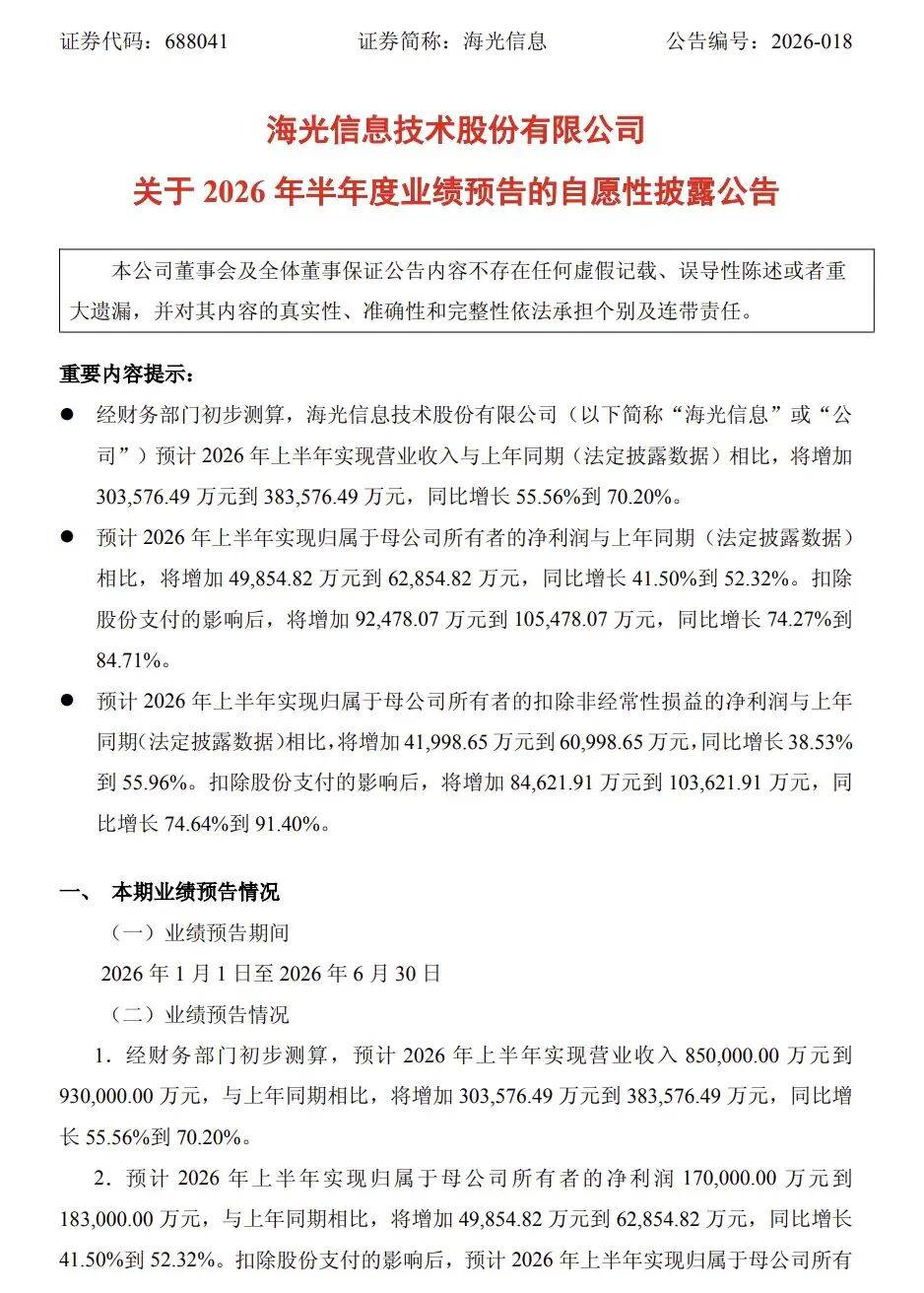

en.Wedoany.com Reported - On the evening of July 16, domestic CPU manufacturer Hygon Information released its semi-year performance forecast for 2026. According to preliminary calculations by the financial department, the company expects to achieve operating revenue of 8.5 billion yuan to 9.3 billion yuan in the first half of 2026, an increase of 3,035.7649 million yuan to 3,835.7649 million yuan compared to the same period last year, representing a year-on-year growth of 55.56% to 70.20%.

It is expected that the net profit attributable to shareholders of the parent company in the first half of 2026 will be 1.7 billion yuan to 1.83 billion yuan, an increase of 498.5482 million yuan to 628.5482 million yuan compared to the same period last year, representing a year-on-year growth of 41.50% to 52.32%. After deducting the impact of share-based payments, the net profit attributable to shareholders of the parent company in the first half of 2026 is expected to be 2.17 billion yuan to 2.3 billion yuan, an increase of 924.7807 million yuan to 1,054.7807 million yuan compared to the same period last year (statutory disclosure data), representing a year-on-year growth of 74.27% to 84.71%.

It is expected that the net profit attributable to shareholders of the parent company after deducting non-recurring gains and losses in the first half of 2026 will be 1.51 billion yuan to 1.7 billion yuan, an increase of 419.9865 million yuan to 609.9865 million yuan compared to the same period last year, representing a year-on-year growth of 38.53% to 55.96%. After deducting the impact of share-based payments, the net profit attributable to shareholders of the parent company in the first half of 2026 is expected to be 1.98 billion yuan to 2.17 billion yuan, an increase of 846.2191 million yuan to 1,036.2191 million yuan compared to the same period last year (statutory disclosure data), representing a year-on-year growth of 74.64% to 91.40%.

Hygon Information stated that the performance growth is mainly attributed to the company's continuous optimization of the "CPU+DCU" business layout, driving technological innovation and product performance improvement through high-intensity R&D investment, maintaining its leading position in the Chinese domestic market. During the reporting period, driven by the accelerated iteration of artificial intelligence large models, the large-scale deployment of AI Agent applications, and the advancement of the localization process towards commercial applications, the company increased R&D investment and iterated product performance, seizing the development opportunity period, promoting the expansion of the high-end processor product market landscape, achieving rapid growth in operating revenue and continuous improvement in overall performance.