en.Wedoany.com Reported - According to the latest analysis by Wood Mackenzie, lithium mine production in Africa is experiencing a surge, but asset equity remains highly concentrated in China.

According to the latest research report released by Wood Mackenzie, by 2030, the equity share of global lithium resources controlled by Chinese enterprises will surge from approximately one-third in 2020 to 39%.

Based on data from Wood Mackenzie's Lens Metals and Mining platform, this research result directly highlights a core divergence in the global critical minerals sector: the actual production geography (geographical distribution) of lithium mines is becoming disconnected from the nationality of asset owners (equity ownership).

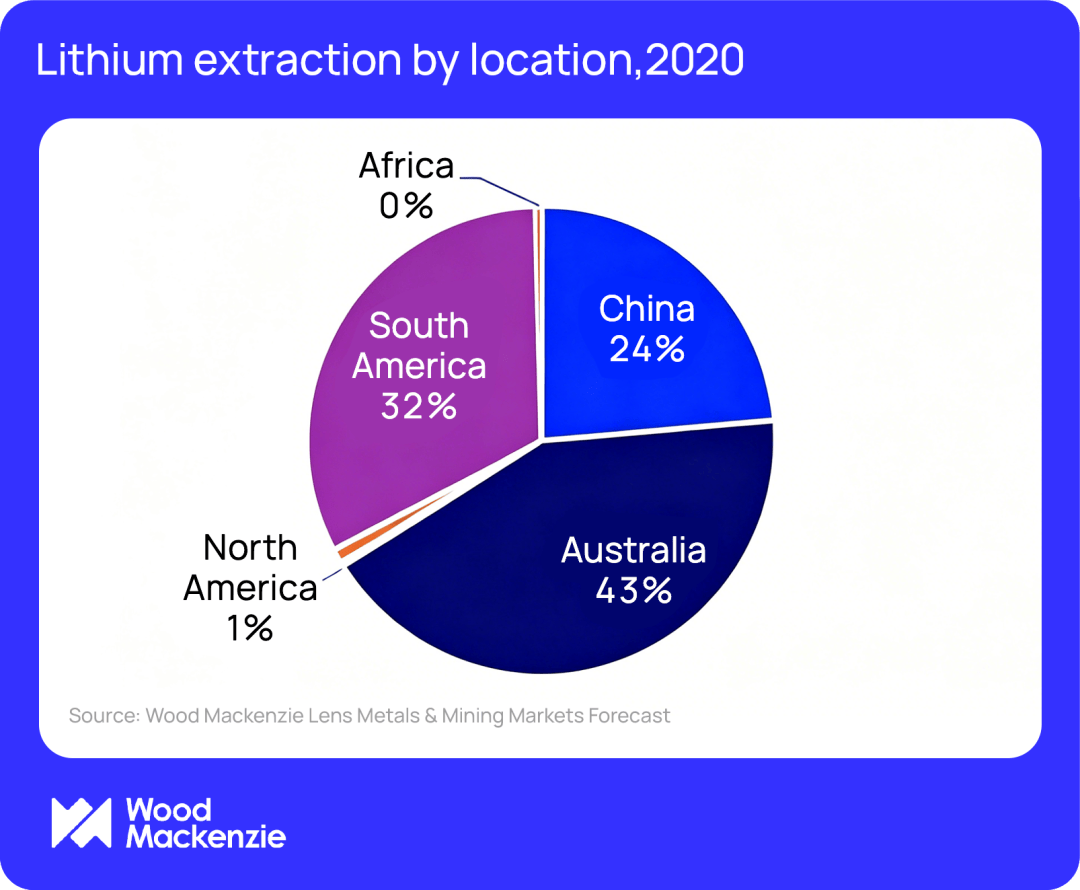

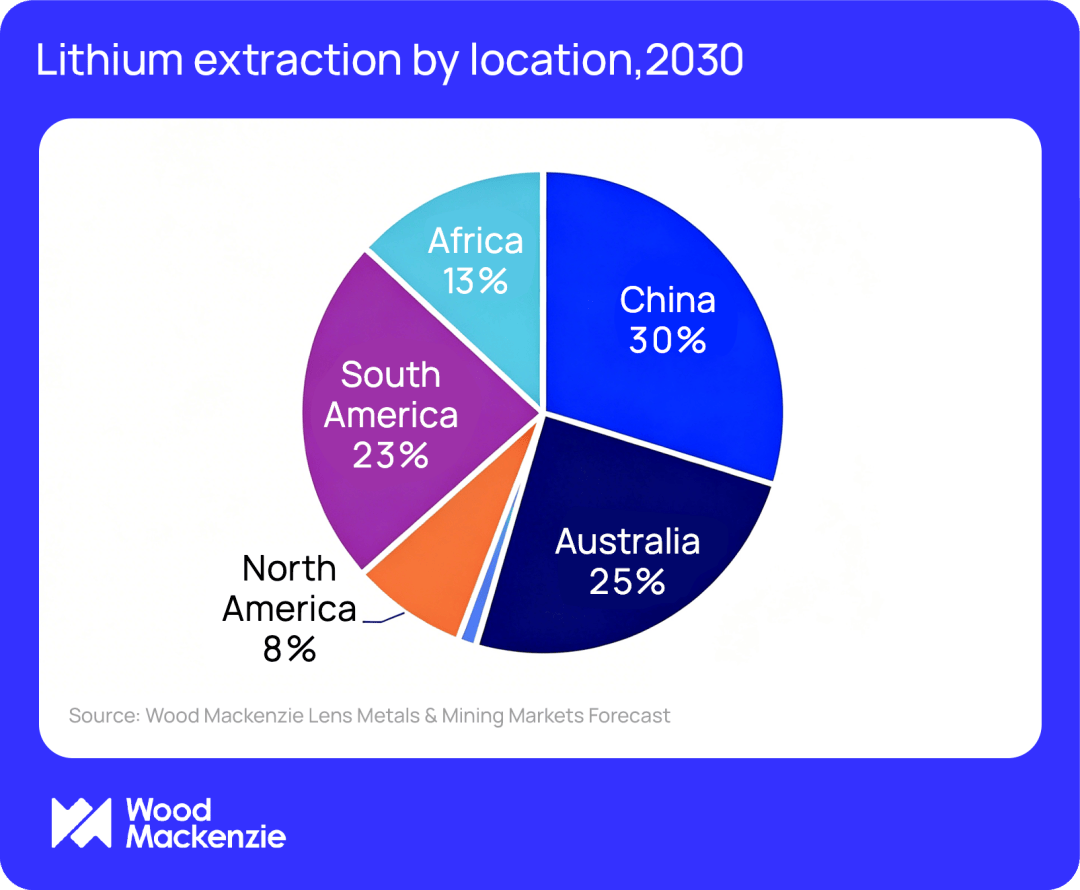

Australia, which long dominated the global lithium supply landscape, accounted for 43% of global mine production in 2020. However, by 2030, this share is forecast to decline to 25%. It is important to clarify that this is not due to shrinking mine investment in Australia, but rather the astonishingly rapid ramp-up in other regions, particularly Africa. Africa's share of global lithium mine production is expected to skyrocket from nearly zero in 2020 to 13% in 2030, marking one of the most disruptive regional supply shifts in the global lithium battery upstream sector.

The "production location" and "equity ownership" of lithium mines are showing increasingly sharp polarization, which is reshaping the supply chain landscape for global critical minerals. While the growth of global production output is diversifying geographically, asset equity remains highly concentrated in the hands of a very small number of enterprises, predominantly led by Chinese companies.

01 Filling the Western Void: Chinese Enterprises' Global Mine Control Layout

The equity ownership layout of Chinese enterprises has long extended far beyond their domestic mine strongholds in China. Chinese companies have established significant asset positions in Australia and Argentina, while deploying capital on a large scale in Africa to fill the void left by increasingly cautious Western investors.

Recently, Huayou Cobalt's proposed acquisition of Atlantic Lithium and joint investment in the Ewoyaa project in Ghana is the latest example of Chinese capital expanding its equity share in the global lithium resource landscape. This follows several major transactions that have already built a strong moat for Chinese capital's dominant position in core production regions, including: Tianqi Lithium securing a 51% stake in the Greenbushes mine in Western Australia (subsequently diluted through a deal with Australian IGO to introduce local capital), and Hainan Mining's substantial investment in Kodal Mining's Bougouni lithium project in Mali.

02 Africa: A Typical Example of the Disconnect Between Production and Equity

Wood Mackenzie points out that Africa most clearly demonstrates the widening divergence between lithium mine production and ownership. Although the entire African continent will account for 13% of global lithium mine production by 2030, enterprises headquartered in Africa are expected to own only 1% of global output.

With few exceptions, the growth of African lithium mines has been largely financed by Chinese capital. As capacity continues to ramp up, this raises important questions about ownership attribution, value capture, and long-term supply chain influence.

03 South America, Europe, and North America: Structural Constraints and Geopolitical Reshuffling

South America also faces heavy competitive pressure. Despite continued investment, the region's share of global lithium supply is expected to fall below one-quarter by 2030. This bottleneck is structural: compared to hard-rock lithium mines, brine-based production has a long production cycle and extremely complex capacity expansion; meanwhile, hard-rock mine capacity in other global regions, such as lepidolite, continues to expand rapidly.

In other regions, following Rio Tinto's acquisition of Arcadium Lithium and Equinor's entry into the battery materials sector, Europe's lithium mine ownership share is rising; while North America's share is declining due to the sale of US-held assets to Rio Tinto. Enterprises headquartered in Australia, supported by both their domestic assets and overseas investments, are expected to retain ownership of approximately 21% of global lithium mine production by 2030.

04 Policy Outlook and Geopolitical Risks

As governments intensify efforts to secure critical mineral supply chains, the high concentration of lithium mine ownership in multiple production regions is likely to remain a growing strategic and policy concern.